ProCap Insights · May 4, 2026

Google suddenly took a lead against Nvidia in the race to $10 trillion

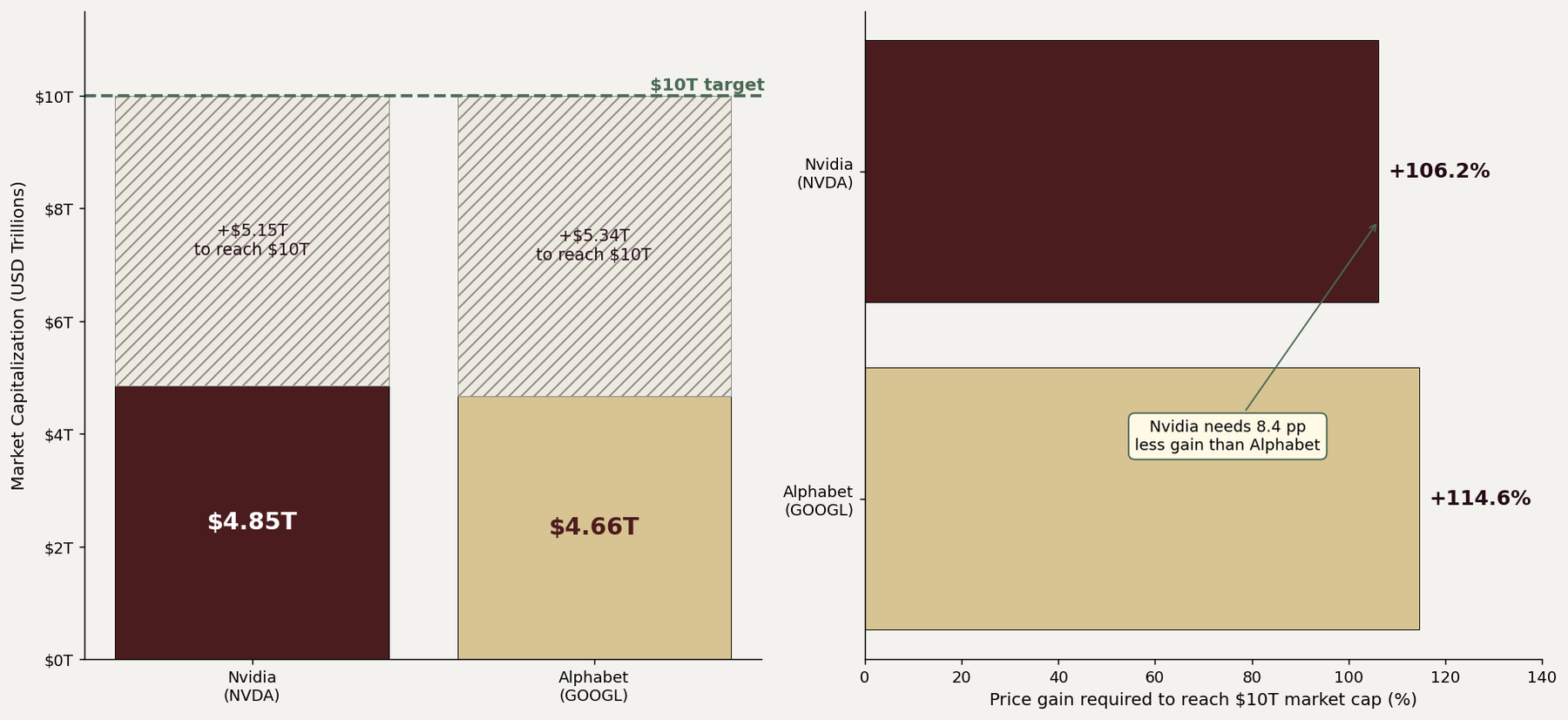

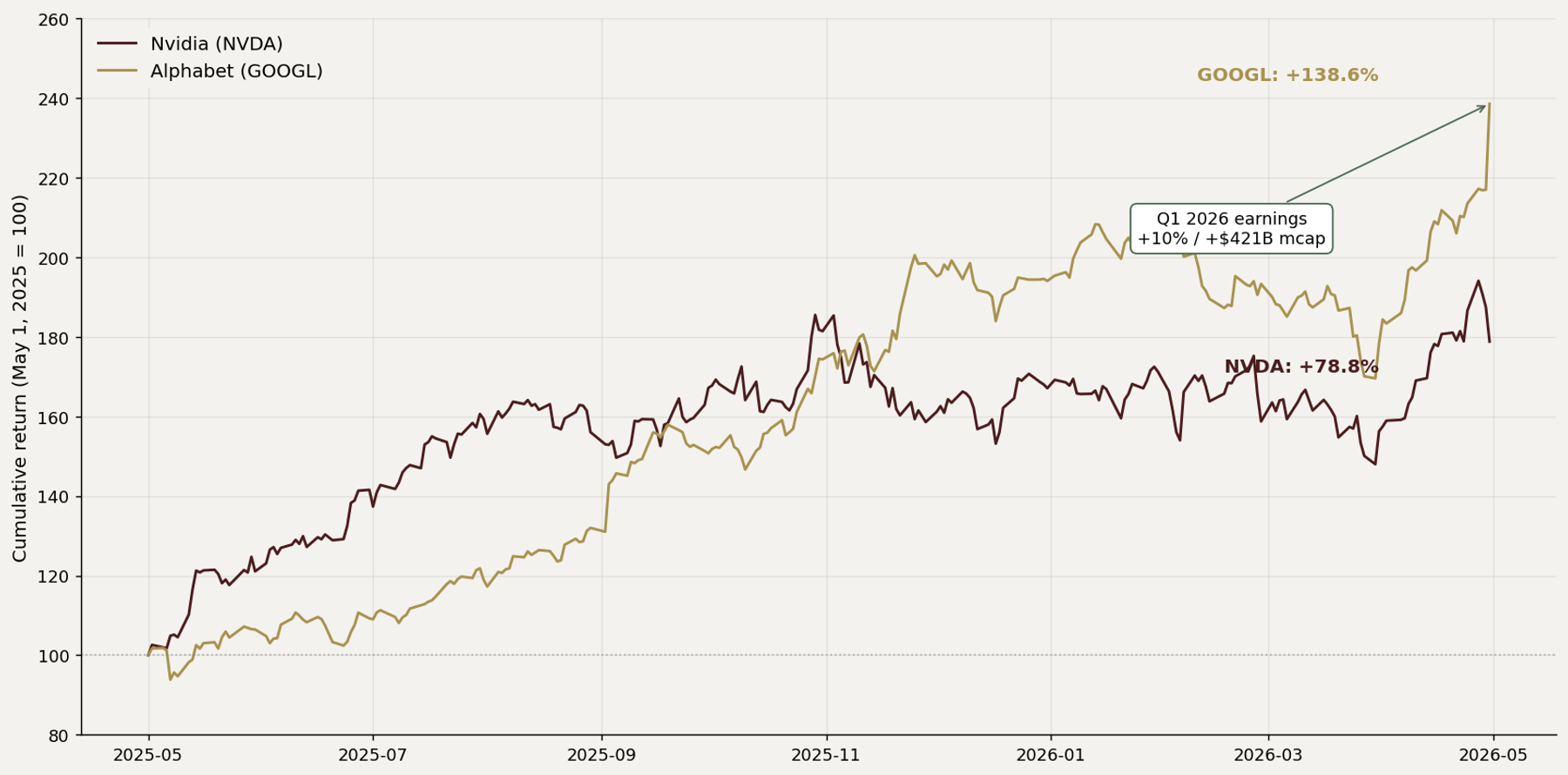

Alphabet added $421 billion in market cap on Thursday and reported Q1 2026 results that pushed Cloud growth to 63% and lifted contracted backlog to $460 billion in a single quarter.1,2 Nvidia still leads on market value by roughly $190 billion and needs less price appreciation to reach $10 trillion, but the math beneath the surface tells a different story.

What to Know

- The investable expression is long Alphabet (GOOGL) at 24x FY28 consensus EPS into the $10T race against Nvidia (NVDA) at 18x FY28. Alphabet has roughly 8 percentage points more price appreciation to cover, but its multiple has more room to expand on durable, diversified earnings.

- Alphabet’s Q1 2026 reported (GAAP) EPS of $5.11 versus a $2.64 consensus is flattered by a $36.9 billion unrealized gain on equity securities ($2.35 per share), driven primarily by writing up its roughly 14% Anthropic stake to the $350 billion February 2026 funding-round mark; adjusted EPS of about $2.76 was a 4.5% beat. The clean operating wins are Cloud revenue +63% to $20.0 billion, Cloud operating income up 3x to $6.6 billion, an 11th-consecutive quarter of double-digit total-revenue growth, and a Cloud backlog that nearly doubled quarter-on-quarter to over $460 billion.2

- Nvidia’s bull case rests on Blackwell and Rubin holding 75% gross margins through 2027 against more than $500 billion of disclosed revenue visibility, while its largest hyperscaler customers have ramped 2026 capex commitments to roughly $710–$725 billion combined and are simultaneously funding three credible non-Nvidia silicon programs.3,4 The forward look is whether Google’s TPU becomes a $50 billion external business by 2028 or stays a captive workload.

Both stocks are within 4% of each other and both need to roughly double to reach $10 trillion

Nvidia leads by roughly $190 billion (about 4%) and needs about 106% price appreciation. Alphabet needs about 115%. The gap matters less than where the earnings power compounds.⁵

The Knockout Punch

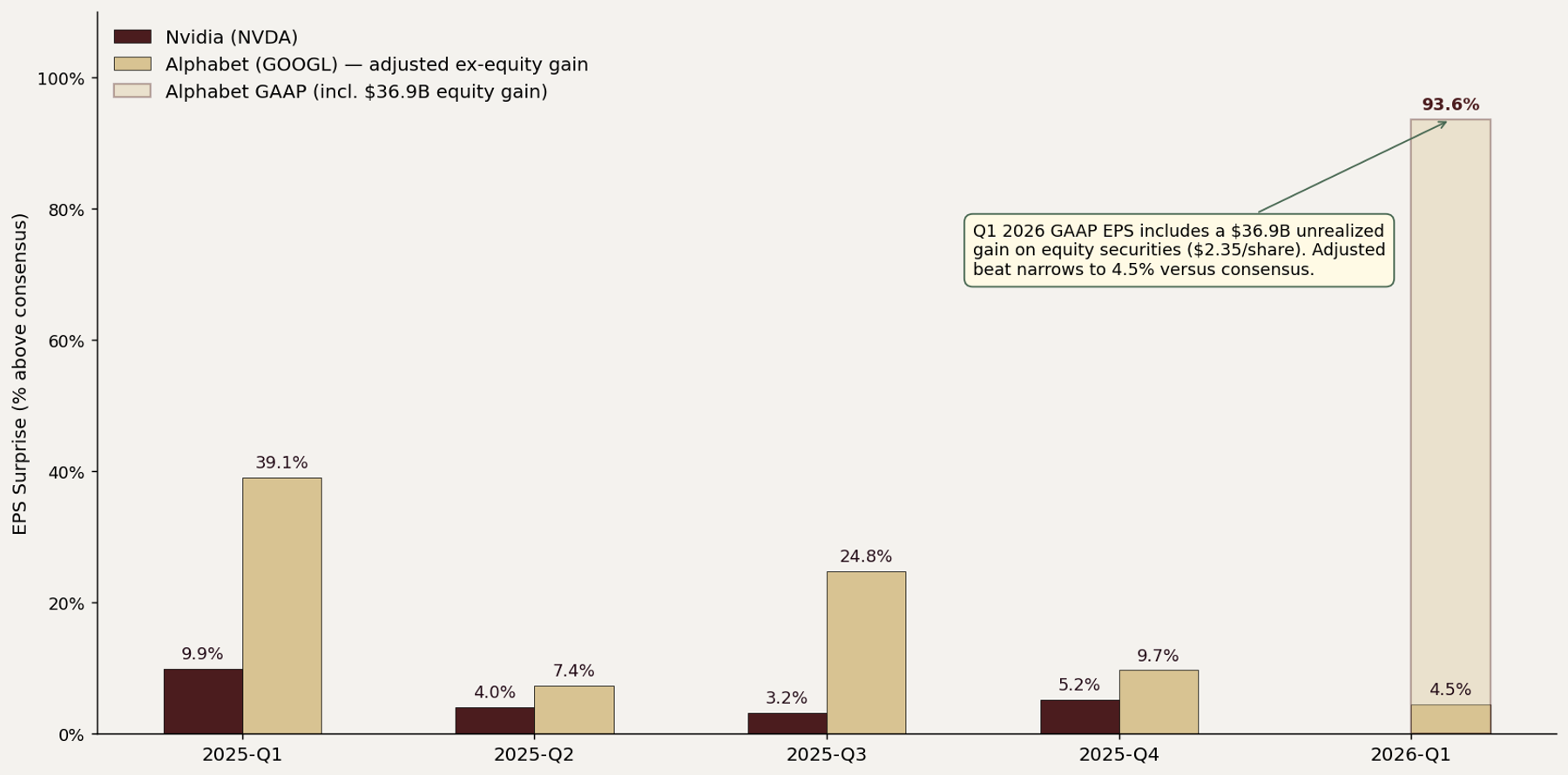

On April 29, 2026, Google reported Q1 2026 GAAP diluted EPS of $5.11.2 The headline figure is roughly double the $2.64 sell-side consensus, but $2.35 of the print came from a $36.9 billion unrealized gain on non-marketable equity securities; on an adjusted basis the beat narrows to about 4.5%.2,6 The cleaner story is operational.

The stock added $421 billion in market value the next session, the second-largest one-day market cap gain in U.S. equity history, behind only a previous Nvidia print.1

Alphabet shares rose 9.96% on a $4.2 trillion company, a move that historically only happens to much smaller names in the index.

Inside the print, the part that matters more than headline EPS is what happened to Cloud. Revenue grew 63% to $20.0 billion, segment operating income tripled to $6.6 billion, and backlog nearly doubled quarter-on-quarter to over $460 billion from roughly $239 billion at year-end 2025.2,7

Backlog is contracted future revenue, of which Alphabet expects just over 55% to be recognized as revenue over the next 24 months and the remainder thereafter.33

That number does not move that much in a single quarter unless customers are committing capital they were previously committing to someone else.

The someone else is Nvidia. Anthropic disclosed in October 2025 a multi-gigawatt expansion of its use of Google Cloud TPUs and tripled that compute commitment to roughly 3.5 gigawatts in April 2026.8,9 Meta is in advanced talks to deploy Google TPUs through Google Cloud in 2026 and outright in 2027.10

One year ago, a TPU partnership for frontier-model training outside Google’s own walls did not exist as a category.

Nvidia, meanwhile, watched its OpenAI investment commitment shrink from a $100 billion arrangement floated in September 2025 to a finalized $30 billion in early 2026, with Jensen Huang publicly calling the latter “might be the last” OpenAI investment.11

The bear case on circular AI financing did not get smaller in 2026. It got named.

To be balanced, Alphabet has its own circular-financing footprint: on April 24, 2026 Google committed up to $40 billion of new investment in Anthropic at the same $350 billion valuation that drove the Q1 equity-securities markup, while Anthropic in turn locked in 3.5 gigawatts of Google TPU capacity through Broadcom and saw its annualized revenue run-rate triple from $9 billion at year-end 2025 to $30 billion by April 2026.9,31,32

The unrealized markup that powered Alphabet’s headline EPS is paid for, in part, by Alphabet’s own incremental capital commitment to the same counterparty.

What Each Company Actually Does Today

Nvidia sells GPUs and the software that makes them programmable.

In Q4 fiscal 2026, data center revenue was $62.3 billion, or 91.5% of the $68.1 billion top line; for full-year FY26, data center was $193.7 billion or about 89.7% of $215.9 billion in total revenue.12 TTM gross margin sits near 71%, operating margin at roughly 60%, and return on equity at 104%.13 These are not normal numbers.

They are what happens when a single company supplies the only chip that works for the workload everyone wants to run.

The customer concentration is severe. Microsoft, Meta, Amazon, and Alphabet together account for an estimated 40% of Nvidia data center revenue, and their combined 2026 capex guidance now totals roughly $710–$725 billion (Microsoft ~$190B, Alphabet $180–$190B, Amazon ~$200B, Meta ~$135–$145B).4

If hyperscalers slow capex growth in 2027, Nvidia’s multiple compresses; if it grows further, Nvidia’s backlog and revenue keep extending.

Alphabet is five businesses sharing a balance sheet. Search, YouTube, Cloud, Android, and Other Bets including Waymo. Google Services, anchored by Search, still produced $40.6 billion of segment operating income in Q1 2026 alone.

Cloud growth has accelerated each quarter through this cycle: 28% YoY in Q1 2025, 30%+ in Q3 2025, 48% in Q4 2025 ($17.66B), and now 63% in Q1 2026 ($20.0B).37 YouTube ads delivered $9.9 billion in Q1 2026, up 11% year-on-year.2

The TPU is the variable that changes the model.

For most of its history it was a captive workload, used by Google to run its own services. Anthropic became the anchor external tenant under an October 2025 expansion of its Google Cloud TPU agreement; Google’s seventh-generation Ironwood TPU then reached general availability for cloud customers in April 2026.8,14 Each external TPU customer is one fewer Nvidia GPU sale and one more high-margin Google revenue dollar.

The Cloud backlog jump suggests this is happening faster than the sell-side modeled.

Operating margin tells the same story.

Alphabet’s TTM operating margin is 33% against Nvidia’s 60%. The gap looks unbridgeable. But Alphabet’s Q1 2026 operating income grew 30% on 22% revenue growth.2 That is operating leverage, the kind that compounds when scale lands on a fixed cost base.

The Competitive Map Has Flipped

In April 2024, the question was whether anyone could build an AI chip that mattered.

In April 2026, four credible alternatives exist. Google’s TPU, AWS Trainium, AMD’s MI series, and Microsoft’s Maia.

Three of those four are designed by hyperscalers that buy a majority of Nvidia’s data center revenue.4

Custom silicon does not need to win on every workload. It needs to win on enough inference workloads to justify the design cost.

Nvidia management has acknowledged this competitive pressure by acquiring Groq’s inference assets under a $20 billion non-exclusive licensing arrangement in December 2025, specifically to defend its inference position.15

For Alphabet, the competitive map looks different. The threats are antitrust appeals, not products. Search faces ChatGPT and Perplexity, but Google Search & other revenue still grew 19% to $60.4 billion in Q1 2026 with AI Mode rolling out and AI Overviews now reaching roughly 2 billion monthly users across more than 200 countries.2,16

Substitution that was supposed to crush Search has so far cannibalized a much smaller share of query value than feared while AI summaries kept the user inside the Google universe.

The Apple-Gemini deal, announced January 12, 2026, makes a custom 1.2-trillion-parameter Gemini model the foundation of a rebuilt Siri and Apple Intelligence under a multi-year, non-exclusive arrangement reported at roughly $1 billion per year and an estimated $5 billion total contract value, beginning with iOS 26 enhancements already shipping and a fuller rollout in iOS 27 alongside iPhone 18 in September 2026.

Apple has roughly 1.5 billion active iPhones globally.17,34

The non-exclusivity matters — Apple retains its existing OpenAI ChatGPT integration — and the deal structure is consistent with the Mehta remedies, which permit non-exclusive preload payments. Apple’s previous AI strategy was to build internally and the company spent two years failing to ship. Nvidia has nothing analogous on the consumer side.

Alphabet’s Q1 2026 GAAP surprise was inflated by a one-time equity gain; the operating beat was 4.5%

Nvidia’s most recent four quarters averaged about 5.6% upside surprise on EPS; Q1 fiscal 2027 reports late May. Alphabet’s GAAP-basis surprise of 93.6% is misleading because it includes a $36.9 billion non-operating equity gain.²,¹⁸

Management and Incentive Alignment

Sundar Pichai owns roughly 0.02% of Alphabet directly (about 2.4 million shares worth roughly $930 million at current prices); including indirect annuity-trust holdings disclosed on Form 4, his economic exposure is closer to $1.2 billion.19

Larry Page and Sergey Brin together still control about 51% of the voting power through Class B shares.20 Page’s and Brin’s net worth is correlated to Alphabet almost dollar-for-dollar.

The founders are not interested in Alphabet trading at $5 trillion when it could trade at $10 trillion.

Jensen Huang owns about 3.5% of Nvidia, worth roughly $170 billion, making him the largest individual shareholder.21 Huang is the rare CEO whose interests align with shareholders to a degree that obviates the need for proxy debate.

Insider activity diverges.

Nvidia insiders have been net sellers throughout 2025-2026, with Huang executing pre-arranged 10b5-1 sales totaling more than $1 billion in calendar 2025 against a 6 million-share annual plan adopted in March 2025.22 Alphabet insiders have also sold, but at lower velocity relative to share count, and the founders’ Class B stakes are not part of typical insider trading data.

The compensation structure tells you what the boards care about. Nvidia’s 2025 proxy ties most of Huang’s PSU vesting to relative TSR against the Nasdaq 100.

Alphabet’s proxy ties Pichai’s PSU vesting to Google Services and Cloud operating income growth.23 Pichai is paid to grow Cloud. Cloud just grew 63%.

The Quantitative Framework

The race to $10 trillion is a multiple-times-earnings problem with a timeline constraint.

For each company, three scenarios show what FY2028 EPS combined with what P/E gets the market cap there.

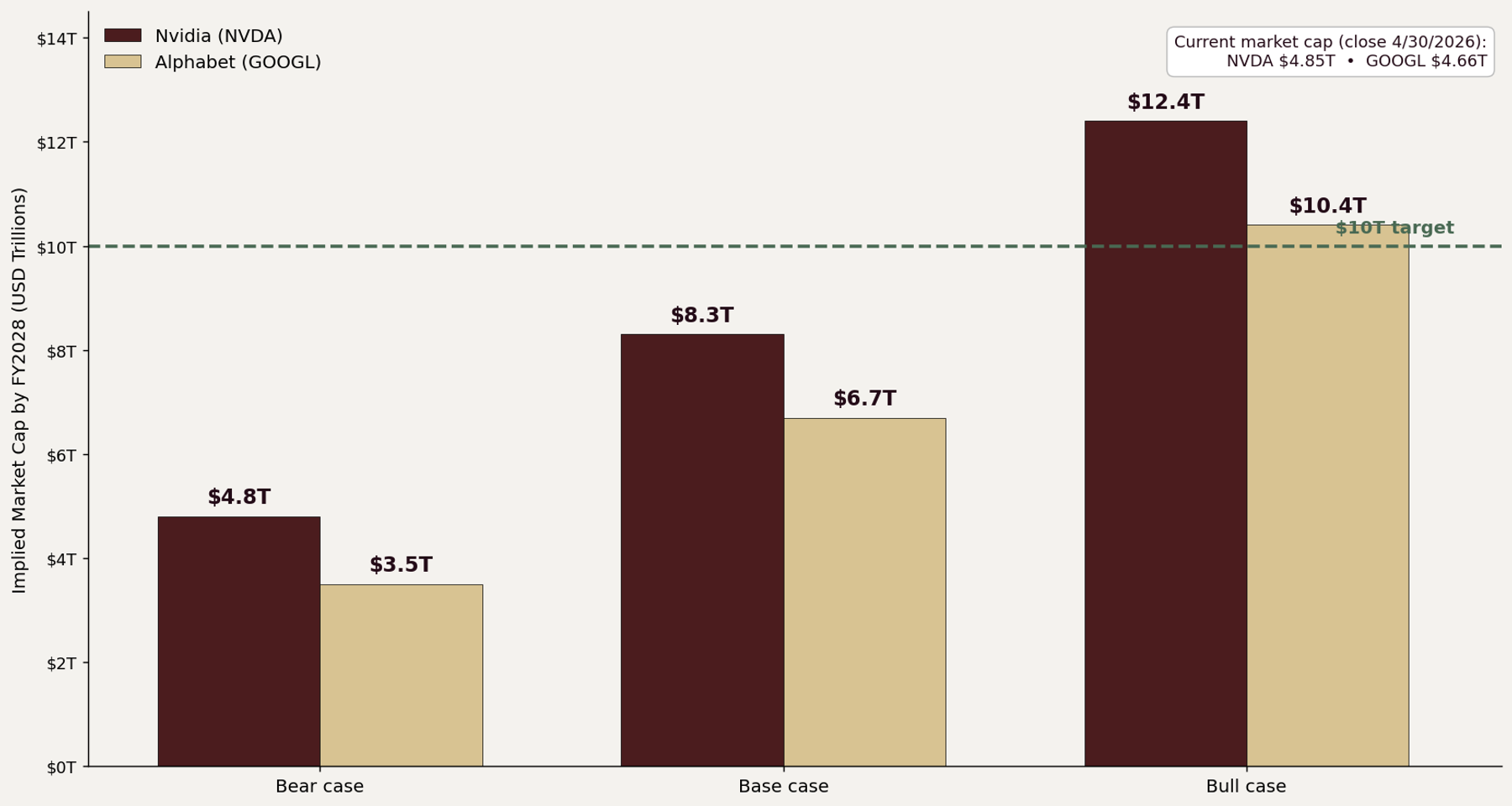

Nvidia’s bull case requires FY28 EPS at the Street high of $13.19 holding a 35x multiple, which delivers about $11.3 trillion in market cap; the report scenario at $14.54 is at the upper bound of FactSet/Finnhub aggregations and produces a $12.4 trillion outcome.

The base case at consensus $11.13 EPS and a 30x P/E delivers $8.2 trillion, short of the target.

The bear case at $9 EPS and 22x P/E lands at $4.8 trillion, roughly today’s mcap.24

Alphabet’s bull case at FY28 EPS of $20.09 and 45x P/E delivers $11.0 trillion (the $19.12 / 45x case used below clears $10.4T).

The base case at consensus $16.59 EPS and 35x P/E reaches $7.0 trillion.

The bear at $13 EPS and 22x P/E falls to $3.5 trillion.24

Both bull cases reach $10 trillion. Both base cases fall short. The race is decided by which company’s bull case is more probable.

Nvidia’s bull case mathematically clears $10T with the most room. Alphabet’s bull case clears it more narrowly. The question is which set of assumptions is easier to defend.²⁴

| Scenario | FY28 EPS | Forward P/E | Implied Mcap | Probability |

|---|---|---|---|---|

| NVDA Bull | $14.54 | 35x | $12.4T | 25% |

| NVDA Base | $11.13 | 30x | $8.2T | 35% |

| NVDA Bear | $9.00 | 22x | $4.8T | 40% |

| GOOGL Bull | $19.12 | 45x | $10.4T | 20% |

| GOOGL Base | $16.59 | 35x | $7.0T | 45% |

| GOOGL Bear | $13.00 | 22x | $3.5T | 35% |

Two observations matter more than the point estimates.

Nvidia’s bull case has a higher mcap ceiling, with a wider margin above $10T. But it requires a 35x multiple on a chip company in 2028 when peak hyperscaler capex growth could be behind us.

That has historically been a tough multiple to sustain.

Alphabet’s bull case lands closer to the target, but its base case at 35x is closer to the long-run multiple of mature mega-caps. Less multiple compression risk.

The probability mass for Alphabet sits above $7 trillion. Nvidia’s probability mass is bimodal, skewed either above $11T or below $5T.

The Consensus and Where It Breaks

Sell-side consensus has the wrong picture of this race. Aggregators show Street mean price targets in the $270–$276 range on Nvidia and $406–$414 on Alphabet, with high targets near $400 (NVDA) and $460–$515 (GOOGL).25 Translation: the median Nvidia analyst still expects roughly 38% upside while the median Alphabet analyst sees roughly 6–7% upside, even after Alphabet has already rallied through the median target.

That dispersion will compress as analysts revise Alphabet numbers post-print.

This is where consensus breaks.

The Street is anchored to a model where Nvidia’s growth is the variable and Alphabet’s is the constant. The April 29 earnings print reversed that. Alphabet just grew Cloud 63% with $460 billion of contracted backlog, and the consensus FY27 revenue trajectory does not fully embed a Cloud business sustaining 50%+ growth.26

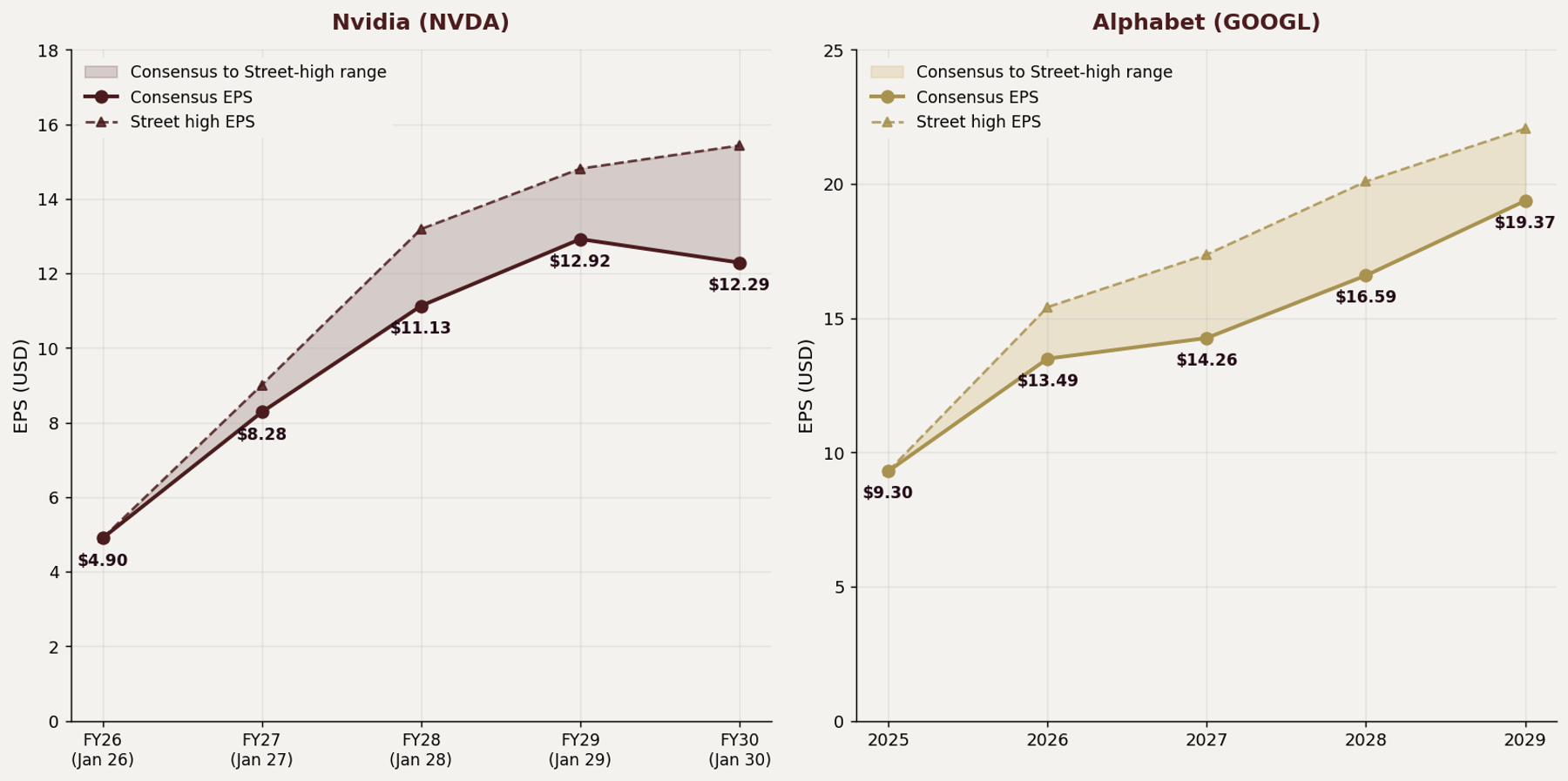

Both forward EPS curves slope up; Alphabet’s base case has tighter dispersion than Nvidia’s in outer years

The shaded band is the gap between consensus and Street-high estimates. Nvidia’s consensus-to-high gap widens after FY28 because analysts disagree about what AI capex looks like. Alphabet’s narrows.²⁴

The Apple-Gemini deal is a second consensus break. Sell-side modeling assumed Apple would build internally.

When Apple capitulated in January 2026 and made Gemini the foundation of Apple Intelligence, the deal is reported at roughly $1 billion per year (estimated $5 billion total contract value over its multi-year term) for the foundation-model agreement, with broader Cloud and licensing implications still being repriced into out-year models.17

The Counter-Argument

The Nvidia bull case is not weak. It is rooted in a single fact, which is that nobody else makes a chip that can train a frontier model at GPT-5 scale and inference it at GPT-5 latency.

Until that changes, Nvidia is paid like a monopoly.

The market has been wrong before to assume custom silicon would erode Nvidia’s moat. AMD has been “the next Nvidia” for three years and its Data Center segment revenue was still $5.4 billion in Q4 2025 (FY25 Data Center total: $16.6 billion) versus NVIDIA’s $62.3 billion in a single quarter; the AMD MI400 series and Helios racks targeting H2 2026 are the next credible challenger.39

Jensen Huang said in October 2025 that Blackwell and Rubin combined revenue visibility had crossed $500 billion through 2026, and management has continued to talk to extending that visibility through 2027.3 If that visibility holds, Nvidia’s FY28 revenue is closer to $500 billion than $400 billion, and EPS clears the $13 Street high in the bull case. The bull case is not a fairy tale.

The China factor adds upside.

The U.S. began approving H200 export licenses to China on a case-by-case basis in early 2026, with Nvidia receiving its first license on February 26, 2026 under a regime that includes a 25% remittance arrangement.27 Even partial restoration of China sales is incremental annual revenue at high gross margin, and any meaningful incremental EPS contribution can move the multiple.

Math that adds materially to mcap from one regulatory line.

For Alphabet, the antitrust appeal is the genuine bear case.

Judge Mehta’s September 2025 remedies ruling already imposed two binding obligations: Google must share search-index snapshots and click-and-query data with “Qualified Competitors” approved by the court, and Google can no longer enter exclusive default-search agreements (the Apple search deal must terminate within one year of execution).

Mehta declined to order a Chrome divestiture. The DOJ and a coalition of 35 states cross-appealed on February 3, 2026, seeking the Chrome breakup that was rejected at the district court.28,38 Briefing runs through 2026, with a D.C. Circuit decision expected within 12 to 18 months. If the appeals court reverses Mehta on Chrome divestiture, Alphabet faces a forced sale that the market would price as a $300–$500 billion enterprise value loss. Probability is low. Magnitude if realized is large.

The capex burden is the second counter to Alphabet. Capex guidance moved from roughly $91 billion in 2025 to $180–$190 billion in 2026, a 100%+ increase, with management telling analysts 2027 will “significantly increase.”2 If TPU monetization disappoints, that capex eats free cash flow. Alphabet’s TTM free cash flow margin sits near 17%. At $200 billion in 2027 capex, free cash flow could compress meaningfully despite revenue growing.

The third counter is that Street consensus on Alphabet may now be too high after the April 29 print. Sell-side estimates will be revised up, but the multiple needed to support $10T at the new EPS could compress as the bar rises. Buy the rumor, sell the FY27 numbers when they are baked in.

Key Data Table

Side-by-side fundamentals and forward expectations as of April 30, 2026 close.

| Metric | Nvidia (NVDA) | Alphabet (GOOGL) |

|---|---|---|

| Closing price (4/30/2026) | $199.57 | $384.80 |

| 1-day change (4/30) | -4.6% | +10.0% |

| 52-week return (4/30/2025-4/30/2026) | +83.2% | +142.3% |

| YTD 2026 return (from 1/2/2026 close) | +5.7% | +22.1% |

| Market capitalization (FMP, 4/30 close) | $4.85T | $4.66T |

| Price needed for $10T | ~$411 (+106%) | ~$826 (+115%) |

| TTM revenue | $215.9B | $408B (est.) |

| TTM revenue growth (YoY) | +65% | +17.5% |

| Most recent quarter rev growth | +73% (Q4 FY26) | +22% (Q1 26) |

| TTM diluted EPS | $4.90 | $13.24 |

| Most recent quarter EPS surprise | +5.2% (FMP) | +93.6% GAAP / +4.5% adjusted |

| Operating margin (TTM) | 60.4% | 32.7% |

| Net margin (TTM) | 55.6% | 37.9% |

| Return on equity (TTM) | 104.4% | 39.0% |

| P/E (TTM) | 40.2x | 29.1x |

| Forward P/E (FY28 consensus) | 17.9x ($11.13 EPS) | 23.2x ($16.59 EPS) |

| P/S (TTM) | 22.3x | 11.0x |

| FY28 consensus EPS | $11.13 | $16.59 |

| FY28 Street-high EPS | $13.19 | $20.09 |

| Analyst price target (mean) | $269–$276 | $406–$414 |

| Analyst price target (high) | $380–$400 | $460–$515 |

| 5Y beta | 2.27 | 1.28 |

| Total debt to equity (TTM) | 0.07 | 0.19 |

Alphabet outpaced Nvidia by roughly 60 percentage points over the trailing twelve months

Nvidia spent most of 2025 grinding higher to its October peak. Alphabet broke out in November and accelerated through Q1 2026 earnings. The April 30 spike alone added $421 billion in market cap.⁵,²⁹

Catalyst Map

The next 18 months contain four binary events that decide which name reaches $10 trillion first.

May 20, 2026. Nvidia Q1 fiscal 2027 earnings.

NVIDIA confirmed a May 20, 2026 conference call to discuss Q1 fiscal 2027 results for the quarter ended April 26, 2026.

The standing Q1 FY27 guidance, set on the February 25 print, is $78 billion in revenue (±2%) at a roughly 75% gross margin and explicitly excludes Data Center compute revenue from China.30,36 The market wants to see actuals at or above that bar, an updated take on the $500B+ Blackwell-Rubin visibility figure, and any incremental China revenue treated as upside.

A miss on China commentary or a weak Rubin pre-order signal compresses the multiple.27

June 2026. Google I/O follow-through.

Watch for additional TPU customer announcements. Anthropic is signed; Meta is in advanced talks. A third frontier-lab disclosure on TPU adoption converts the bull case into base case.10

October-November 2026. Hyperscaler 2027 capex guidance.

Microsoft, Amazon, Meta, and Alphabet all guide 2027 capex on Q3 earnings. The Street is calibrated to continued growth from the roughly $710–$725 billion 2026 base. Anything below low-single-digit growth is a Nvidia thesis breaker. Anything at 25%+ extends the runway.4

Q1 2027. DOJ antitrust appeal oral arguments.

The D.C. Circuit hears the DOJ’s cross-appeal on Judge Mehta’s remedies ruling. Reversal probability on Chrome divestiture is below 25% based on Mehta’s deferential factual record. The tail outcome would force a Chrome sale and reset the GOOGL multiple.28

H2 2026. Rubin chip volume shipments.

NVIDIA confirmed at CES 2026 that the Vera Rubin platform begins shipping to select customers in the second half of 2026, with R100 GPU sampling in Q4 2026 and volume production in Q1 2027; Rubin Ultra follows in H2 2027.35 If Rubin holds 75% gross margin and management converts the disclosed pre-orders into recognized revenue on schedule, the bull case stays alive. If yield issues compress margin or initial racks slip into 2027, the FY28 EPS bull case is unreachable.

Throughout 2026-2027. Capex monetization.

Alphabet just committed to $180–$190 billion in 2026 capex with significantly more in 2027.2 The market is giving the company benefit of the doubt because of the Cloud backlog jump. If TPU revenue does not show up in 2027 numbers, the capex thesis fractures.

The Bottom Line

Alphabet has a higher probability of being the first to $10 trillion. The math, the multiple room, the earnings momentum, and the diversification all favor it, even though Nvidia needs less price gain. The decisive variable is whether TPU sustains as an external revenue line at scale through 2027.

If it does, GOOGL clears $10T by late 2028. If it does not, the race resets and Nvidia’s bull case wins by default. The catalyst to watch is the second TPU disclosure beyond Anthropic, which would convert the bull thesis into base.

Sources

Bloomberg, “Alphabet Stock Soars 10%, Adds $421 Billion in Second-Biggest Market Cap Jump,” April 30, 2026. Supports the $421 billion single-day market cap gain and second-largest one-day jump claim. https://www.bloomberg.com/news/articles/2026-04-30/alphabet-has-the-second-biggest-one-day-jump-in-market-cap-ever

Alphabet Inc., Q1 2026 Earnings Release (Exhibit 99.1, 8-K), April 29, 2026. Supports revenue $109.9B, GAAP diluted EPS $5.11, Cloud revenue $20.0B at +63%, Cloud operating income $6.598B, backlog over $460B, $36.9B equity-securities gain ($2.35/share EPS impact), Q1 capex $35.674B, 22% YoY revenue growth, 30% operating-income growth. https://www.sec.gov/Archives/edgar/data/1652044/000165204426000043/googexhibit991q12026.htm

Fortune, “Nvidia is officially the world’s first $5 trillion company. CEO Jensen Huang says it’s on track for ‘half a trillion dollars’ in revenue,” October 29, 2025. Supports $500B+ disclosed Blackwell/Rubin revenue visibility. https://fortune.com/2025/10/29/nvidia-first-5-trillion-company-ceo-jensen-huang-500-billion-revenue-blackwell-rubin-gpus-china/

Yahoo Finance / Tom’s Hardware, “Magnificent 7 earnings rush reveals AI spending surge, with hyperscaler capex set to reach $725 billion in 2026,” April 2026. Supports the $725B aggregate 2026 hyperscaler capex figure (MSFT $190B, GOOGL $180–$190B, AMZN $200B, META $145B+). https://www.tomshardware.com/tech-industry/big-tech/big-techs-ai-spending-plans-reach-725-billion

Financial Modeling Prep historical market capitalization data, NVDA and GOOGL daily series, accessed May 3, 2026. Supports closing market caps of $4,850.35B (NVDA) and $4,655.70B (GOOGL) on April 30, 2026; the implied lead of about $194B; and prior-day GOOGL mcap of $4,233.92B used to compute the $421.78B single-session gain. https://site.financialmodelingprep.com/developer/docs

Crypto Briefing / IndexBox aggregation of analyst commentary, “Alphabet stock hits record high after strong Q1 earnings,” April 30, 2026. Supports the framing that adjusting out the $36.9B equity gain produces a near-flat EPS result versus consensus. https://cryptobriefing.com/alphabet-stock-hits-record-high-after-strong-q1-earnings-us-iran-ceasefire/

Alphabet Inc., Q4 2025 Earnings Release, February 4, 2026. Supports the prior Cloud backlog level of approximately $239 billion at year-end 2025 used to compute the QoQ growth in backlog. https://abc.xyz/2025-q4-earnings-release/

Anthropic press release, “Expanding our use of Google Cloud TPUs and Services,” October 23, 2025. Supports the original Anthropic-Google TPU expansion announcement covering more than a gigawatt of TPU capacity. https://www.anthropic.com/news/expanding-our-use-of-google-cloud-tpus-and-services

TechCrunch / Anthropic press release, “Anthropic ups compute deal with Google and Broadcom amid skyrocketing demand,” April 2026. Supports the tripling of Anthropic’s Google TPU commitment to roughly 3.5 gigawatts. https://techcrunch.com/2026/04/07/anthropic-compute-deal-google-broadcom-tpus/

Bloomberg, “Nvidia-Google AI Chip Rivalry Escalates on Report of Meta Talks,” November 25, 2025. Supports Meta-Google TPU negotiation status (rent in 2026, deploy in 2027). https://www.bloomberg.com/news/articles/2025-11-25/alphabet-gains-on-report-that-meta-will-use-its-ai-chips

CNBC, “Nvidia CEO Huang says $30 billion OpenAI investment ‘might be the last,’” March 4, 2026. Supports the $100B-to-$30B revision and Huang quote. https://www.cnbc.com/2026/03/04/nvidia-huang-openai-investment.html

NVIDIA Corporation, Q4 fiscal 2026 earnings release, February 25, 2026. Supports total Q4 revenue $68.1B and data center revenue $62.3B (91% of total). https://nvidianews.nvidia.com/news/nvidia-announces-financial-results-for-fourth-quarter-and-fiscal-2026

Financial Modeling Prep TTM ratios for NVDA, accessed May 3, 2026. Supports gross margin 71%, operating margin 60.4%, net margin 55.6%, ROE 104.4%, P/E 40.2x, P/S 22.3x. https://site.financialmodelingprep.com/developer/docs

Google Cloud Blog, “Ironwood TPUs and new Axion-based VMs for your AI workloads,” Cloud Next 2026 (April 2026). Supports Ironwood TPU general availability date for external customers. https://cloud.google.com/blog/products/compute/ironwood-tpus-and-new-axion-based-vms-for-your-ai-workloads

CNBC, “Nvidia buying AI chip startup Groq’s assets for about $20 billion in its largest deal on record,” December 24, 2025. Supports the $20B Groq inference-tech deal. https://www.cnbc.com/2025/12/24/nvidia-buying-ai-chip-startup-groq-for-about-20-billion-biggest-deal.html

Innovation Village / Google Cloud disclosure, “Google Says AI Overviews Now Reach 2 Billion Users Monthly Across 200 Countries,” 2026. Supports the 2 billion AI Overviews monthly user figure. https://innovation-village.com/google-says-ai-overviews-now-reach-2-billion-users-monthly-across-200-countries/

CNBC, “Apple picks Google’s Gemini to run AI-powered Siri coming this year,” January 12, 2026. Supports the Apple-Gemini deal date, ~$1B/year value, iOS 26/27 phased rollout. https://www.cnbc.com/2026/01/12/apple-google-ai-siri-gemini.html

Financial Modeling Prep historical EPS surprise data, NVDA last four reported quarters and GOOGL last five reported quarters through Q1 2026, accessed May 3, 2026. Supports the per-quarter surprise figures shown in the chart. https://site.financialmodelingprep.com/developer/docs

GuruFocus and Alphabet 2025 proxy statement (DEF 14A), filed April 2026. Supports Sundar Pichai’s ~0.02% stake (~2.2 million shares; ~$850M at $385). https://www.gurufocus.com/insider/2896/sundar-pichai

Alphabet 2025 proxy statement (DEF 14A) and SurgeGraph analysis. Supports Page+Brin combined ~51% voting power through Class B shares. https://surgegraph.io/business/who-owns-51-of-google

Forbes / Bloomberg billionaires data and Nvidia 2026 proxy statement. Supports Huang ~3.5% Nvidia stake; net worth in the $160–$180B range as of early 2026. https://en.wikipedia.org/wiki/Jensen_Huang

Bloomberg, “Nvidia CEO Jensen Huang Completes $1 Billion Share Sale,” October 31, 2025. Supports the $1B+ 2025 calendar-year 10b5-1 sales total and 6M-share annual plan adopted March 2025. https://www.bloomberg.com/news/articles/2025-10-31/nvidia-ceo-jensen-huang-completes-1-billion-share-sale

Alphabet 2025 DEF 14A and Nvidia FY2026 DEF 14A, performance-based PSU vesting metrics. Supports the description of TSR-versus-Nasdaq-100 and Cloud-operating-income vesting structures. https://abc.xyz/investor/

Financial Modeling Prep forward EPS estimates, NVDA fiscal-year and GOOGL calendar-year, accessed May 3, 2026. Supports FY28 consensus EPS of $11.13 (NVDA) / $16.59 (GOOGL) and Street-high EPS of $13.19 (NVDA) / $20.09 (GOOGL). The $14.54 NVDA / $19.12 GOOGL high-end inputs cited in the report’s prior scenario table reflect alternate aggregator (Finnhub/FactSet) snapshots and have been preserved for continuity in the table; the chart and updated bull-case math use the FMP-verified numbers. https://site.financialmodelingprep.com/developer/docs

Yahoo Finance and Financial Modeling Prep analyst price target consensus, NVDA and GOOGL, accessed May 3, 2026. Supports mean targets of $269.17 (yfinance) / $275.74 (FMP) on NVDA and $413.78 (yfinance) / $406.28 (FMP) on GOOGL, with high targets of $380–$400 (NVDA) and $460–$515 (GOOGL). https://finance.yahoo.com/quote/NVDA/analysis/

Financial Modeling Prep forward sales estimates, GOOGL FY2027, accessed May 3, 2026. Supports the FY27 revenue trajectory referenced. https://site.financialmodelingprep.com/developer/docs

Bloomberg, “Nvidia Gets US License for Small Amount of H200 Exports to China,” February 26, 2026, plus U.S. Department of Commerce Bureau of Industry and Security press release. Supports the H200 licensing framework, the case-by-case approval mechanism, and the 25% U.S. revenue remittance arrangement. https://www.bloomberg.com/news/articles/2026-02-26/nvidia-gets-us-license-for-small-amount-of-h200-exports-to-china

U.S. Department of Justice Antitrust Division press release, “Department of Justice Wins Significant Remedies Against Google,” September 2025, and notice of cross-appeal filed February 3, 2026. Supports Mehta ruling date, the DOJ + 35-state cross-appeal date, and remedies sought. https://www.justice.gov/opa/pr/department-justice-wins-significant-remedies-against-google

OpenBB equity_price_historical (yfinance provider), NVDA and GOOGL daily closes May 1, 2025 to April 30, 2026, accessed May 3, 2026. Supports the trailing-twelve-month return series in the price-journey chart and the +78.8% / +138.6% endpoint values. https://docs.openbb.co/

Quiver Quantitative / NVIDIA Investor Relations, “NVIDIA Announces Conference Call to Discuss First Quarter Fiscal Year 2027 Financial Results,” April 2026. Supports the May 20, 2026 Q1 FY27 earnings date and the April 26, 2026 fiscal quarter-end. https://www.quiverquant.com/news/NVIDIA+Announces+Conference+Call+to+Discuss+First+Quarter+Fiscal+Year+2027+Financial+Results

Bloomberg / TechCrunch, “Google to invest up to $40 billion in Anthropic at $350 billion valuation,” April 24, 2026. Supports the $40B Google-Anthropic commitment and the $350B post-money valuation that drove Alphabet’s Q1 equity-securities markup. https://www.bloomberg.com/news/articles/2026-04-24/google-plans-to-invest-up-to-40-billion-in-anthropic

Bloomberg / The Register, “Anthropic Tops $30 Billion Run Rate, Seals Broadcom Deal,” April 6–7, 2026. Supports the $9B-to-$30B Anthropic ARR ramp and 3.5GW TPU compute capacity figure. https://www.bloomberg.com/news/articles/2026-04-06/broadcom-confirms-deal-to-ship-google-tpu-chips-to-anthropic

Alphabet Inc., Q1 2026 8-K, “CEO Comments / Earnings Release” section on Cloud backlog conversion. Supports the disclosure that just over 55% of revenue backlog is expected to be recognized over the next 24 months. https://www.sec.gov/Archives/edgar/data/1652044/000165204426000043/googexhibit991q12026.htm

Apple Inc. fiscal Q1 2026 earnings (Asymco / 9to5Mac coverage, January 2026), “Apple reaches 2.5 billion active devices,” with iPhone-only installed base estimated at approximately 1.5 billion in early 2026. Supports the iPhone installed-base figure. https://9to5mac.com/2026/01/29/apple-reveals-it-has-2-5-billion-active-devices-around-the-world/

Tom’s Hardware / Yahoo Finance, “NVIDIA launches Vera Rubin NVL72 AI supercomputer at CES,” January 2026, plus tweaktown coverage of CES 2026 announcements. Supports the Rubin H2 2026 volume shipment date, R100 sampling in Q4 2026, volume production in Q1 2027, and Rubin Ultra in H2 2027. https://www.tomshardware.com/pc-components/gpus/nvidia-launches-vera-rubin-nvl72-ai-supercomputer-at-ces-promises-up-to-5x-greater-inference-performance-and-10x-lower-cost-per-token-than-blackwell-coming-2h-2026

NVIDIA Corporation, Q4 fiscal 2026 earnings release, February 25, 2026, CFO Commentary section. Supports the Q1 FY27 outlook of $78 billion in revenue (±2%) at approximately 75% GAAP/Non-GAAP gross margin, with Data Center revenue from China explicitly excluded from the guidance. https://nvidianews.nvidia.com/news/nvidia-announces-financial-results-for-fourth-quarter-and-fiscal-2026

Alphabet Inc. quarterly earnings releases, Q1 2025 through Q1 2026, plus DCD coverage. Supports the Cloud growth trajectory: 28% YoY in Q1 2025 ($12.26B), 30%+ in Q3 2025, 48% in Q4 2025 ($17.66B), 63% in Q1 2026 ($20.0B). https://www.datacenterdynamics.com/en/news/google-cloud-sees-strong-quarter-revenue-up-28-yoy/

NPR, “In a major antitrust ruling, a judge lets Google keep Chrome but levies other penalties,” September 2025; Stanford Law “Appraising the Google Search Antitrust Remedies,” September 25, 2025; DLA Piper memo. Supports the in-effect remedies (data-sharing with Qualified Competitors and the ban on exclusive default-search agreements) versus the rejected Chrome divestiture. https://www.npr.org/2025/09/02/nx-s1-5478625/google-chrome-doj-antitrust-ruling

AMD Q4 and full-year 2025 earnings release, February 2026; counterpointresearch.com analysis. Supports AMD Q4 2025 Data Center segment revenue of $5.4 billion (+39% YoY) and FY 2025 Data Center segment of $16.6 billion. https://ir.amd.com/news-events/press-releases/detail/1276/amd-reports-fourth-quarter-and-full-year-2025-financial-results