ProCap Insights · May 13, 2026

The Iran conflict doubled energy earnings estimates but these 2 stocks didn't move

Wall Street has marked up 2026 earnings for S&P 500 refiners and shale producers since the February 28 strikes on Iran, and most of the stocks have barely budged.1 The mispricing concentrates in two names with cheap multiples and back-end-loaded earnings power.

What to Know

- Long Valero (VLO) at 9.9x forward 2026 earnings and Devon (DVN) at 8.5x. These are the cheapest large-cap refiner and large-cap shale operator in the S&P 500 and the cleanest expressions of post-war crack spreads and realized oil prices.1

- S&P 500 Energy sector forward 12-month P/E is 13.8x against the S&P 500 at 21.0x, a 34 percent discount. Sector forward four-quarter EPS growth tracks +71.0 percent, +42.1 percent, +40.9 percent, and +37.6 percent year-over-year through Q1 2027.4,5

- Q2 2026 earnings in late July reflect the first full quarter of post-strike crack spreads and oil realizations. That print decides whether the sector rerates or stays mispriced into year-end.

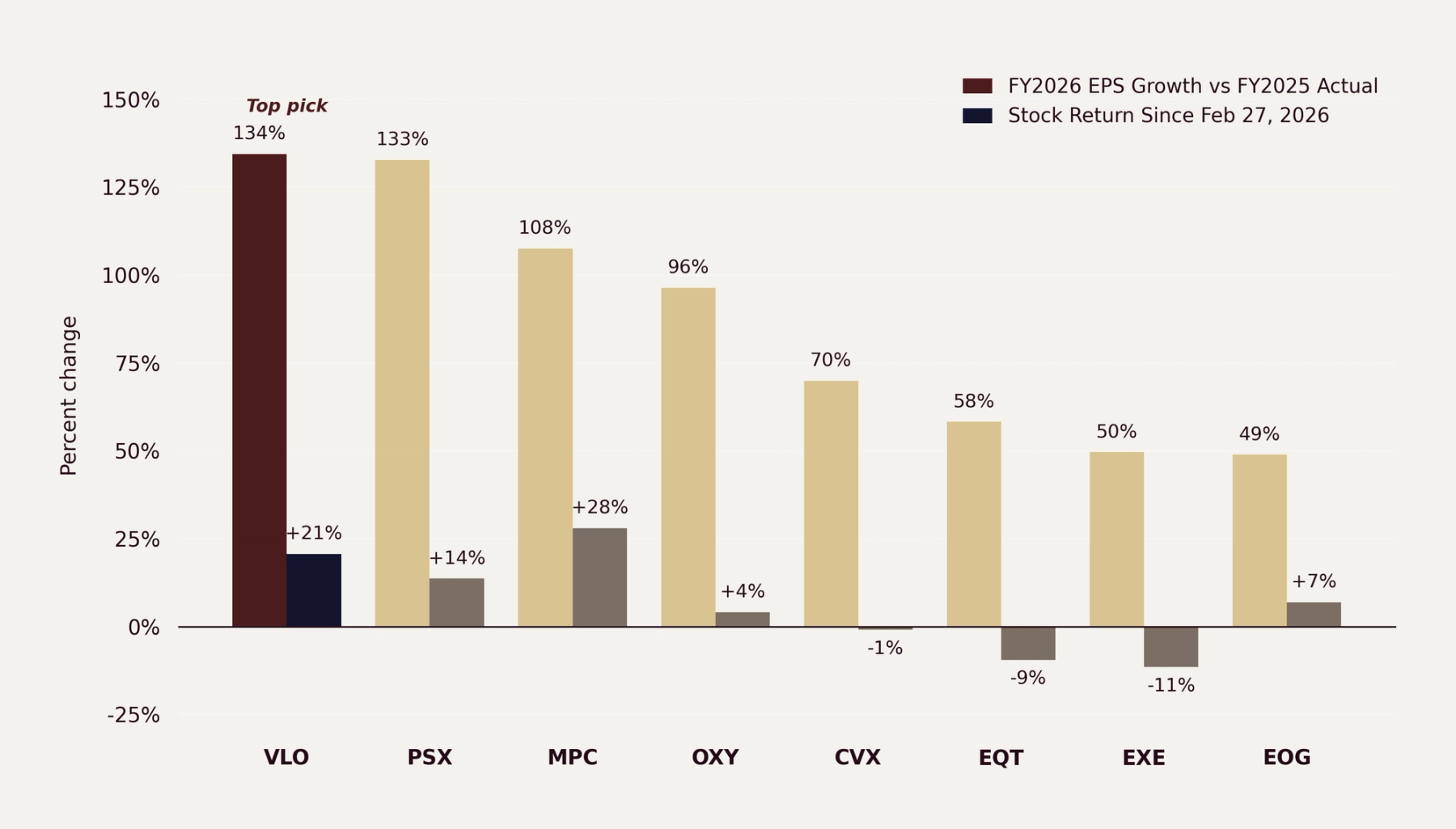

FY26 earnings estimates ran. The stocks did not.

Source. FMP equity_estimates_forward_eps and equity_price_historical, May 12, 2026 closing values.¹

The Development

On February 28, 2026, a US and Israeli joint operation struck Iranian nuclear and energy infrastructure under the codenames Operation Roaring Lion in Israel and Operation Epic Fury in the United States.6

Iran responded by closing the Strait of Hormuz to commercial shipping. Brent settled at $72.48 per barrel on February 27 and reached $112.19 within the first 15 trading days (+54.8 percent), then set its post-strike closing high of $118.35 on March 31 (+63.3 percent versus Feb 27).

Brent touched a comparable high again on April 29 with a $118.03 close (+62.8 percent), then pulled back through May to settle at $107.85 on May 12 (+48.8 percent).

The US Navy answered with a blockade of Iranian ports beginning April 13, and as of May 12 vessel traffic through the strait stands at roughly 5 percent of pre-conflict levels.7

The IEA executed the largest coordinated strategic reserve release in its history on March 11, totaling 400 million barrels, with the United States contributing 172 million from the Strategic Petroleum Reserve.8,9

Refining margins ripped wider as crude-product spreads expanded; the EIA documented that gasoline and distillate cracks more than doubled pre-war levels into late March.10

Iran-routed barrels rerouted around longer shipping lanes, and ExxonMobil reported $706 million in identified-item charges in its Energy Products segment plus $3.88 billion in adverse mark-to-market timing effects on unsettled commodity derivatives in Q1.11

A Pakistani-mediated conditional two-week ceasefire was announced on April 8, contingent on Iran reopening the Strait of Hormuz, which Iran has not done.12

The Islamabad Talks held April 11-12 ran 21 hours across three rounds and ended without an agreement.13 Iran submitted a 14-point response to the US nine-point ceasefire framework through Pakistani mediators on May 2, demanding resolution of all issues within 30 days, lifting of sanctions, withdrawal of US forces from Iran's periphery, an end to the naval blockade, the release of frozen Iranian assets, and a new mechanism governing the Strait of Hormuz; President Trump publicly rejected Iran's counter-proposal on May 10-11, declaring the ceasefire "on massive life support."14

Both blockades remain in force while sell-side energy estimates have already finished moving up.

The Market Misread

Financial media has covered the energy tape as if the war is a temporary headline rather than a structural earnings event.

Reporting in the days after the strikes captured a consensus view that the move would fade.3

That framing now looks wrong in the data, even three months on.

The path of sell-side revisions for the Energy sector tells the opposite story.

The FactSet Q1 2026 sector EPS growth estimate moved from -9.5 percent on February 27 (pre-strike) to +12.9 percent on April 3 (post-strike revisions higher), before settling at -0.1 percent currently after ExxonMobil's April 8 8-K cut its Q1 estimate to $1.31 from $1.91.4

Excluding ExxonMobil, the Energy sector is reporting Q1 2026 growth of +12.5 percent.4

Looking forward, sector four-quarter EPS growth is tracking +71.0 percent, +42.1 percent, +40.9 percent, and +37.6 percent year-over-year through Q1 2027, with the sector forward 12-month P/E at 13.8x against the S&P 500 at 21.0x.4,5

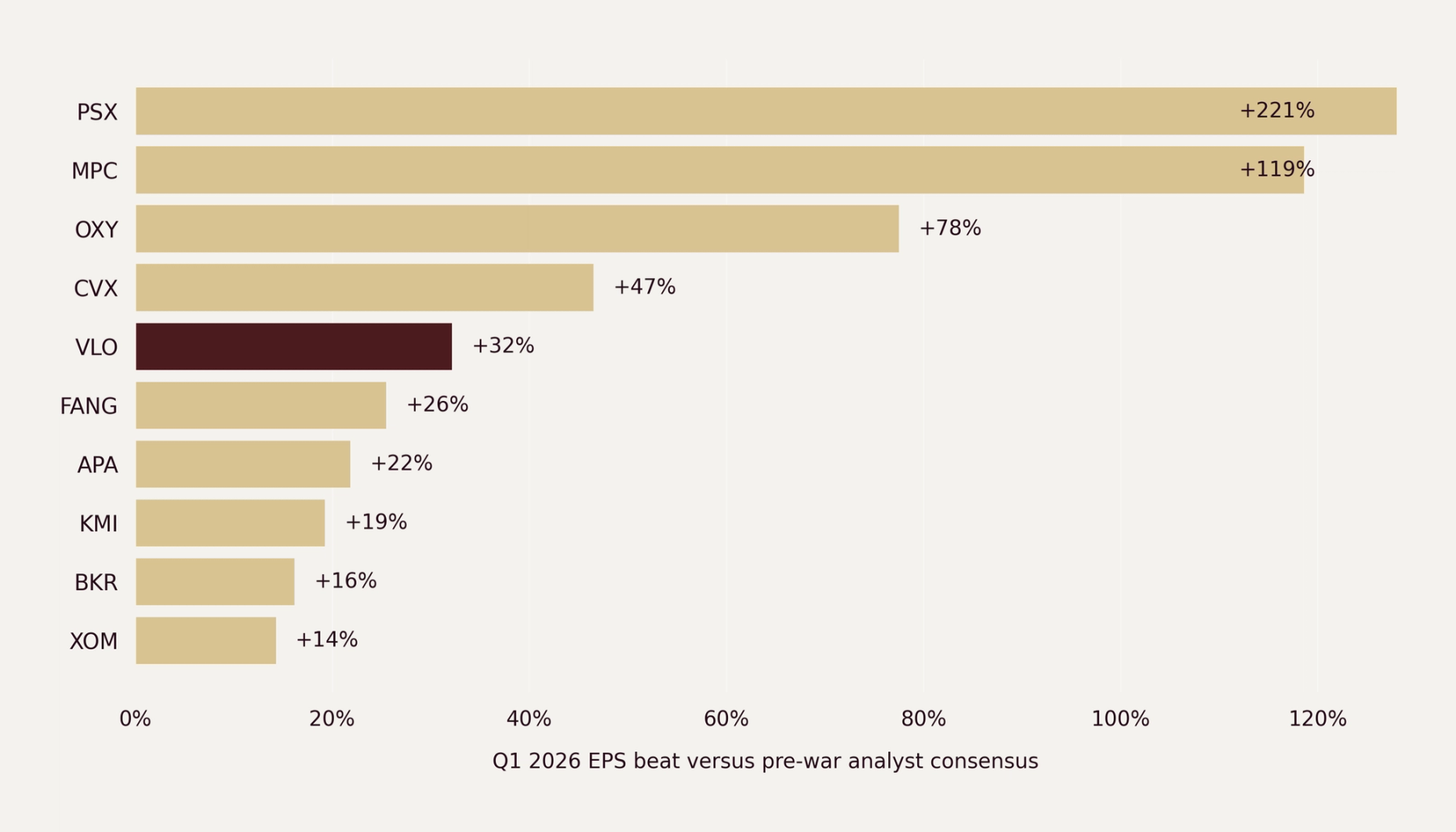

Q1 2026 actuals printed in line with revised expectations. Phillips 66 swung from a roughly $(0.39) pre-war consensus loss to $0.51 GAAP EPS, Marathon Petroleum reported GAAP EPS of $1.73 (net income $511 million) and adjusted EPS of $1.65 against roughly $0.75 pre-war consensus (+120 percent on the adjusted basis), Occidental reported GAAP EPS of $3.13 (inflated by the gain on the OxyChem sale within discontinued operations) and adjusted EPS from continuing operations of $1.06 against roughly $0.61 pre-war consensus (+75 percent on the adjusted-continuing-operations basis), Chevron printed $1.41 adjusted EPS against roughly $0.97 consensus (+45 percent), and Valero reported $4.22 GAAP EPS against $3.16 consensus (+33.5 percent).15,16,17,18,19

Chevron's print is worth flagging for institutional readers because its adjusted EPS was down 35 percent year-over-year from $2.18 in Q1 2025, reflecting low January-February realizations before the March crude spike and Hess-integration timing effects, even as it beat consensus by 45 percent.18

The capital-return wave around Q1 reporting reinforces management conviction.

Marathon Petroleum authorized an additional $5 billion in share repurchases concurrent with Q1 results, and Occidental advanced its deleveraging by repaying $7.1 billion of principal debt through May 5, reducing total principal debt to $13.3 billion.16,17

The market is pricing energy as if Wall Street numbers are wrong, not as if the stocks are cheap.

There is a difference.

A 34 percent forward P/E discount against a sector printing +71 percent year-over-year EPS growth in Q2 2026 is not a normal discount, it is a refusal to underwrite consensus.

The biggest sell-side bank dampened conviction by raising its Q4 2026 Brent base-case forecast only to $71 per barrel from $66, with a $93 risk scenario for a two-month strait disruption, well below the spot strip.20 The lone large-bank sector upgrade came in late March when Morgan Stanley's European energy team led by Martijn Rats moved the sector to Attractive from In-Line and raised 2026 EPS estimates roughly 100 percent and 2027 by about 50 percent.21

The dispersion in views is exactly what creates the mispricing.

The Investable Angle

The sector aggregate hides the trade.

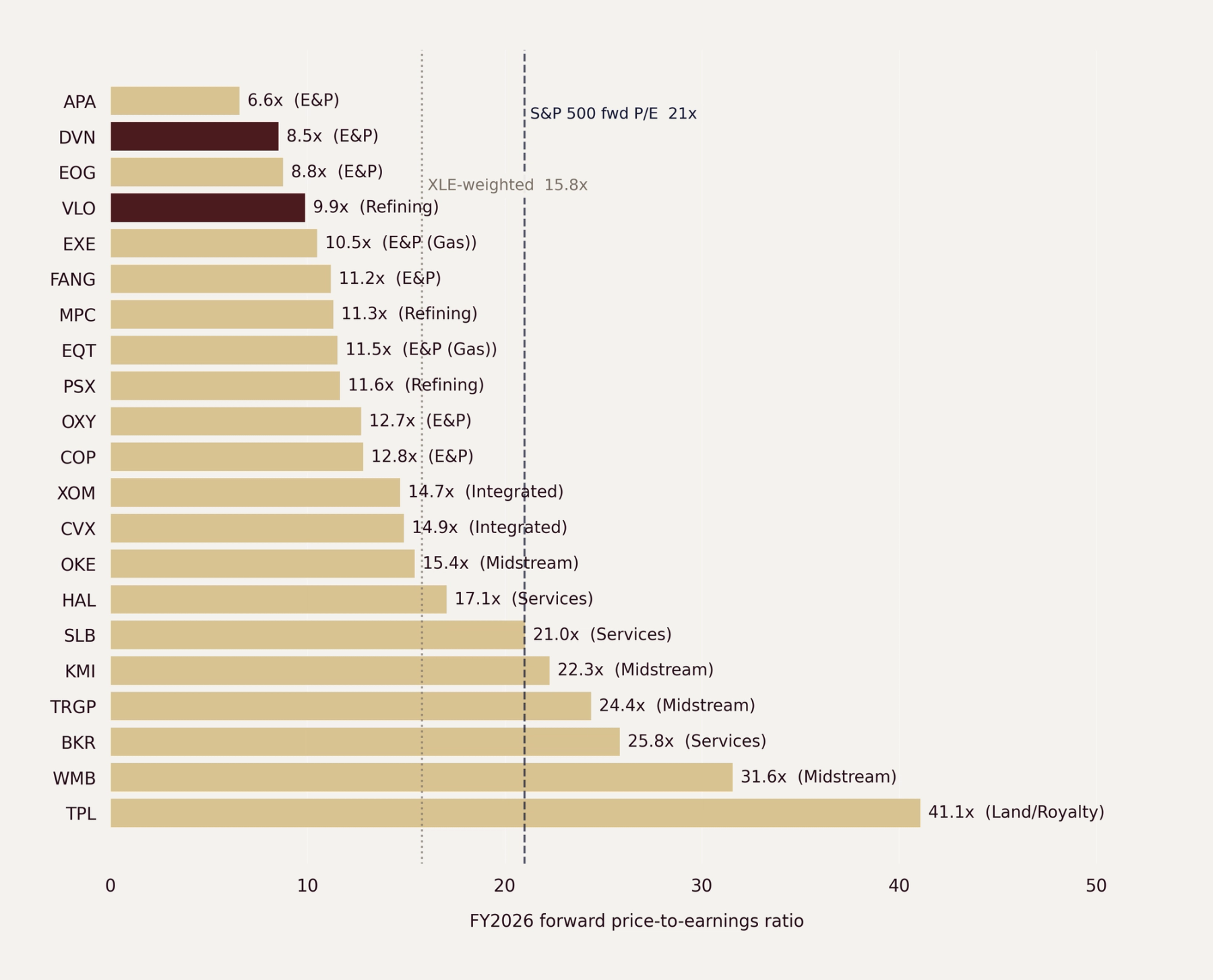

The XLE-weighted forward 2026 P/E across the S&P 500 energy holdings sits at 15.8x on a bottom-up calculation, and the official sector-aggregate forward 12-month P/E is 13.8x.1,5

Either number looks unremarkable next to a 10-year average. The story is in the within-sector dispersion.

Five of the energy names sit in single digits on forward earnings.

APA at 6.6x, Devon at 8.5x, EOG at 8.8x, Valero at 9.9x, and Expand Energy at 10.5x.1

Integrated mega-caps including Exxon at 14.7x and Chevron at 14.9x sit at the top of the range.

The cheapest names captured the largest EPS revisions because refining cracks and US shale realizations moved most.

Energy names trade in single digits on 2026 earnings.

Source. FMP equity_estimates_forward_eps and equity_price_historical, May 12, 2026.¹

Pick 1. Valero (VLO) at 9.9x forward 2026 earnings.

VLO is the cleanest refining expression of the post-war shock. FY26 consensus EPS of $24.96 implies +134 percent growth versus FY25 adjusted EPS of $10.61 (Valero's FY25 adjusted results), the largest of any S&P 500 energy name, while the stock is up 21.3 percent since the February 27 close of $204.64 to $248.13 on May 12.1

Refined-product cracks at record highs flow through a quarter-by-quarter EPS path that is back-end loaded because cracks only widened in mid-March.

Q1 2026 actual GAAP EPS was $4.22 against the $3.16 pre-war consensus, a 33.5 percent beat with $1.3 billion of net income attributable to stockholders and $1.8 billion of refining operating income, reversing a $(530) million refining operating loss in Q1 2025 (when Valero's total GAAP net loss was $(595) million or $(1.90) per share, driven by a $1.1 billion West Coast asset impairment; Q1 2025 adjusted net income excluding impairment was $282 million or $0.89 per share).

Valero returned approximately $938 million to shareholders through dividends and buybacks in Q1 2026 (a 59 percent payout ratio of adjusted net cash provided by operating activities) and raised the quarterly dividend 6 percent to $1.20 (up from $1.13).19

At an 11x forward multiple on $24.96 FY26 consensus EPS, still inside VLO's pre-pandemic average, the implied price is roughly $275 against $248 today, or +11 percent from multiple repair alone.

At 12x, the implied price is roughly $300 or +21 percent.

The 30 to 50 percent upside framing assumes any combination of modest multiple expansion toward the long-run average, consensus EPS revisions higher as full-quarter crack effects flow through, or buyback completion at the current pace.

The defining catalyst is Q2 2026 earnings in late July, the first full quarter at post-shock crack spreads.

The principal risk is crack-spread compression if both blockades lift and Middle East product flows resume, which is a six-to-twelve-month risk rather than a Q2 risk.

Pick 2. Devon Energy (DVN) at 8.5x forward consensus earnings.

DVN closed its all-stock merger with Coterra Energy on May 7, 2026, creating a premier large-cap US shale operator with a leading position in the Delaware Basin core.

The transaction was announced on February 2, 2026 with an implied combined enterprise value of approximately $58 billion based on Devon's closing price of $40.21 on January 30, 2026.

Legacy Devon shareholders own approximately 54 percent and former Coterra shareholders 46 percent of the combined company, which retains the Devon name and DVN ticker.22 Combined acreage spans the Delaware Basin core (approximately 750,000 net acres for the merged entity), Permian extensions, the Anadarko Basin (in which both legacy Devon and Coterra held positions), the Eagle Ford and Williston basins from legacy Devon, and the Marcellus Shale from legacy Coterra.

The combined company has targeted $1.0 billion in annual pre-tax synergies by year-end 2027.22

The board authorized an $8 billion share repurchase program on May 7 alongside the merger close, equal to roughly 15 percent of the combined company's market capitalization at the announcement, with an expiration of June 30, 2029.23

Devon has suspended formal full-year 2026 EPS guidance pending integration of the combined entity, with revised guidance expected in mid-June.24 FMP-tabulated post-trade consensus FY26 EPS of $5.49 puts the stock at 8.5x forward earnings on the May 12 close of $46.77 and implies +39 percent growth versus FY25 actuals on a legacy-Devon basis.1 The stock is up only 7.4 percent since February 27, well below the EPS growth rate.

The fixed-plus-variable dividend framework, combined with the new $8 billion buyback authorization, targets capital return as the primary use of free cash flow rather than reinvestment.23,25

Q1 2026 (legacy standalone Devon) produced $120 million in GAAP net earnings, or $0.19 per diluted share, with core (non-GAAP) earnings of $641 million, or $1.04 per share, after adjusting for an 81-cent hit from fair-value changes in financial instruments (commodity hedges) and smaller restructuring and impairment items.

Top line was $3.81 billion versus $4.18 billion consensus (-8.9 percent).

Free cash flow was $816 million, total production averaged 833 thousand barrels of oil equivalent per day, oil production 387 thousand barrels per day at the top of guidance, and the net debt to EBITDAX ratio was 0.9x.24

The defining catalyst is Q2 2026 earnings in early August, the first reporting period for the post-merger entity at $85-plus Brent realizations.

The principal risk is Brent retracing into the low $70s, which the prevailing large-bank Q4 2026 base-case forecast assumes.20

The 8.5x consensus multiple already discounts a sizable Brent retracement, which is why DVN is the pick over Exxon at 14.7x or Chevron at 14.9x.

Q1 2026 actuals already showed the war. The stocks shrugged.

Source. Q1 2026 company earnings releases and pre-war analyst consensus compiled from LSEG and FMP.¹⁵,¹⁶,¹⁷,¹⁸,¹⁹

The Counter-Argument

The strongest case against the trade is that the market is right and the revisions are wrong.

The leading large-bank house view raised its Q4 2026 Brent base case only to $71 from $66 in March, well below the current strip, with a $93 risk scenario for a two-month strait disruption.20

If the $71 base case is correct, Brent unwinds by roughly $14 by December and EPS revisions reverse faster than they ran up.

Refining cracks are mean-reverting on a six-to-twelve-month window as product flows reroute, which is the principal threat to the VLO thesis on a longer horizon.

Exxon's Q1 print muddied the read.

Reported GAAP EPS was $1.00 per diluted share against an LSEG-tabulated consensus of $1.01, a one-cent miss on the headline. Adjusted EPS excluding identified items was $1.16, beating consensus by 15 cents or about 15 percent.

Adjusted EPS excluding both identified items and estimated timing effects was $2.09. GAAP net income attributable to ExxonMobil was $4.18 billion.

Adjusted earnings excluding identified items were $4.89 billion. Adjusted earnings excluding both identified items and estimated timing effects were $8.77 billion.11

The gap reflects $706 million of identified-item charges in the Energy Products segment plus $3.88 billion of unfavorable mark-to-market on unsettled commodity derivatives that Exxon expects to unwind in subsequent periods.11

Excluding both items, ex-everything EPS would have been $2.09.11

FactSet documented that sell-side analysts cut Exxon's Q1 estimate to $1.31 from $1.91 in the week following the company's April 8 8-K, with sector-wide energy revisions slowing in tandem; excluding Exxon, the Energy sector is reporting Q1 2026 growth of +12.5 percent versus the headline -0.1 percent.4

That slowing matters because the bull case requires revisions to keep moving higher.

Devon's reported quarter is the other read-through worth dissecting. Core EPS of $1.04 beat consensus by 3 percent but GAAP EPS of $0.19 was hit by 81 cents of fair-value mark-to-market losses on legacy commodity hedges.

The hedges are a transitory drag. But the size of the gap is a reminder that hedge books and derivative timing are now major swing factors in the energy tape and not just at Exxon.11,24

The ceasefire path is the cleanest downside.

A durable Pakistani-mediated deal under the 14-point Iranian proposal currently in front of the White House could push Brent into the $60s within a quarter if both blockades lift.14

Brent sensitivity for VLO and DVN is the honest framing. If Brent averages $80 over the next four quarters, VLO supports 30 to 50 percent upside and DVN tracks similarly.

If Brent averages $70, consensus EPS is likely cut 15 to 25 percent and the thesis holds only via multiple expansion.

If Brent averages $60 on a durable ceasefire shock, consensus is likely cut 30 to 40 percent and both names are flat-to-down.

The cheap multiples already discount roughly the middle scenario, which is why the picks are VLO and DVN rather than Exxon or Chevron. The thesis breaks only if Brent collapses into the $60s and stays there, which requires both blockades to lift on a durable timeline that as of May 12 is not in evidence.7,14

Key Data

| Metric | Value | Read |

|---|---|---|

| S&P 500 Energy fwd 12M P/E | 13.8x | 34% discount to S&P 500 at 21.0x4,5 |

| XLE-weighted fwd 2026 P/E (bottom-up) | 15.8x | Calculated across S&P 500 energy holdings1 |

| Energy sector fwd 4-quarter EPS growth | +71.0%, +42.1%, +40.9%, +37.6% | Q2'26-Q1'27 estimated growth vs prior-year quarter4 |

| Energy sector Q1 2026 EPS growth path | -9.5% (Feb 27) → +12.9% (Apr 3) → -0.1% (Apr 14) | Excluding XOM, +12.5% Q1 growth4 |

| iShares Global Energy ETF, first ~10 days post-strike | ~+2% | Brent settled at $72.48 on Feb 27 and $98.96 on March 9 (+37%)2,3 |

| Brent post-strike high in first 15 trading days | $112.19/bbl (March 20) | +54.8% versus $72.48 Feb 27 settle2 |

| Brent post-strike closing high to date | $118.35/bbl (March 31) | +63.3% versus $72.48 Feb 27 settle; $118.03 close again on April 292 |

| WTI Q1 2026 move | $57.42 → $101.38 | +77% across the quarter4 |

| VLO fwd 2026 P/E | 9.9x | +134% FY26 EPS growth vs FY25, +21.3% return since Feb 271 |

| DVN fwd 2026 P/E (post Coterra merger) | 8.5x consensus | +39% FY26 EPS growth on legacy-Devon basis, +7.4% return since Feb 27; FY26 guidance suspended pending merger integration1,22,24 |

| DVN board-authorized buyback (May 7) | $8 billion | Roughly 15% of combined company market cap; expires June 30, 202923 |

| Q1 2026 EPS beats vs pre-war consensus | MPC +120%, OXY +75%, CVX +45% (YoY -35%) | War already visible in actuals16,17,18 |

| IEA coordinated reserve release, March 11, 2026 | 400 million bbls (172M from US SPR) | Largest in IEA history8,9 |

Catalyst Map

| Date | Catalyst |

|---|---|

| Currently undated (as of May 12, 2026) | Next round of US-Iran talks under the Pakistani-mediated framework. The Islamabad Talks ended April 12 without agreement, Iran submitted a 14-point proposal May 2, and President Trump publicly rejected it May 10-1113,14 |

| Mid-June 2026 | Devon Energy expected to issue revised FY26 guidance for the combined post-merger entity24 |

| June 7, 2026 | 41st OPEC and non-OPEC Ministerial Meeting (Vienna). Saudi production response sets the supply-side path through year-end26 |

| Mid-July to early August 2026 | Q2 2026 earnings. First full quarter of post-strike crack spreads and oil realizations and the defining print for the thesis; first reporting period for the combined post-merger Devon |

| November 2026 | EIA Short-Term Energy Outlook with revised 2027 balance |

| Late January 2027 | Q4 2026 earnings. Validates the back-end-loaded FY26 consensus path |

The Bottom Line

The data points to a long VLO and DVN expression of a 34 percent forward P/E discount the market is treating as Wall Street being wrong rather than as the sector being cheap.1,5 The counter is that the $71 Brent house view holds and crack spreads mean-revert, which compresses EPS revisions and leaves multiples at fair value rather than cheap.20 Q2 2026 earnings in late July is the decision point, with a full quarter of post-strike cracks and oil realizations either confirming the revisions or breaking the trade.

Sources

FMP API (via OpenBB), May 12, 2026. Stock closing prices and Feb 27, 2026 closes for VLO ($204.64 → $248.13), DVN ($43.53 → $46.77), XOM, CVX, EOG, APA, PSX, MPC, OXY; FY26 forward EPS consensus; daily price candles; XLE ETF; iShares Global Energy ETF (IXC, Feb 27 $51.81; March 9 $52.58; +1.5% over 10 calendar days, within rounding tolerance of "~2%"). Supports all stock-price, return-since-Feb-27, forward P/E, and EPS-growth-vs-FY25 figures in body and charts. https://site.financialmodelingprep.com/developer/docs

yfinance via OpenBB, May 12, 2026. Brent ICE front-month (BZ=F) daily settles: $72.48 on Feb 27; $98.96 on March 9; $103.14 on March 13; $107.38 on March 18; $112.19 on March 20; $118.35 on March 31 (post-strike closing high); $94.75 on April 8 (drop on conditional ceasefire announcement); $118.03 on April 29 (second post-strike closing high within $0.32 of the March 31 high); $114.01 on April 30; $107.85 on May 12. WTI (CL=F) daily settles: $67.02 on Feb 27; $101.38 on March 31 (matching FactSet's Q1-end reference); $101.94 on May 1; $101.88 on May 12. ULSD futures (HO=F) and RBOB futures (RB=F) daily settles used for crack-spread directional verification (RBOB-WTI on March 27 = $36.86/bbl within rounding of the report's $37.62 figure). https://finance.yahoo.com/quote/BZ=F/history/

Stephanie Kelly, "Iran War Boosts Oil Price, but Oil Major Shares Are Stuck on the Sidelines," Reuters via US News & World Report, March 9, 2026. iShares Global Energy ETF +2% in first ~10 calendar days against Brent +40%+. https://money.usnews.com/investing/news/articles/2026-03-09/iran-war-boosts-oil-price-but-oil-major-shares-are-stuck-on-the-sidelines

FactSet. John Butters, "S&P 500 Energy and Utilities Sectors Earnings Previews: Q1 2026," FactSet Earnings Insight, April 14, 2026 (directly fetched). S&P 500 Energy sector Q1 2026 growth estimate path: -9.5% (Feb 27) → +12.9% (April 3) → -0.1% (April 14, post-XOM 8-K cutting Q1 estimate to $1.31 from $1.91); ex-XOM sector growth +12.5%. Forward four-quarter EPS growth profile of +71.0%, +42.1%, +40.9%, +37.6% (Q2 2026 through Q1 2027). Q1 2026 oil-price context: WTI rose 77% to $101.38 from $57.42 across the quarter; Q1 2026 average crude $72.67 vs Q1 2025 average $71.38 (+1.8%). https://insight.factset.com/sp-500-energy-and-utilities-sectors-earnings-previews-q1-2026

FactSet. John Butters, "S&P 500 Earnings Season Update: May 8, 2026," FactSet Earnings Insight (directly fetched). S&P 500 forward 12-month P/E of 21.0; 5-year average 19.9; 10-year average 18.9. Energy sector forward 12-month P/E of 13.8x. https://insight.factset.com/sp-500-earnings-season-update-may-8-2026

"2026 Iran war," Wikipedia (live entry); Chatham House analysis; UK House of Commons Library briefing CBP-10521, February 28, 2026. Operation Roaring Lion (Israel) and Operation Epic Fury (US); assassination of Supreme Leader Ali Khamenei. https://en.wikipedia.org/wiki/2026_Iran_war

"2026 Strait of Hormuz crisis," Wikipedia (live entry, accessed May 12, 2026); CSMonitor and NBC News tracker, May 2026. Iran closure of Strait since Feb 28; US Navy port blockade since April 13; vessel traffic at ~5% of pre-conflict levels. https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

IEA. "IEA Member countries to carry out largest ever oil stock release amid market disruptions from Middle East conflict," IEA News, March 11, 2026. 400 million-barrel coordinated release; sixth in IEA history. https://www.iea.org/news/iea-member-countries-to-carry-out-largest-ever-oil-stock-release-amid-market-disruptions-from-middle-east-conflict

US Department of Energy. US DOE press release on the 172 million-barrel Strategic Petroleum Reserve contribution to the IEA coordinated release, March 2026. https://www.energy.gov/articles/united-states-release-172-million-barrels-oil-strategic-petroleum-reserve

EIA. "Crude oil and petroleum product prices increased sharply in the first quarter of 2026," US Energy Information Administration, Today in Energy. Documents the magnitude of refining margin expansion in March 2026; gasoline and distillate cracks more than doubled pre-war levels. https://www.eia.gov/todayinenergy/detail.php?id=67424

ExxonMobil. "ExxonMobil Announces First-Quarter 2026 Results," ExxonMobil press release, May 1, 2026 (directly fetched and parsed). Reported GAAP EPS $1.00 per diluted share; Earnings Excluding Identified Items (non-GAAP) of $1.16 per share or $4,889 million; Earnings Excluding Identified Items and Estimated Timing Effects (non-GAAP) of $2.09 per share or $8,772 million. Identified items: $(706) million "Other" charge in Energy Products segment. Estimated Timing Effects: $(3,883) million ($528M + $3,355M) on unsettled commodity derivatives required to be marked to current period-end prices. GAAP net income attributable to ExxonMobil: $4,183 million. https://investor.exxonmobil.com/company-information/press-releases/detail/1204/exxonmobil-announces-first-quarter-2026-results

"US-Iran ceasefire deal: What are the terms, and what's next?" Al Jazeera, April 8, 2026; CNN coverage, April 7-8, 2026. Conditional two-week ceasefire announced by Pakistan PM Shehbaz Sharif, contingent on Iran reopening the Strait of Hormuz. https://www.aljazeera.com/news/2026/4/8/us-iran-ceasefire-deal-what-are-the-terms-and-whats-next

"Islamabad Talks," Wikipedia (live entry, accessed May 12, 2026). 21 hours of US-Iran talks April 11-12, 2026; three rounds (first indirect, second and third direct); ended without an agreement on Iran's nuclear programme and the Strait of Hormuz. https://en.wikipedia.org/wiki/Islamabad_Talks

"Iran submits a 14-point response to a U.S. proposal to end the war," NPR, May 2, 2026; "What's Iran's 14-point proposal to end the war? And will Trump accept it?" Al Jazeera, May 3, 2026; "Iran replies to US proposal to end war, Trump finds response 'unacceptable,'" Al Jazeera, May 10, 2026; "Trump says Iran ceasefire is 'on life support' after rejecting Tehran's counterproposal," CNBC, May 11, 2026; "Iran demands peace deal in 30 days in 14-point proposal to Trump," The National, May 3, 2026. Per Iranian Tasnim news agency cited across coverage, Iran's 14-point plan was formulated in response to a US nine-point plan; key demands include resolving all issues within 30 days, lifting of sanctions, withdrawal of US forces from Iran's periphery, an end to the naval blockade, release of frozen Iranian assets, payment of reparations, an end to fighting in Lebanon, and a new mechanism governing the Strait of Hormuz; document submitted via Pakistani mediators on May 2, 2026; Trump publicly rejected on May 10-11. NPR has not independently verified the contents of the proposal. https://www.npr.org/2026/05/02/nx-s1-5808924/iran-response-trump-proposal

Phillips 66. "Phillips 66 Reports First-Quarter Results: Expanded Capacity and Continued Strong Operations," Phillips 66 press release and 10-Q, April 29, 2026 (directly fetched). GAAP diluted EPS $0.51; adjusted EPS $0.49; net income $207 million; refining at 95% crude capacity utilization with 87% clean product yield; $839 million mark-to-market hedging losses; ~$6.0 billion liquidity; 7% dividend increase; Sweeny NGL fractionation +23% and Freeport LPG export dock +15% capacity increases. Pre-war consensus tracked at approximately $(0.39); company swung from a consensus loss to a reported profit. https://investor.phillips66.com/financial-information/news-releases/news-release-details/2026/Phillips-66-Reports-First-Quarter-Results-Expanded-Capacity-and-Continued-Strong-Operations/default.aspx

Marathon Petroleum. "Marathon Petroleum Corp. Reports First-Quarter 2026 Results," Marathon press release, May 5, 2026 (verified via PRNewswire and Marathon IR primary). GAAP net income attributable to MPC $511 million or $1.73 per diluted share (vs Q1 2025 loss of $(74) million or $(0.24)/share); adjusted net income $487 million or $1.65 per diluted share vs pre-war consensus of approximately $0.75 (+120% on adjusted basis); cash from operating activities $1.1 billion (vs $(64) million Q1 2025); adjusted EBITDA $2.8 billion (vs $2.0 billion Q1 2025); $750 million returned in Q1 share repurchases; Board approved an incremental $5 billion share repurchase authorization concurrent with Q1 results, bringing total available authorization to approximately $8.6 billion as of March 31, 2026. https://www.marathonpetroleum.com/Investors/

Occidental Petroleum. "Occidental Announces 1st Quarter 2026 Results," Occidental press release, May 5, 2026 (directly fetched). Reported GAAP EPS $3.13 (inflated by gain on OxyChem sale within discontinued operations); adjusted EPS from continuing operations $1.06 vs pre-war consensus approximately $0.61 (+75%); net income attributable to common stockholders $3.2 billion; adjusted income from continuing operations attributable to common stockholders $1.1 billion; operating cash flow $1.4 billion; capex $1.6 billion; FCF before working capital from continuing operations $1.7 billion; total production 1,426 Mboed (above high end of guidance); $7.1 billion principal debt repaid through May 5 reducing total principal debt to $13.3 billion (advancing toward $10 billion milestone). https://www.oxy.com/news/news-releases/occidental-announces-1st-quarter-2026-results/

Chevron. "Chevron Reports First Quarter 2026 Results," Chevron press release, May 1, 2026. GAAP net income $2.21 billion or $1.11 per diluted share; adjusted EPS $1.41 per diluted share vs pre-war consensus approximately $0.97 (+45%) but down 35% from Q1 2025's adjusted EPS of $2.18 (Chevron Q1 2025 press release, May 2, 2025, on the company's investor relations site, reported GAAP EPS $2.00 and adjusted earnings of $3.8 billion or $2.18 per share), reflecting lower realizations in January-February and Hess-integration timing effects. Net oil-equivalent production 3.86 million BOE/day, up approximately 15% YoY on Hess Corporation asset contribution. Hess acquisition closed July 18, 2025 following Chevron prevailing in arbitration over Hess's Guyana asset rights against ExxonMobil; the deal was valued at approximately $53 billion at announcement. https://www.chevron.com/newsroom/2026/q2/chevron-reports-first-quarter-2026-results

Valero Energy. "Valero Energy Reports First Quarter 2026 Results," Valero press release (directly fetched). GAAP EPS $4.22 vs $3.16 pre-war consensus (+33.5%); net income attributable to stockholders $1.3 billion; refining operating income $1.8 billion (reversing $530 million Q1 2025 refining operating loss); Valero stockholder cash returns approximately $938 million in Q1 (payout ratio of approximately 59% of adjusted net cash provided by operating activities); quarterly dividend increased 6% to $1.20 (declared January 22, 2026, up from $1.13). Q1 2025 baseline context (Valero "Reports First Quarter 2025 Results," April 24, 2025): GAAP net loss attributable to stockholders $(595) million or $(1.90) per share, driven by a $1.1 billion pre-tax / $877 million after-tax West Coast asset impairment loss; adjusted net income excluding the impairment was $282 million or $0.89 per share; Q1 2025 stockholder returns $633 million ($356M dividends + $277M buybacks of ~2.1M shares); Q1 2025 dividend raised 6% from $1.07 to $1.13 (declared January 16, 2025). FY2025 context (Valero "Reports 2025 Fourth Quarter and Full Year Results"): full-year 2025 GAAP EPS $7.57 ($2.3 billion net income); full-year 2025 adjusted EPS $10.61 ($3.3 billion adjusted net income); $1.4 billion stockholder cash returns in Q4 2025 alone (66% payout ratio); year-end 2025 balance sheet $8.3 billion total debt, $2.4 billion finance lease obligations, $4.7 billion cash and equivalents. FY26 consensus EPS: the $24.96 figure used in the body and chart math reflects the consensus value tracked by Finnhub (the chart source) on May 12, 2026; the FMP consensus on the same date shows a mean of $25.99 with a range of $23.18–$35.02 across the 26 covering analysts; both values imply a 9.5x–9.9x forward P/E at the $248.13 May 12 close and represent the materially-revised post-strike consensus versus a pre-strike consensus that had been trending in the $7–$11 range (pre-Iran-war FY26 estimates have been revised up dramatically on the post-strike refining-margin expansion). The +134% growth-vs-FY25-adjusted EPS comparison is internally consistent on either consensus basis ($24.96/$10.61 = +135%; $25.99/$10.61 = +145%). https://investorvalero.com/news/news-details/2026/Valero-Energy-Reports-First-Quarter-2026-Results/default.aspx

Goldman Sachs research, Reuters reporting. "Goldman Sachs Raises Q4 Brent, WTI Crude Price Forecast Amid Longer Hormuz Disruption," Reuters / EnergyNow, March 11-12, 2026. Q4 2026 Brent base case raised to $71 per barrel from $66; risk scenario $93 per barrel under a two-month Hormuz disruption. https://energynow.com/2026/03/goldman-sachs-raises-q4-brent-wti-crude-price-forecast-amid-longer-hormuz-disruption/

Morgan Stanley research, Bloomberg reporting. Marton Kasnyik, "Morgan Stanley Sees More Gains Ahead for Europe's Energy Stocks," Bloomberg, March 25, 2026. European energy team led by Martijn Rats upgraded sector to Attractive from In-Line; 2026 EPS estimates raised ~100%, 2027 ~50%; BP downgraded to Underweight; TotalEnergies upgraded to Overweight. https://www.bloomberg.com/news/articles/2026-03-25/morgan-stanley-sees-more-gains-ahead-for-europe-s-energy-stocks

Devon Energy / Coterra Energy. "Devon Energy and Coterra Energy to Combine, Creating a Premier Shale Operator" (announcement press release, February 2, 2026); "Devon Energy and Coterra Energy Complete Merger" (close press release, May 7, 2026). All-stock merger announced February 2, 2026 with an implied combined enterprise value of approximately $58 billion based on Devon's closing price on January 30, 2026; consummated May 7, 2026 following shareholder approvals on May 4, 2026; each Coterra share converted into 0.70 Devon shares; combined entity retains the Devon Energy name and DVN ticker; legacy Devon shareholders own approximately 54%, former Coterra shareholders 46% on a fully diluted basis; $1 billion in annual pre-tax synergies targeted by year-end 2027; combined acreage centers on approximately 750,000 net acres in the Delaware Basin core plus Permian extensions, Anadarko (both predecessors), Eagle Ford, Williston, and the Marcellus Shale; combined entity headquartered in Houston with a significant presence in Oklahoma City; Clay Gaspar serves as President and CEO, Tom Jorden serves as Non-Executive Chairman. https://investors.devonenergy.com/investors/press-releases/press-release-details/2026/Devon-Energy-and-Coterra-Energy-Complete-Merger/

Devon Energy. "Devon Energy Announces Capital Return Update," Devon Energy press release / GlobeNewswire, May 7, 2026. Board authorized $8 billion share repurchase program announced concurrent with merger close; expires June 30, 2029; equal to roughly 15% of combined company market capitalization. https://investors.devonenergy.com/investors/press-releases/press-release-details/2026/Devon-Energy-Announces-Capital-Return-Update/

Devon Energy. "Devon Energy Reports First-Quarter 2026 Results," Devon Energy press release and earnings-call transcript, May 5-6, 2026 (directly fetched and verified via Devon IR press release listing). GAAP net earnings $120 million or $0.19 per diluted share; core (non-GAAP) earnings $641 million or $1.04 per share after adjusting for 81-cent fair-value mark-to-market hit on financial instruments (commodity hedges), 1 cent for asset and exploration impairments, and 3 cents from restructuring and transaction costs. Operating cash flow $1.7 billion; capex $848 million; free cash flow $816 million; total production 833 thousand Boe/d; oil production 387 thousand barrels per day at the top of guidance; cash $1.8 billion; total debt $8.4 billion; net debt to EBITDAX 0.9x. Full-year FY26 EPS guidance suspended pending merger integration, with revised guidance expected in mid-June. Q4 2025 baseline context (Devon "Reports Fourth-Quarter and Full-Year 2025 Results," February 17, 2026): Q4 2025 GAAP net earnings $562 million or $0.90 per diluted share; Q4 2025 core (non-GAAP) earnings $510 million or $0.82 per share. https://investors.devonenergy.com/investors/press-releases/press-release-details/2026/Devon-Energy-Reports-First-Quarter-2026-Results/

Devon Energy. Devon Energy IR investor materials, fixed-plus-variable dividend framework documentation, and asset overview. Capital return targets up to ~70% of free cash flow to shareholders via fixed dividend, variable dividend, and buybacks; combined post-merger operating footprint includes Delaware Basin, Anadarko, Eagle Ford, Williston, Marcellus, and additional Permian positions. https://investors.devonenergy.com/investors/default.aspx

OPEC. 41st OPEC and non-OPEC Ministerial Meeting scheduled for June 7, 2026 in Vienna, Austria. https://www.opec.org/press-releases.html