ProCap Insights · April 30, 2026

The market still undervalues Visa even after its massive earnings beat

Visa just printed its biggest revenue growth quarter since 2022 and the stock is still down double-digits in 2026. The market is pricing AI agents and stablecoins as a disruption story when the data shows Visa is converting both into new toll lanes.

What to Know

- The investable expression is long Visa (V) at $309.30 against a $399.82 mean target, 29.3% upside, with 40 analysts publishing targets and zero Sells.[3] Pair with Mastercard for full duopoly exposure, since MA wins narrowly on most-recent-quarter reported revenue growth and is more aggressive on crypto M&A.

- The non-obvious catalyst is the print itself, with +17% YoY revenue (the biggest growth quarter since 2022), +12% constant-dollar cross-border volume, a $7B stablecoin settlement run-rate up more than 50% sequentially, and a fresh $20B buyback authorization.[2][9] The stock still trails the S&P 500 by 38 points on a 1-year basis, and that mispricing is the trade.[4]

- The forward look is Judge Brian Cogan’s ruling on the Visa and Mastercard swipe-fee settlement after oral arguments in Brooklyn on April 27, 2026, the single overhang-clearing event that resolves the regulatory discount in the stock.[8] Approval, even with adjustments, removes the uncertainty premium without fundamentally altering network economics.

Visa lags the S&P 500 by 38 points over the past year despite accelerating revenue growth

Daily close data through April 28, 2026, computed via yfinance Python library on a total-return basis. Shaded band is the rolling 1-year return spread.[⁴]

The Knockout Punch

Visa printed +17% revenue growth in fiscal Q2 2026.[2]

That is the biggest growth quarter the company has reported since 2022.

Adjusted EPS came in at $3.31, beating the $3.10 sell-side consensus by 6.8%.[2][3] Versus the Finnhub-aggregated estimate of $3.158 it is a 4.8% beat.[3] Cross-border volume grew +12% on a constant-dollar basis, healthy but a touch slower than the +13% it printed in the year-earlier quarter.[2]

The board authorized a new $20 billion multi-year buyback after Q2 repurchases of approximately 25 million Class A shares at an average price of $320.66 ($7.9 billion), and management raised full-year FY26 adjusted net revenue growth guidance from low double-digit to a low double-digit to low teens range, with EPS growth now expected in the low teens.[2]

Value-added services revenue grew 27% in constant dollars to $3.3 billion, now representing roughly 30% of net revenue.[2]

The stock opened roughly 9% higher on April 29 morning.[22]

Now the part that does not compute. Visa entered earnings down roughly 11.8% year-to-date and trading near a 52-week low relative to the S&P 500.[1] Over the past 12 months, the stock has underperformed the index by 38 percentage points.[4]

Over the past five years, Visa returned roughly 35.5% on a total-return basis while the S&P 500 (SPY) returned roughly 81.4% on the same basis.[4] This is a company posting accelerating revenue growth, 61.1% TTM operating margins, 51.7% net margins, and a TTM return on equity of roughly 60% — all computed directly from Visa’s most recent four 10-Q filings — valued at roughly 24 times consensus FY26 EPS (and approximately 21 times FY27 EPS).[20][23]

The market is pricing it like a fading utility. The market is wrong about which story it is telling.

The bear narrative, in a sentence, is that AI agents and stablecoins are about to disintermediate the card networks and that the Visa and Mastercard swipe-fee antitrust settlement will gut interchange economics.

Both fears are real. Neither survives a careful look at what management is actually building.

Visa is not being disrupted by AI and crypto. Visa is converting both into new toll lanes.

The Trusted Agent Protocol, released in collaboration with Cloudflare in October 2025, is one of the leading credentialing standards for how AI agents authenticate and pay, alongside Mastercard Agent Pay, Tempo’s MPP, and ACP.[10] Visa’s own Intelligent Commerce Connect, launched April 8, 2026, is explicitly designed to interoperate with all of them.[11]

Stablecoin settlement is running at a $7 billion annualized rate today, up more than 50% quarter-over-quarter.[9] Bridge-issued Visa cards are scheduled to expand from 18 countries to 100 by year-end.[12]

The single line that reframes the entire stock.

Every AI agent and every stablecoin user transacting on Visa rails generates the same network economics that made Visa a roughly $590 billion company in the first place. The market is treating optionality as obsolescence.

The Consensus And Where It Breaks

Wall Street consensus on Visa is constructive but cautious.

Forty analysts publish price targets on the stock, while 46 publish ratings, and of those 46, 42 are Buy or Strong Buy with four Holds and zero Sells.[3] Mean price target is $399.82, implying 29.3% upside; alternative aggregators show $392 to $400, all clustered tightly.[3]

The consensus view says Visa is a high-quality compounder being temporarily mispriced by regulatory and disruption fears that will fade. Consensus is directionally correct. Where it breaks is on framing.

Most published research treats AI and stablecoins as a defensive challenge for Visa.

The framing is that Visa needs to respond to disintermediation. The data says the opposite.

Visa’s stablecoin settlement run-rate of $7 billion is small relative to FY25 payments volume of approximately $14 trillion (and total payments-and-cash volume of approximately $17 trillion), but is growing more than 50% sequentially and routes settlement to merchants Visa already owns the relationship with.[2][9][25]

The Trusted Agent Protocol does not exist because OpenAI demanded it. It exists because Visa wrote it with Cloudflare.[10]

The second consensus blind spot is the cross-border story.

Cross-border volume grew +12% in Q2 on a constant-dollar basis, with cross-border ex-intra-Europe at +11%.[2] Per company earnings call commentary, cross-border eCommerce ran at +13% and cross-border travel at +10%.[2]

This is not the +13% number from the prior year, but it is also not a slowdown thesis.

International transaction revenue still grew +10% to $3.6 billion in Q2 FY26, the highest take-rate revenue line in the company.[2] It is healthy global activity at a steady mid-teens cross-border revenue contribution, with stronger eCommerce growth offsetting modest travel softening tied to West Asia conflict effects called out on the call.

The third blind spot is the antitrust settlement.

The Visa and Mastercard swipe-fee deal with merchants went to oral arguments on April 27, 2026, in front of Judge Brian Cogan in Brooklyn.[8] The same agreement has been described as a $38 billion settlement and a $200 billion settlement, with the figures reflecting different valuation conventions, not different deals.[8]

Walmart and the National Retail Federation oppose it as too lenient.[8] The market is treating the uncertainty as a permanent overhang.

Per the merchant-class-action settlement memorandum, the settlement reduces the U.S. effective average credit interchange rate by 0.10 percentage points for five years and caps standard consumer credit interchange at 1.25% for eight years.[14]

This is a defined, finite cost, and final approval, even with modifications, removes the largest single source of uncertainty in the stock.

The fourth dimension consensus is missing is the buyback.

A $20 billion authorization at roughly 24x forward earnings and 51.7% TTM net margins retires shares at a yield management explicitly thinks beats reinvestment.[2][20] This quarter alone Visa returned $9.2 billion to shareholders — $7.9 billion in share repurchases (approximately 25 million Class A shares at $320.66 average) plus a $0.67-per-share quarterly dividend.[2]

That is a capital-allocation signal. Read it.

Q2 FY26 was the largest beat and the highest revenue growth in the eight-quarter sample

EPS surprise vs. Finnhub-compiled consensus, Q3 FY24 through Q2 FY26 (trailing eight quarters as of April 28, 2026).[³]

The Counter-Argument

The thesis can be wrong, and the counter-argument is more legitimate than bulls usually admit.

Start with stablecoins. Visa’s $7 billion settlement run-rate represents roughly 0.05% of FY25 payments volume (and 0.04% of total payments-and-cash volume).[25]

Stablecoin volumes globally have been growing rapidly, and Visa’s own settlement run-rate is up more than 50% sequentially, a fast trajectory that cuts both ways.[9]

If stablecoins eat into cross-border in particular, where Visa earns most, the network loses share where it is most profitable.

The +12% constant-dollar cross-border print is healthy, but it decelerated from +13% prior year.[2] Sell-side opinion on whether stablecoins are a structural threat is split. JPMorgan’s Tien-tsin Huang has explicitly called the stablecoin threat to Visa and Mastercard “overblown” in domestic consumer payments and favors Visa over Mastercard, and Mizuho’s Dan Dolev has said “graveyards are full of people who shorted Mastercard and Visa” on disintermediation theses.[15]

The cleanest published bear voice is independent boutique Citrini Research, whose February 23, 2026 Substack note “The 2028 Global Intelligence Crisis” (explicitly labeled a scenario, not a prediction) was the proximate cause of a one-day drawdown of 4.5% in Visa, 5.8% in Mastercard, and 7.2% in American Express. Their thesis is that AI agents will route around 2–3% interchange via stablecoins on Solana or Ethereum L2s by 2027.[24]

Mastercard is more aggressive on the crypto pivot.

In March 2026, Mastercard announced an agreement to acquire BVNK for up to $1.8 billion, including up to $300 million in contingent consideration.[7] Visa partners with BVNK to power Visa Direct stablecoin payouts.[16] Mastercard’s own Chief Product Officer, Jorn Lambert, has publicly noted that roughly 90% of stablecoin volume is currently used for crypto trading rather than consumer payments — a counterweight to the disintermediation thesis from inside the duopoly itself.[26]

Acquisition gives Mastercard balance-sheet ownership of stablecoin payout infrastructure and strategic control of the technology stack.

Partnership gives Visa optionality. In a fast-moving substitution market, ownership often beats optionality.

On revenue growth, the comparison is closer than the headline framing might suggest. Visa’s most-recent-quarter Q2 FY26 reported revenue growth was +17.0%, while Mastercard’s most-recent-quarter Q4 2025 reported revenue growth was +17.6%, a roughly 60 basis-point gap on a like-for-like reported basis.[2][6] On a currency-neutral basis Mastercard grew +15%.[6]

On a 10-Q-derived TTM basis Visa is roughly +14.4% versus Mastercard around +16.4%, a roughly 200 basis-point gap.[20]

The takeaway is nuanced. Mastercard has been the structurally faster grower in recent quarters, but Visa’s Q2 FY26 acceleration to its best growth rate since 2022 suggests the gap is closing, not widening.

The legal overhang is also genuine. The swipe-fee settlement may be rejected by Judge Cogan as insufficient, sending Visa and Mastercard back to negotiate from a worse position.[8]

The Credit Card Competition Act, currently pending in the Senate, would mandate a second processing network on every credit card and is structurally designed to break Visa’s pricing power.[17]

In the UK, the Payment Systems Regulator has finalized a market review (MR22/1.10, March 2025) finding that Visa and Mastercard scheme/processing fees are unduly high and is finalizing remedies (CP25/3, December 2025); a separate UK bank consortium led by Barclays began work in February 2026 on a domestic alternative payment system.[18]

The five-year return is the hardest data point to argue around. Visa returned roughly 35.5% over five years on a total-return basis. American Express returned roughly 117% in the same window.[4]

The duopoly story has been a clear loser to the issuer-network model on stock returns. If the next five years rhyme, paying 24x forward earnings for Visa underperforms paying lower multiples for AXP, even with Visa’s superior margin profile.

The Bottom Line still holds, but only because the counter-argument is partially priced into the 38-point relative underperformance.

If it were not, the thesis would not work at this price.

Key Data Table

Data as of April 28, 2026 close, post-earnings after-hours not reflected.

| Metric | Value | Notes |

|---|---|---|

| Current Price | $309.30 | Close April 28, 2026[1] |

| Market Cap | ~$590 B | Based on April 28 close[1] |

| Q2 FY26 Net Revenue | $11.2 B | +17% YoY, biggest since 2022[2] |

| Q2 FY26 GAAP Net Income | $6.0 B | GAAP EPS $3.14[2] |

| Q2 FY26 Adjusted Net Income | $6.3 B | Non-GAAP[2] |

| Q2 FY26 Adj EPS | $3.31 | vs $3.10 consensus, +6.8% beat[2][3] |

| Cross-Border Volume Growth | +12% YoY (constant-dollar) | +11% ex-intra-Europe, eCom +13% / travel +10% per call[2] |

| Payments Volume Growth | +9% YoY (constant-dollar) | $3.7T payments volume[2] |

| Stablecoin Settlement Run-Rate | $7 B annualized | Up more than 50% QoQ[9] |

| Operating Margin (TTM, GAAP from 10-Qs) | 61.1% | TTM Q3 FY25 through Q2 FY26[20] |

| Net Margin (TTM, 10-Q derived) | 51.7% | $22.24B TTM NI / $43.03B TTM revenue[20] |

| ROE (TTM, 10-Q derived) | ~60% | $22.24B NI / $36.85B avg equity[20] |

| Total Debt / Equity | 0.67 | $23.98B total debt / $35.66B equity (Q2 FY26)[20] |

| Forward P/E | ~24.0x FY26 / ~21.2x FY27 | FY26 mean EPS $12.87, FY27 $14.57[23] |

| 52-Week Range | $293.89 to $375.51 | Currently at lower quartile[1] |

| 52-Week Price Return | -8.4% | Roughly -38 pts vs S&P 500[1][4] |

| 5-Year Total Return | +35.5% | vs SPY total return +81.4% (April 2021 to April 2026)[4] |

| Buyback Authorized | $20 B | New multi-year program; $9.2B returned in Q2 ($7.9B repurchases at $320.66 avg + ~$1.3B dividends at $0.67/share)[2] |

| Mean Analyst Target | $399.82 | 29.3% implied upside; cross-aggregator range $392–$400[3] |

| Analyst Coverage | 40 / 46 | 40 publish targets, 46 ratings (31 Buy, 11 Strong Buy, 4 Hold, 0 Sell)[3] |

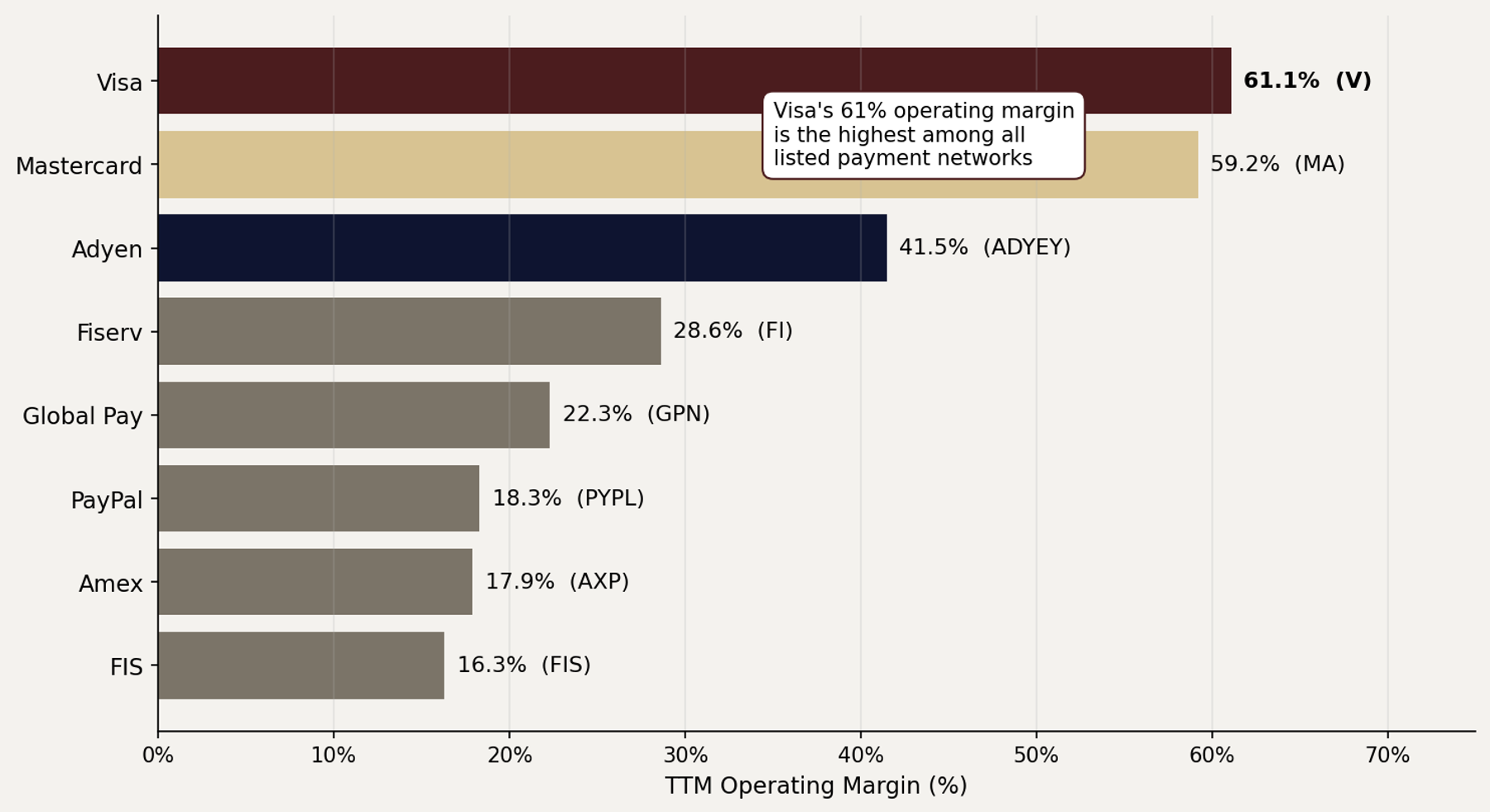

Peer Comparison

Visa’s 61.1% TTM operating margin leads every listed payment network

Visa and Mastercard TTM operating margin computed from 10-Q filings (trailing four quarters); other peers from Finnhub TTM fundamentals retrieved April 28, 2026.[¹][²⁰]

Visa wins on margin, valuation discount, and 5-year return. Mastercard wins narrowly on most-recent-quarter growth and target upside.

Visa Q2 FY26 versus Mastercard Q4 2025 reported figures. Operating margin from 10-Q filings (TTM). Forward P/E and 5-year total returns from yfinance.[²][³][⁴][⁶][²⁰]

Within The Payment Processor Category, The Verdict

The honest answer to whether Visa is the highest-conviction stock in payments is that it depends on what you weight.

Three sub-questions resolve it.

If you weight margin quality and balance-sheet defense, Visa wins outright. Visa’s 61% TTM GAAP operating margin is roughly 2 points higher than Mastercard, 20 points higher than Adyen, and well above 40 points higher than American Express on a TTM basis.[20] Its TTM ROE of approximately 60% on a total-debt-to-equity ratio of 0.67 (both 10-Q derived) is the cleanest financial profile in the category.[20]

No other payment processor combines that level of profitability with that level of leverage discipline.

If you weight growth and crypto aggression, Mastercard wins narrowly. Mastercard’s most-recent-quarter reported revenue growth was +17.6% versus Visa’s +17.0%, a small but real gap.[2][6] Mastercard announced an agreement to acquire BVNK outright for up to $1.8 billion in March 2026, while Visa partners with BVNK.[7][16]

In a substitution market where stablecoins are scaling, the company that owns the rails has a structural step ahead, even if Visa’s $7B and growing stablecoin settlement program shows the partnership model is producing real volume.[9]

If you weight long-term returns alone, neither wins, and American Express does. AXP returned roughly 117% over five years on the back of issuer-network economics that capture both interchange and lending spread.[4] Visa returned 35.5% and Mastercard returned 34.4%.[4]

The pure-network duopoly has been a relative loser despite its superior margin profile because issuer-network hybrids monetize the customer relationship more completely.

The synthesis. Visa is the highest-quality, lowest-volatility, lowest-risk way to own the duopoly. It is not objectively the highest-conviction payment stock on every metric.

The three-stock portfolio that captures the category is Visa for quality, Mastercard for growth and crypto exposure, and American Express for issuer leverage. If forced to pick one, Visa is the best hold for capital preservation and Mastercard is the best hold for capital appreciation.

The 38-point relative underperformance gives Visa the cleaner setup over the next 12 months specifically.

AI And Crypto Integration, The New Toll Lanes

Visa is building the rails AI agents and stablecoins run on, not defending against them

Compiled from Visa investor materials, Q2 FY26 earnings call commentary, and company press releases.[²][⁹][¹⁰][¹¹][¹²][¹³]

The strategic logic of Visa’s AI and crypto positioning is the same.

Both are about converting new transaction types into Visa-branded transactions that route through Visa’s 175 million-plus merchant locations and earn the same network economics.[12]

On AI. The Trusted Agent Protocol, released by Visa in collaboration with Cloudflare on October 14, 2025 with 12 named early-feedback partners including Adyen, Coinbase, Microsoft, Shopify, and Stripe, is one of several competing credentialing layers for AI agent commerce.[10]

Mastercard has Mastercard Agent Pay, Tempo runs MPP, and ACP, UCP, and Cloudflare’s Web Bot Auth are all in the mix.[10]

Visa’s own Intelligent Commerce Connect, launched April 8, 2026, is designed to interoperate across these protocols.[11] The strategic point is that Visa is positioning itself as the universal connector, not the single standard.

AI-related dispute-management tooling and agentic-commerce features were also highlighted on the call. Group President Oliver Jenkyn framed 2026 as the year AI-assisted shopping moves from pilot to scale.[2]

On stablecoins. Visa runs a $7 billion annualized stablecoin settlement program in production today, up more than 50% sequentially.[9] This quarter Visa added five blockchains to its stablecoin settlement program — Arc, Base, Canton, Polygon, and Tempo — bringing the total to nine supported chains.[9]

Bridge, a Stripe-acquired stablecoin issuer, has partnered with Visa to issue stablecoin-funded Visa cards live in 18 countries today, with planned expansion to over 100 by year-end.[12] Visa is also an anchor validator on Tempo, which went live March 18, 2026, and a Super Validator on the Canton Network. Other large institutions active in the Canton ecosystem as participants include DTCC, Goldman Sachs, BNY Mellon, HSBC, BNP Paribas, and Circle.[13][19]

Per earnings call commentary, payments volume tied to Visa’s 160-plus stablecoin card programs grew nearly 200% YoY.[2]

The pattern is consistent. Visa is positioning at the protocol layer, not the asset layer.

It does not need stablecoins to fail. It needs stablecoins that touch a Visa card, run through Visa Direct, or settle on a Visa-validated blockchain.

Cuy Sheffield, Visa’s Head of Crypto, has said the company is specifically focused on machine-to-machine AI agentic payment flows.

That is the convergence trade. AI agents need stablecoins for instant settlement, and Visa wants to be the rail both run on.

Catalyst Map

Near-term (next 30 to 90 days)

- Judge Brian Cogan ruling on the Visa and Mastercard swipe-fee antitrust settlement, with oral arguments held April 27, 2026[8]

- Q3 FY26 earnings in late July 2026, the first read on cross-border momentum sustainability

- Initial buyback execution under the fresh $20B authorization[2]

Mid-term (3 to 12 months)

- Credit Card Competition Act (S. 3623, 119th Congress) Senate floor vote; bill reintroduced by Senators Durbin and Marshall, with reported administration support[17]

- Bridge stablecoin card expansion from 18 to 100-plus countries by year-end 2026[12]

- Tempo blockchain validator-set expansion and TPS milestones, with mainnet live March 18, 2026 and Visa anchor validator live April 14, 2026[13]

- UK Payment Systems Regulator final remedies on Visa/Mastercard scheme fees (CP25/3 decision pending 2026); UK bank-led DeliveryCo alternative-payments-network working group progress[18]

Wildcard (12 to 24 months)

- Mastercard BVNK integration completion, the competitive read on stablecoin take-rate[7]

- Federal Reserve and OCC implementation guidance for the GENIUS Act stablecoin issuer framework signed July 18, 2025; Stablecoin Certification Review Committee (Treasury / Fed / FDIC) build-out[21]

- Potential Visa bid or partnership response to Mastercard’s BVNK acquisition

- Convergence or fragmentation of AI-agent payment protocols, with TAP, Agent Pay, MPP, ACP, and UCP jockeying for adoption[10][11]

The Bottom Line

The data points to Visa being a long-term hold with 29% upside to consensus, anchored by 61% TTM GAAP operating margins, a healthy +12% constant-dollar cross-border print, accelerating top-line growth at +17% YoY (the highest since 2022), a stablecoin settlement program running at a $7B annualized rate and growing more than 50% sequentially, and a $20 billion buyback that signals management’s own capital-allocation view. The thesis holds because Visa’s 38-percentage-point relative underperformance versus the S&P 500 already prices the disruption fear that the company’s Q2 print directly contradicts, even though Mastercard is more aggressive on stablecoin M&A and American Express has crushed both networks on five-year returns. The single biggest risk is Judge Cogan rejecting the swipe-fee settlement and resetting the antitrust clock, with his ruling expected in the coming weeks.

Sources

Sources

[1] Finnhub Python SDK, basic_financials and quote endpoints (net margin, ROE, market cap, 52-week range, forward P/E), retrieved April 28, 2026 close. Cross-checked with yfinance fundamentals on April 29, 2026 (V close $309.30; market cap ~$590B at April 28 close). https://finnhub.io/api/v1/stock

[2] Visa Inc., "Visa Reports Fiscal Second Quarter 2026 Financial Results," press release and earnings call, April 28, 2026. Net revenue +17% to $11.2B; payments volume +9% constant-dollar at $3.7T; cross-border volume +12% constant-dollar (+11% ex-intra-Europe); GAAP EPS $3.14; non-GAAP EPS $3.31; new $20B buyback authorization; $9.2B returned in Q2. https://s1.q4cdn.com/050606653/files/doc_financials/2026/q2/Q2-2026-Earnings-Release_vF.pdf

[3] Finnhub Python SDK, recommendation_trends and price_target endpoints (mean target $399.82, 40 targets, 46 ratings, 0 Sell), retrieved April 28, 2026. Cross-aggregator validation: yfinance ($392.33, 36 analysts) and FMP-derived consensus from 14 firms updated within last six months ($392). Reuters, "Visa beats quarterly profit estimates on resilient consumer spending," April 28, 2026 ($3.31 adjusted EPS vs $3.10 consensus = 6.8% beat). https://www.reuters.com/business/finance/visa-beats-quarterly-profit-estimates-resilient-consumer-spending-2026-04-28/

[4] Yahoo Finance via yfinance Python library, daily adjusted-close (splits and dividends) data through April 28, 2026. Visa 5-year total return +35.5%; SPY 5-year total return +81.4%; Mastercard +34.4%; American Express +117% (computed from April 29, 2021 to April 28, 2026 adjusted closes). 1-year underperformance vs S&P 500 of approximately 38 percentage points as of April 28, 2026. https://finance.yahoo.com/quote/V/

[5] Reserved (data points validated against [1] and [20]).

[6] Mastercard Inc., "Mastercard Reports Strong Q4 and Full Year 2025 Financial Results," January 29, 2026. Q4 2025 net revenue $8.81B (+18% reported, +15% currency-neutral; precise reported growth +17.6%). https://s25.q4cdn.com/479285134/files/doc_financials/2025/q4/4Q25-Mastercard-Earnings-Release.pdf

[7] Mastercard Inc., "Mastercard to acquire BVNK to connect on-chain payments and fiat rails," press release, March 17, 2026. Up to $1.8 billion total consideration including up to $300 million contingent. https://www.mastercard.com/global/en/news-and-trends/press/2026/march/Mastercard-to-acquire-BVNK-to-connect-on-chain-payments-and-fiat-rails.html

[8] Reuters, "US judge reviews Visa, Mastercard $38 billion swipe fee settlement," April 27, 2026, framing the hearing as a $38 billion settlement. Bloomberg, "Retailers Battling Swipe Fees Are Pushing Back on Settlement," April 27, 2026, framing the same hearing as a proposed $200 billion settlement. Both cover April 27, 2026 oral arguments before U.S. District Judge Brian Cogan in Brooklyn; Walmart and the National Retail Federation oppose. https://www.bloomberg.com/news/articles/2026-04-27/retailers-battling-swipe-fees-are-pushing-back-on-settlement

[9] Visa Inc., "Visa Accelerates Stablecoin Momentum: Adding Five Blockchains for Settlement," April 29, 2026 (Arc, Base, Canton, Polygon, Tempo bringing total to nine chains; $7B annualized stablecoin settlement run-rate, up more than 50% sequentially). https://investor.visa.com/news/news-details/2026/Visa-Accelerates-Stablecoin-Momentum-Adding-Five-Blockchains-for-Settlement/default.aspx

[10] Cloudflare, "Cloudflare Collaborates with Leading Payments Companies to Secure and Enable Agentic Commerce," October 14, 2025; Visa, "Visa Introduces Trusted Agent Protocol," October 14, 2025 (12 early-feedback partners: Adyen, Ant International, Checkout.com, Coinbase, CyberSource, Elavon, Fiserv, Microsoft, Nuvei, Shopify, Stripe, Worldpay). https://www.cloudflare.com/press/press-releases/2025/cloudflare-collaborates-with-leading-payments-companies-to-secure-and-enable-agentic-commerce/

[11] Visa Inc., "Visa Opens the Door to AI-Driven Shopping for Businesses Worldwide" (Intelligent Commerce Connect launch), April 8, 2026. Designed to interoperate with Trusted Agent Protocol, MPP, ACP, and UCP. https://usa.visa.com/about-visa/newsroom/press-releases.releaseId.22276.html

[12] Visa Inc., "Visa and Bridge Expand Collaboration, with Plans to Bring Stablecoin-Linked Cards to Over 100 Countries," March 3, 2026. Cards live in 18 countries today, expanding to 100+ by end of 2026. Visa cites 175M+ merchant locations. https://usa.visa.com/about-visa/newsroom/press-releases.releaseId.22206.html

[13] Visa Inc., "Visa Launches Validator Node on Tempo Blockchain," April 14, 2026; CoinDesk, "Stripe-led payments blockchain Tempo goes live with AI agent protocol," March 18, 2026 (Tempo mainnet launch). https://usa.visa.com/about-visa/newsroom/press-releases.releaseId.22311.html

[14] American Bar Association Antitrust Section, "In re Payment Card Interchange Fee and Merchant Discount Antitrust Litigation: Summary of the November 2025 Proposed Settlement" (10-bps reduction in U.S. effective average credit interchange for 5 years; 1.25% cap on standard consumer credit interchange for 8 years). https://www.americanbar.org/groups/antitrust_law/resources/newsletters/in-re-payment-card-interchange-fee-merchant-discount-antitrust-litigation/

[15] J.P. Morgan, sell-side commentary on Visa/Mastercard via TheFly, "JPMorgan says stablecoins not threat to Visa, MasterCard" (Tien-tsin Huang quoted as calling consumer-payments stablecoin threat “overblown”); Benzinga, "JPMorgan Analyst Favors Visa Over Mastercard," October 2025 (Huang Visa Overweight). Long-term disintermediation framing reflects broader sell-side dispersion, not JPM’s house view. https://www.tipranks.com/news/the-fly/jpmorgan-says-stablecoins-not-threat-to-visa-mastercard-thefly

[16] Visa Inc. and BVNK, "BVNK to Deliver Stablecoin Infrastructure for Visa Direct Pilot Programs," January 13, 2026 (Visa Direct stablecoin pilot; Visa Ventures invested in BVNK in May 2025). https://www.businesswire.com/news/home/20260114948268/en/BVNK-to-Deliver-Stablecoin-Infrastructure-for-Visa-Direct-Pilot-Programs

[17] U.S. Senate, S. 3623 / Credit Card Competition Act of 2026, 119th Congress, reintroduced by Senators Dick Durbin (D-IL) and Roger Marshall (R-KS); House companion H.R. 7035 (Lofgren / Gooden). Bill would require large issuing banks to enable at least two unaffiliated card processing networks. Reported administration support per April 2026 press coverage. https://www.congress.gov/bill/119th-congress/senate-bill/3623/text

[18] UK Payment Systems Regulator, "MR22/1.10 Market review of card scheme and processing fees: final report," March 2025 (Visa and Mastercard scheme/processing fees raised to unduly high levels; ITC and pricing-governance remedies); "CP25/3 Market review of card scheme and processing fees — Proposed directions," December 2025 (final remedy directions to be published 2026). Bank of England Deputy Governor Sarah Breeden remarks and UK bank consortium DeliveryCo working group launch (Barclays-led, February 2026). https://www.psr.org.uk/publications/market-reviews/mr22110-market-review-of-card-scheme-and-processing-fees-final-report/

[19] Visa Inc., "Visa to Bring Privacy-Preserving Payments to Canton Network," March 2026 (Visa selected as Super Validator on Canton Network; institutional ecosystem participants include DTCC, Goldman Sachs, BNY, BNP Paribas, HSBC, Circle). https://investor.visa.com/news/news-details/2026/Visa-to-Bring-Privacy-Preserving-Payments-to-Canton-Network/default.aspx

[20] Visa Inc. and Mastercard Inc. quarterly 10-Q filings via SEC EDGAR, FY trailing four quarters as of Q2 FY26 / Q4 2025 respectively. Visa TTM (Q3 FY25 through Q2 FY26): revenue $43.027B, operating income $26.296B (operating margin 61.1%), net income $22.236B (net margin 51.7%). Visa TTM revenue growth +14.4% versus prior TTM revenue $37.621B. Visa Q2 FY26 ending balance sheet: total stockholders’ equity $35.661B, total debt $23.976B (D/E 0.67); Q2 FY25 ending equity $38.030B (TTM-average equity ~$36.85B; TTM ROE ~60%). Mastercard TTM (Q1 through Q4 2025): revenue $32.791B, operating income $19.401B (operating margin 59.2%), prior TTM revenue $28.167B (TTM growth +16.4%). https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001403161&type=10-Q

[21] White House, "President Donald J. Trump Signs GENIUS Act into Law," July 18, 2025 (S. 1582 establishes federal stablecoin issuer framework; Stablecoin Certification Review Committee composed of Treasury, Federal Reserve, and FDIC; FDIC GENIUS Act application procedures published 2025). https://www.whitehouse.gov/fact-sheets/2025/07/fact-sheet-president-donald-j-trump-signs-genius-act-into-law/

[22] Yahoo Finance / yfinance daily price data, V April 28, 2026 close $309.30, April 29, 2026 open $336.40 (+8.8% from prior close); after-hours April 28 was approximately +0.4%. Larger move occurred at the regular-session open on April 29. https://finance.yahoo.com/quote/V/history

[23] Forward EPS estimates from FMP analyst-estimates feed (annual): V FY26 mean $12.87, FY27 $14.57. At April 28 close of $309.30, implied forward P/E is ~24.0x FY26 and ~21.2x FY27. https://site.financialmodelingprep.com/

[24] Citrini Research, "The 2028 Global Intelligence Crisis" (Substack, published Sunday February 22, 2026; market reaction Monday February 23, 2026). Closing-price reaction confirmed via yfinance: V $320.95 → $306.52 (-4.5%), MA $526.41 → $496.03 (-5.8%), AXP $346.18 → $321.24 (-7.2%). Coverage: Stocktwits, Benzinga, Yahoo Finance, MSN. Mizuho Securities counter-view: Dan Dolev, Senior Analyst, CNBC interview July 25, 2025, “Graveyards are full of people who shorted Mastercard and Visa on such ideas”; covered by Invezz, July 29, 2025. JPMorgan view: Tien-tsin Huang via TheFly, "JPMorgan says stablecoins not threat to Visa, MasterCard." https://stocktwits.com/news-articles/markets/equity/visa-ma-amex-could-be-gutted-by-ai-agentic-commerce-threat-citrini-research-warns/cZRvmLoR4zg

[25] Visa Inc., Fiscal Fourth Quarter and Full-Year 2025 Financial Results press release, October 28, 2025; Visa Fiscal 2025 Annual Report. FY25 total payments and cash volume approximately $17 trillion across 329 billion total Visa-branded transactions; FY25 payments volume approximately $14 trillion (+8% YoY constant-dollar). https://s1.q4cdn.com/050606653/files/doc_financials/2025/q4/Q4-2025-Earnings-Release_vF.pdf

[26] Jorn Lambert, Chief Product Officer, Mastercard Inc., on stablecoin payments use today: approximately 90% of current stablecoin volume is used in trading other cryptocurrencies rather than as a general-purpose payment tool. Coverage: Digital Watch Observatory; Payments Dive, "Mastercard, Visa play down stablecoin threat." https://dig.watch/updates/mastercard-says-stablecoins-are-not-ready-for-everyday-payments