ProCap Insights · April 27, 2026

2 stocks that rally if Kalshi is right about Fed rate cuts

Prediction markets price roughly a 60% chance the Fed cuts at least once in 2026. Rates futures price about 27%. Two rate-sensitive stocks at or near 52-week lows are trading like the futures market is right, and the asymmetry favors the names that move when Kalshi does.

What to Know

- The trade is long Lennar (LEN, $94.05) and BXP Inc (BXP, $57.73), both at or near 52-week lows and decoupled from their sector ETFs by 14 to 18 percentage points over three months.

- Kalshi prices a roughly 60% probability of at least one 2026 cut while CME Fed Funds futures price about 27%, the widest divergence of this cycle.

- The catalyst window collapses into the next three weeks as Sen. Tillis lifts his hold on the Warsh confirmation, the Banking Committee votes April 29, and Powell's term ends May 15.

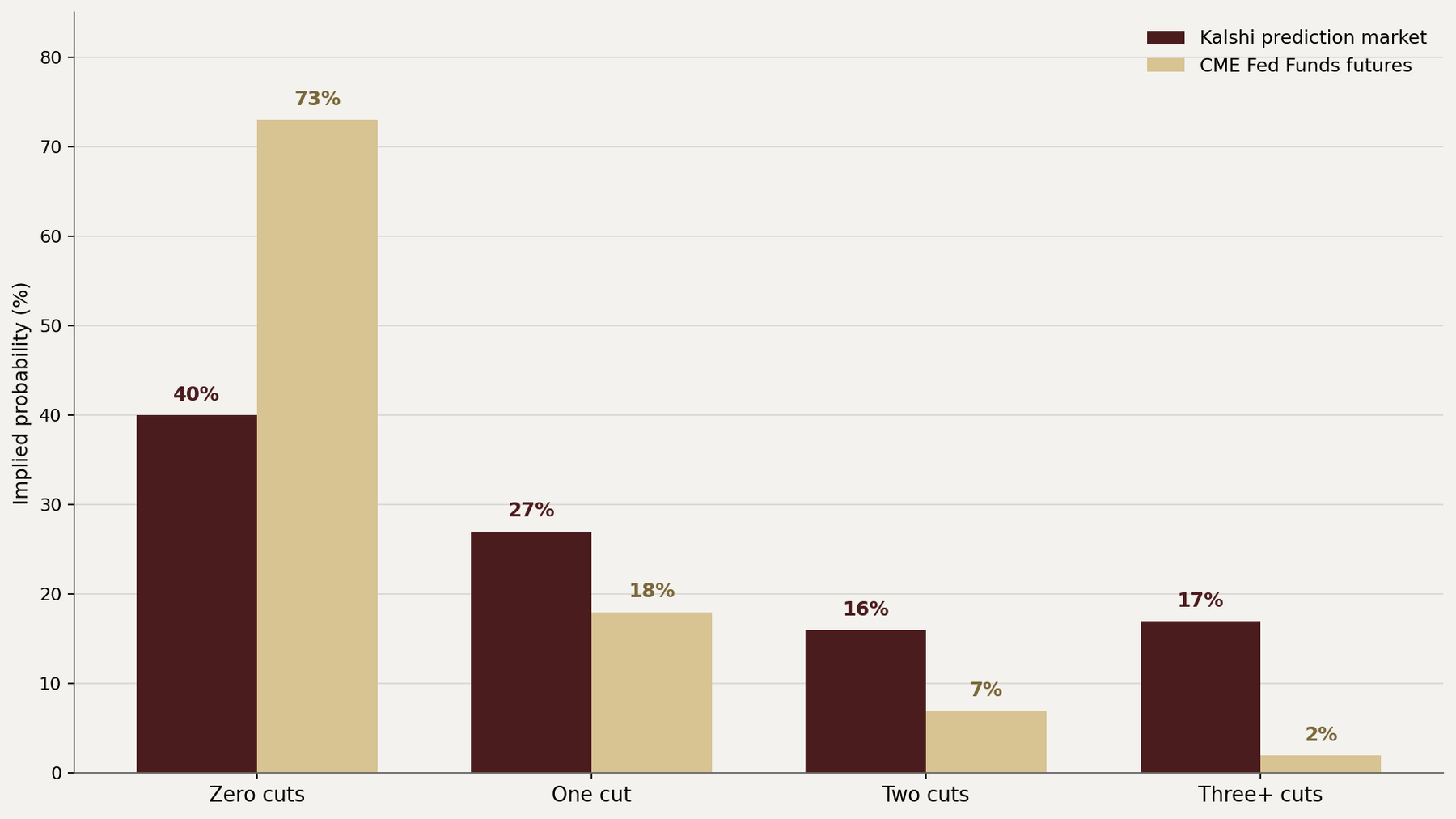

Kalshi prices a 60% chance of a 2026 cut. CME futures price 27%.

Implied 2026 cut count distribution.²

The Theme

The Fed has held the federal funds rate at 3.50 to 3.75% since December 2025. The March 2026 dot plot showed a median of one cut for 2026, with seven of nineteen FOMC members projecting zero. CME Fed Funds futures price roughly 73% probability of zero cuts in 2026.2

Kalshi prices roughly 40% probability of zero cuts.5 The two markets are looking at the same Fed and pricing very different outcomes.

The divergence is not noise. The current Kalshi distribution shows zero cuts at about 40%, one cut at 27%, two cuts at 16%, and three or more cuts at roughly 17%, implying about 60% at-least-one-cut.5

Polymarket converges on a similar 60% implied probability for the first 2026 cut by year-end.6

CME futures and equity rate-sensitive sectors converge near 27%. Prediction markets are pricing the political-economy reality of Powell departing, Warsh advancing through confirmation, and oil collapsing.

Rates futures price the textbook reaction function with core PCE running at 3.0% in February 2026, the most recent reading.11

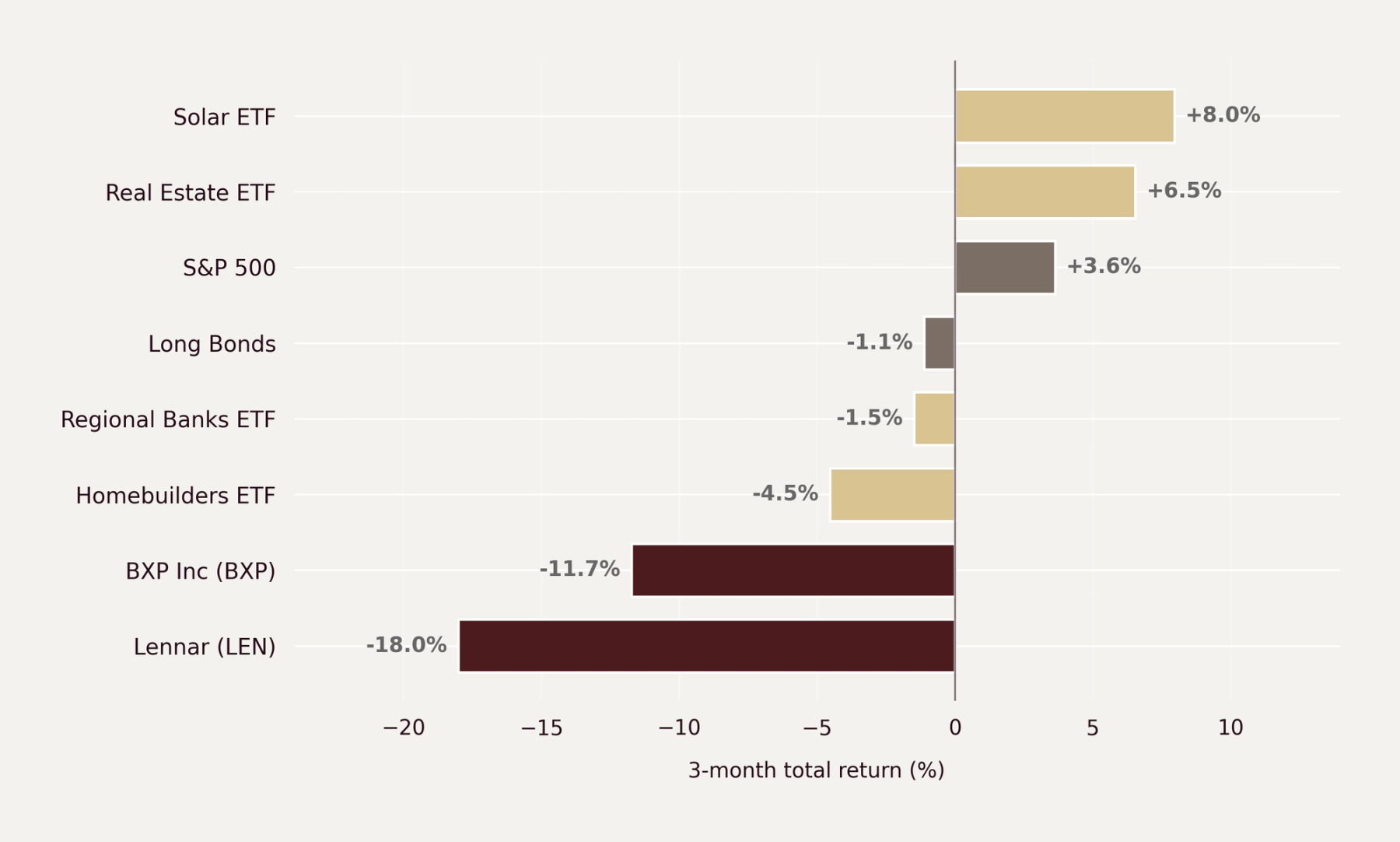

Equities have followed CME, not Kalshi. The XHB Homebuilders ETF is down 4.5% in three months even though Freddie Mac PMMS shows the 30-year fixed-rate mortgage at 6.23% for the week ending April 23, 2026.17

The XLRE Real Estate ETF is up 6.5% over three months and up 8.6% YTD, but that strength has been driven by data center REITs while office and net-lease REITs lag.

Specific names within rate-sensitive sectors have decoupled from their own ETFs in ways that imply zero probability of relief.

The Consensus and Where It Breaks

Wall Street consensus is the dot plot, and the dot plot says one cut in 2026.

The published forecasts span the same range. Goldman Sachs Research expects two 25-basis-point cuts in 2026, in June and September, taking the funds rate to 3.00 to 3.25% by year-end. Morgan Stanley's November 2025 US Economics Outlook penciled in three cuts running through April 2026.

JPMorgan's Michael Feroli forecasts zero cuts in 2026, with the Fed's next move a 25-basis-point hike in Q3 2027.7

The CME-aligned 27% probability of any cut is the institutional default. Equity flows have followed CME pricing, not Kalshi.

Where consensus breaks is the assumption that Powell-era reaction functions persist past May 15.

Kevin Warsh's November 2025 Wall Street Journal op-ed argued the Fed's balance sheet can be reduced significantly and that the resulting capacity should be redeployed as lower interest rates for households and small and medium-sized businesses. His April 2025 G30 Spring Lecture at the IMF, “Commanding Heights: Central Banks at a Crossroads,” argued for a regime change at the Fed.8

At his April 21 Senate Banking Committee hearing, Warsh struck a more balanced public tone. He told senators he never promised the White House he would cut rates and pledged to be an independent actor, while reaffirming inflation control and signaling appetite for regime change at the central bank.9

Democrats accused him of flip-flopping. Markets read the testimony as confirming a policy reset, not a dovish capitulation.

With Tillis's hold lifted on April 26, the Banking Committee vote is scheduled for Wednesday April 29. A full Senate vote is expected within days.3

By the June 16 to 17 FOMC, Warsh could plausibly be voting and the dots could reflect his preferences. Kalshi traders are pricing this transition. Equity markets are not.

The second break is oil.

WTI peaked near $113 on April 6 during the Iran Strait of Hormuz crisis and collapsed to about $80 after the strait reopened on April 17, with WTI closing at $79.78, a single-session decline of more than 12%.10

Headline CPI for March 2026 came in at 3.3% year over year, with the gasoline index posting its largest monthly increase since the series began in 1967, up 21.2% on the month and 18.9% versus a year earlier.11

The April CPI release on May 12 will show the post-ceasefire energy reversal. Core PCE for February 2026, the most recent BEA reading, came in at 3.0% year over year, down from 3.1% in the prior month, still a full percentage point above the Fed's 2.0% target.

Fed officials have already begun pivoting to energy-pass-through framing.

LEN at minus 18% and BXP at minus 11.7% are not sector trades. They are idiosyncratic mispricings.

Three-month total return, January 22 to April 24, 2026.¹

The Names That Express It

Lennar (LEN). The Cleanest Housing Rate Trade

Lennar is the second-largest US homebuilder by closings, with a strategy built around volume and incentives.

The company has used mortgage rate buydowns of 100 to 300 basis points and price discounts more aggressively than any peer.

That strategy compresses gross margin in a high-rate environment and expands it dramatically when rates drop. The math is the entire thesis.

Q4 fiscal 2025, reported December 16, 2025, posted adjusted EPS of $2.03 against pre-earnings consensus running between $2.21 and $2.23, a miss of roughly 8 to 9% depending on the source. GAAP EPS of $1.93 was weighed down by a one-time $156 million loss on the Millrose Properties exchange offer.12

Q1 fiscal 2026, reported March 12, 2026, posted net earnings per diluted share of $0.93, missing consensus of roughly $0.95 by about 2%; excluding mark-to-market gains on technology investments, EPS was $0.88, a roughly 7% miss.

The two-quarter miss has driven the stock to a 52-week low of $83.03 on April 2.

At $94.05 the stock trades at roughly 12.9x trailing earnings, about 1.05x book, and 0.7x sales. The dividend yield is 2.1% and total-debt-to-equity, defined as long-term plus short-term debt divided by total stockholders' equity, is near 0.20.

Sell-side conviction on the long side is washed out. Recommendation skew leans hold-to-sell, with a recommendation mean reading of 3.4 (where 3 is hold and 4 is underperform).

The analyst pool puts the median 12-month target at $92, just below current price, and the Street high at $137, set by UBS's John Lovallo on December 18, 2025.

If Kalshi's roughly 60% probability of at least one 2026 cut is right, Lennar's incentive load drops, gross margin recovers, and the bearish consensus reverses.

The catalyst is the next quarterly print in mid-June and the June FOMC dot plot.

BXP Inc (BXP). The Office REIT Setup

BXP is the largest publicly traded developer and owner of Class A office properties in the United States, concentrated in Boston, New York, San Francisco, and Washington.

The post-pandemic office trade is over. The current trade is duration and refinancing risk.

BXP carries debt-to-equity of about 3.4x, typical for a REIT but punishing in a high-rate world. The stock hit a 52-week low of $49.72 on March 9.

Current price $57.73 reflects a partial recovery but is still 14.4% below year-start. The forward dividend yield, based on the current $0.70 quarterly distribution annualized, is roughly 4.85%, well above the 10-year Treasury.

Q4 2025 FFO per share came in at $1.76, missing the Zacks consensus of $1.80 by about 2%, and full-year 2025 FFO of $6.85 lagged consensus of $6.90 and prior-year FFO of $7.10.

The miss reflected non-cash straight-line rent reserves on two clients and higher G&A.

The bull case is not that operating performance is crushing expectations, it is that operating performance is roughly stable while the equity has priced in a refinancing and rate scenario the prediction markets do not believe.

The analyst setup is the cleanest contrarian read in this report. Recommendation skew leans buy, with a recommendation mean of 2.2 on the standard 1-to-5 scale where 2 is buy.13

The analyst pool puts the median 12-month target at $72.5 and the Street high at $89.

Median target $72.5 implies roughly 26% upside. Street-high target $89 implies roughly 54%.13

Rate cuts help BXP in two ways.

First, refinancing maturing debt at lower coupons. Second, cap rate compression directly increases NAV per share.

A 50-basis-point cut translates to roughly a 5 to 8% NAV uplift for premium office. That math is what the current price is ignoring.

LEN and BXP broke from SPY in February and bottomed within four weeks of the Iran ceasefire.

Year-to-date total return, January 2 to April 24, 2026.¹

The Counter-Argument

The thesis breaks if core PCE re-accelerates. The 3.0% February reading is sticky and shelter inflation has not collapsed.11

If services inflation excluding shelter prints above 3.5% for two consecutive months, the Fed will not cut regardless of who chairs it. Warsh told the Senate Banking Committee on April 21 that inflation is a choice and the Fed must take responsibility for it.9

In that scenario, Warsh inherits a hawkish reality and his early commentary forces commitments to inflation targeting. The Kalshi 60% probability would compress quickly toward CME's 27%.

Lennar carries idiosyncratic risk beyond rates. The company's incentive strategy implies its margins are structurally lower than D.R. Horton's or Toll Brothers'.

If buyers do not return even at lower rates, because credit standards have tightened or recession risk has risen, Lennar takes more pain than peers.

The two-quarter EPS miss is consistent with a deeper demand problem, not just an affordability problem.12

BXP carries refinancing risk that even cuts may not solve. Per the BXP Form 10-K for fiscal year 2025, filed with the SEC on February 27, 2026, and the Q3 2025 10-Q, the partnership has $1.0 billion of 2.750% senior unsecured notes maturing October 1, 2026, plus $100 million remaining on the 2024 Unsecured Term Loan due September 26, 2026.15

Refinancing at any rate above 5.5% reduces FFO regardless of whether the Fed cuts to 3.0% or 2.5%. CBRE's Q1 2026 San Francisco Office Figures put the SF overall vacancy at 30.4%; Cushman & Wakefield's Boston/Southern New Hampshire MarketBeat put Boston overall vacancy at 18.2% as of Q4 2025; JLL's Q1 2026 Manhattan and US Office Market Dynamics reports flagged the first leg of an office recovery cycle, with Manhattan posting 1.7 million square feet of positive absorption.16

Even with rate relief, secular work-from-home demand destruction is not fully priced into BXP's NAV.

The Warsh confirmation timeline remains a live variable.

With Tillis's hold lifted, the Banking Committee voting April 29, and Senate floor action expected within days, confirmation before May 15 is now plausible.

A procedural snag, whether Democratic delay tactics or additional Republican defections, could still push confirmation into June or later. If the September FOMC is still chaired by Powell or an interim, one cut in 2026 becomes physically harder to deliver.

The second-order risk is that prediction markets are simply wrong.

Kalshi traders priced 2024 election outcomes accurately, but rate-cycle predictions have a worse track record.

In 2025 the Fed started the year at 4.25 to 4.50% and held its target range at five consecutive meetings (January, March, May, June, and July) before delivering three back-to-back 25-basis-point cuts in September, October, and December, ending the year at 3.50 to 3.75%.

The actual 75 basis points of easing came in slightly above the 50-basis-point median projection from the December 2024 SEP and roughly tracked the path CME futures had converged on by mid-summer, after compressing repeatedly from more aggressive earlier-year pricing.

Prediction markets are noisy on Fed decisions because the base rate of Fed cuts is low and political-economy framing leaks into pricing.

CME's near-zero April-meeting cut probability of about 2% is a reminder that immediate-meeting odds can collapse even when full-year odds hold.2

Kalshi prices roughly 17% on three or more cuts, which is aggressive given current data.

The thesis still holds because the asymmetry is right. LEN at $94 with a $137 Street-high target and an $83 floor is roughly plus 46% upside versus minus 12% downside if the floor holds.

BXP at $58 with an $89 high target and a $50 floor is roughly plus 54% versus minus 14%. Even at lower probabilities than Kalshi implies, the expected value is positive.

Key Data Comparison

| Metric | LEN | BXP | XHB | XLRE | SPY |

|---|---|---|---|---|---|

| Current price | $94.05 | $57.73 | $108.45 | $43.83 | $713.94 |

| YTD return | -8.5% | -14.4% | +5.3% | +8.6% | +4.7% |

| 3-month return | -18.0% | -11.7% | -4.5% | +6.5% | +3.6% |

| 52-week high | $144.24 | $79.33 | n/a | n/a | n/a |

| 52-week low | $83.03 | $49.72 | n/a | n/a | n/a |

| 52-week low date | Apr 2, 2026 | Mar 9, 2026 | n/a | n/a | n/a |

| P/E TTM | 12.9x | 33.2x | n/a | n/a | n/a |

| P/B | 1.05x | 1.79x | n/a | n/a | n/a |

| Dividend yield | 2.1% | 4.9% fwd | n/a | n/a | n/a |

| Median target (FMP) | $92 | $72.5 | n/a | n/a | n/a |

| High target | $137 | $89 | n/a | n/a | n/a |

| Recommendation skew | Hold-to-sell | Buy | n/a | n/a | n/a |

Pricing, fundamentals, and analyst data sourced as cited in endnotes.

Catalyst Map

- April 28 to 29, 2026.FOMC meeting, with the April-meeting hold priced at roughly 98% on CME FedWatch and 99.7% on Polymarket. The press conference is the catalyst. Powell signaling openness to cuts lifts Kalshi probability and closes the LEN/BXP gap.

- A hawkish hold widens the gap and improves the entry.

- April 29, 2026.Senate Banking Committee vote on the Warsh nomination, scheduled for 10:00 AM. Committee approval clears Warsh for a full Senate vote.

- Early to mid May 2026.Expected full Senate confirmation vote on Warsh. With Tillis's hold lifted, confirmation before Powell's May 15 term-end is now plausible.3

- May 12, 2026.April CPI release at 8:30 AM ET. Energy reversal post-Iran ceasefire is the key variable. A headline print at or below 3.0% lifts Kalshi probability above 70%.11

- May 15, 2026.Powell term ends. Warsh likely transitions in as chair if confirmation has cleared.3

- June 16 to 17, 2026.FOMC meeting with new dot plot, the first that could include Warsh's vote.4

- June (date TBD), 2026.Lennar fiscal Q2 earnings, the quarter that incorporates the spring selling season. A second consecutive miss accelerates the bearish case. A beat with stable margin guidance reverses it.12

- July 28 to 29, 2026.FOMC meeting.

- Sep 26 to Oct 1, 2026.BXP debt refinancing window. The $100M remaining on the 2024 Unsecured Term Loan matures September 26, and $1.0B of 2.750% senior unsecured notes mature October 1. Refinancing coupons become the data point that confirms or breaks the cap rate compression thesis.15

Two rate-sensitive equities are priced as if Fed cuts will not happen, while Kalshi prices a roughly 60% probability they will, and the catalyst window has compressed into the next three weeks as the Warsh confirmation accelerates.

The thesis breaks if core PCE re-accelerates above 3.5% on services excluding shelter, or if confirmation slips past Powell's May 15 term-end and the September FOMC inherits a Powell or interim chair. The asymmetry holds because LEN sits 13% above its April 2 low with a $137 Street-high target, and BXP sits 16% above its March 9 low with sell-side recommendation skew already on the buy side at a 2.2 recommendation mean.

ProCap Insights is a research division of ProCap Financial. This report is for informational and analytical purposes only. It does not constitute investment advice and does not make buy, sell, or hold recommendations on any security. Nothing in this report should be construed as a solicitation or recommendation to buy or sell any financial instrument. Readers should conduct their own due diligence and consult a qualified financial advisor before making any investment decision.

Sources

- OpenBB Platform / Yahoo Finance equity quote and historical price endpoints, queried April 26, 2026 (LEN, BXP, XHB, XLRE, SPY, KRE, TAN, TLT). 52-week ranges and closing prices verified end of session April 24, 2026.

- CME FedWatch Tool, April 24, 2026 snapshot. CME, “FedWatch Tool,” cmegroup.com. Distribution coverage via Bitcoin News, “Federal Reserve Set to Hold Rates at 3.75% as Traders Price 99% Odds for April 29 FOMC,” April 24, 2026.

- CNBC, “Tillis ends block of Fed chair nominee Warsh, clears way for Trump pick,” April 26, 2026, cnbc.com. Senate Banking Committee Executive Session schedule, banking.senate.gov. Coverage of full Senate vote timeline via Washington Examiner, April 26, 2026.

- Federal Reserve, March 18, 2026 Summary of Economic Projections, federalreserve.gov.

- Kalshi public market data, “Number of rate cuts in 2026?” (KXRATECUTCOUNT-26DEC31), queried April 26, 2026, kalshi.com.

- Polymarket, “How many Fed rate cuts in 2026?” polymarket.com; “Fed rate cut by …” market series, queried April 2026.

- Goldman Sachs, “The Outlook for Fed Rate Cuts in 2026,” goldmansachs.com; Morgan Stanley, “2026 US Economics Outlook: Emerging From Policy Uncertainty,” November 2025; JPMorgan, Michael Feroli rate forecast commentary, January 2026 (CNBC, “‘Pretty weak’ case for Fed rate cuts in the near-term, says JPMorgan’s Michael Feroli,” January 14, 2026).

- Kevin Warsh, Wall Street Journal op-ed, November 2025 (on AI as a disinflationary force and Fed balance sheet reduction); Kevin Warsh, Wall Street Journal op-ed, fall 2024 (criticizing Powell-era policy choices); Kevin Warsh, “Commanding Heights: Central Banks at a Crossroads,” G30 Spring Lecture at the IMF, April 25, 2025, hosted at hoover.org; Hoover Institution interview, “Inflation Is A Choice: Kevin Warsh On Fixing The Federal Reserve,” hoover.org.

- CNBC, “Kevin Warsh hearing takeaways,” April 21, 2026, cnbc.com; CNN Business, “Fed chair nominee Kevin Warsh vows not to be Trump’s ‘sock puppet’,” April 21, 2026.

- CNBC, “US oil price plunges below $84 as Iran declares Strait of Hormuz open, easing supply fears,” April 17, 2026; CNBC, “A timeline of how the Iran war shook oil prices,” April 21, 2026.

- US Bureau of Labor Statistics, Consumer Price Index Summary, March 2026 (released April 10, 2026), bls.gov; BLS Schedule of Releases for the Consumer Price Index (April 2026 CPI scheduled May 12, 2026); BEA Personal Consumption Expenditures Price Index data, bea.gov.

- Lennar Corporation, “Lennar Reports Fourth Quarter and Fiscal 2025 Results,” December 16, 2025, newsroom.lennar.com; Zacks via Nasdaq, “Lennar Q4 Earnings Miss Estimates, Revenues Beat, Stock Down,” December 17, 2025 (Zacks consensus $2.23); Investing.com earnings call transcript, “Lennar’s Q4 2025 results miss EPS forecasts, stock drops,” December 16, 2025 (consensus $2.21); Lennar Corporation, “Lennar Reports First Quarter 2026 Results,” March 12, 2026, newsroom.lennar.com; OpenBB / FMP equity_fundamental_historical_eps endpoint, queried April 26, 2026.

- Primary citation: OpenBB Platform / Financial Modeling Prep (FMP) equity_estimates_consensus and equity_estimates_price_target endpoints, queried April 26, 2026 (LEN target_high $125 from FMP consensus; Street-high $137 from John Lovallo, UBS, December 18, 2025, lowered from $161). Cross-reference: OpenBB Platform / Yahoo Finance equity_estimates_consensus, queried April 26, 2026 (LEN median $89, BXP median $68). Recommendation mean: LEN 3.4 (hold-to-sell), BXP 2.2 (buy).

- Boston Properties, “BXP Announces Fourth Quarter and Full Year 2025 Results,” January 27, 2026, ir.bostonproperties.com; Nasdaq, “Boston Properties (BXP) Q4 FFO and Revenues Lag Estimates,” January 28, 2026; full audited operating results in BXP Form 10-K for fiscal year 2025, sec.gov.

- BXP Inc Form 10-K for fiscal year ended December 31, 2025, filed with the SEC on February 27, 2026 (accession 0001037540-26-000006), sec.gov (filing index here); BXP Form 10-Q for the quarter ended September 30, 2025, filed November 7, 2025 (accession 0001037540-25-000013), sec.gov (filing index here). Debt note discloses $1.0 billion of 2.750% senior unsecured notes due October 1, 2026, and $100 million outstanding on the 2024 Unsecured Term Loan due September 26, 2026. Cross-reference: BXP Q1 2025 Supplemental Operating and Financial Data, investors.bxp.com.

- CBRE, “San Francisco Office Figures Q1 2026,” cbre.com; JLL, “U.S. Office Market Dynamics, Q1 2026,” jll.com; JLL, “New York Office Market Dynamics, Q1 2026,” jll.com; Cushman & Wakefield, “Boston/Southern New Hampshire MarketBeats,” cushmanwakefield.com; Cushman & Wakefield, “New York City Area MarketBeats,” cushmanwakefield.com.

- Freddie Mac Primary Mortgage Market Survey, “The 30-Year Fixed-Rate Mortgage Declines Further,” week ending April 23, 2026, freddiemac.gcs-web.com (PMMS series).

- Federal Reserve daily target-range data via OpenBB Platform / federalreserve.gov effective federal funds rate series, queried April 26, 2026 (target_range_upper / target_range_lower transitions documenting cuts effective September 18, 2025; October 30, 2025; and December 11, 2025); Federal Reserve, “FOMC Statement,” September 17, 2025, October 29, 2025, and December 10, 2025, federalreserve.gov; Federal Reserve, December 18, 2024 Summary of Economic Projections, federalreserve.gov (2025 year-end median dot at 3.75–4.00%, implying 50 basis points of 2025 cuts from year-start 4.25–4.50%).