ProCap Insights · April 7, 2026

3 Stocks That Win From Both Tariff Refunds and the Iran Oil Shock

Wall Street has separated the Iran oil shock from the $166 billion tariff refund into two trades. The market is pricing energy names for oil and retail names for tariff windfalls, but three companies sit squarely at the intersection of both catalysts, and nobody is talking about the overlap.

What to Know

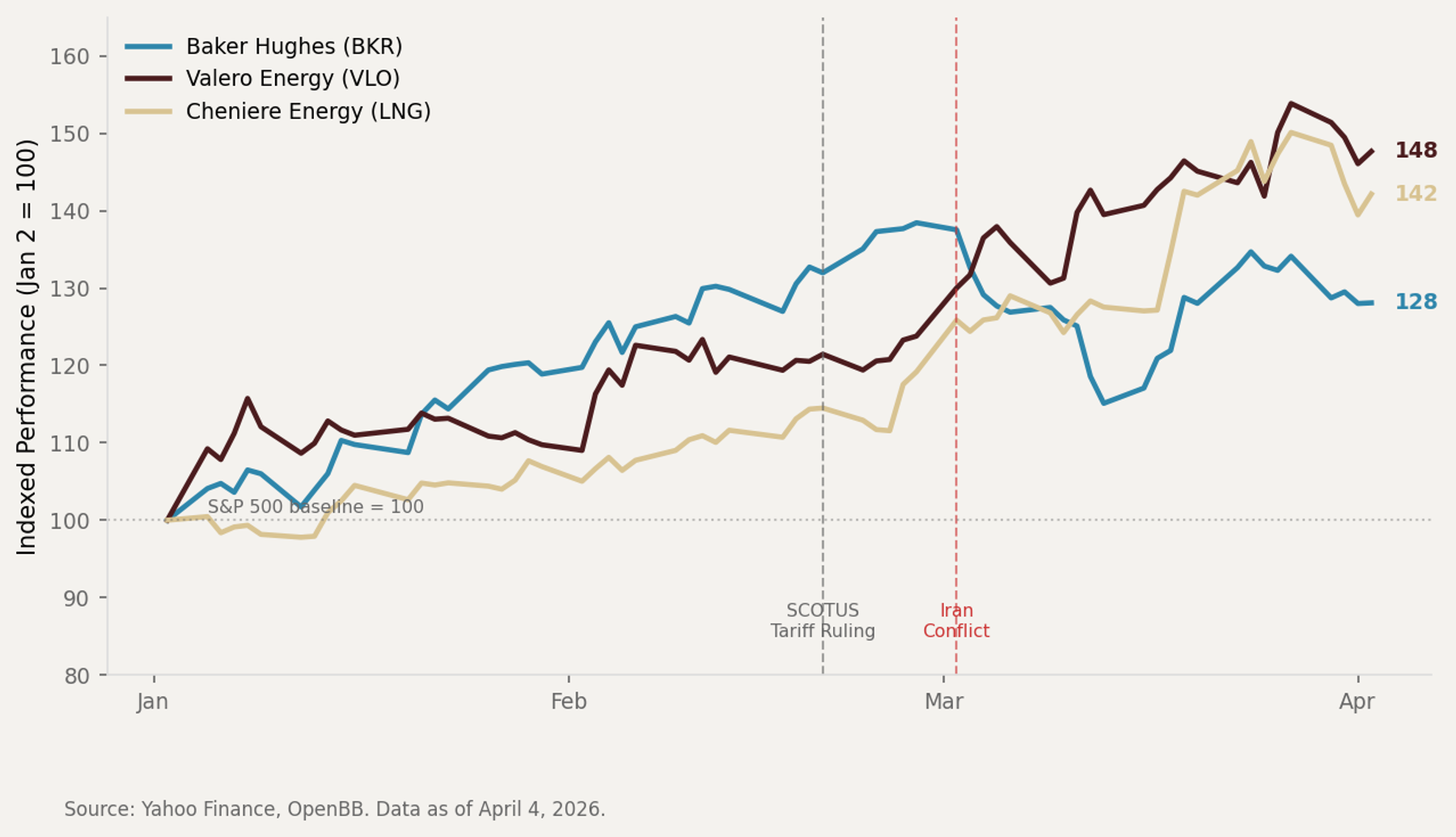

- Baker Hughes (BKR, $60.38), Valero Energy (VLO, $244.09), and Cheniere Energy (LNG, $281.16) each benefit from both the Hormuz-driven oil shock and the Supreme Court-ordered IEEPA tariff refunds. An equally weighted basket of the three has returned 39% YTD, outpacing the S&P 500 energy sector by 9 percentage points.

- Baker Hughes disclosed a $100 to $200 million tariff drag on EBITDA in 2025. That drag now becomes a potential cash refund, adding roughly 8% to forward EPS at a time when the Iran conflict is simultaneously driving record oilfield services demand.

- The CBP tariff refund portal launches around April 20, 2026, creating a near-term catalyst window for all three names as refund filings begin and analysts start modeling the windfall into Q2 estimates.

All Three Dual-Catalyst Stocks Accelerated After the Iran Conflict Began in Early March

Yahoo Finance, OpenBB. Indexed to 100 on January 2, 2026.

The Analytical Framework

The selection criteria required a company to pass two independent filters simultaneously. Filter one demanded direct, material revenue or margin benefit from Brent crude above $100 per barrel, whether through production economics, refining margins, or export pricing. Filter two required documented exposure to IEEPA tariff costs on imported goods, meaning a verifiable record of paying tariffs on steel, equipment, construction materials, or commodity imports that are now eligible for refund under the Court of International Trade ruling from March 4, 2026.

Most energy companies pass filter one. Few pass filter two, because domestic E&P producers like EOG Resources or Pioneer import relatively little.

Most tariff refund beneficiaries, such as Walmart, Target, and Apple, fail filter one entirely. The intersection is narrow, and that narrowness is what makes it valuable.

The three names that emerged, Baker Hughes, Valero, and Cheniere, each represent a different angle on the dual catalyst. BKR captures the intersection through oilfield equipment imports.

VLO captures it through refining input costs and crude import tariffs. LNG captures it through massive construction-phase equipment imports for its Corpus Christi Stage 3 expansion.1

| Company | Ticker | Price | Mkt Cap | YTD Return | Fwd P/E | Oil Catalyst | Tariff Catalyst |

|---|---|---|---|---|---|---|---|

| Baker Hughes | BKR | $60.38 | $59.7B | +28.1% | 22.9x | Record services demand | $100-200M EBITDA refund |

| Valero Energy | VLO | $244.09 | $73.0B | +47.7% | 14.6x | Crack spread at $54/bbl | Capex steel/crude tariff refund |

| Cheniere Energy | LNG | $281.16 | $60.5B | +42.1% | 19.3x | Qatar LNG supply lost, pricing surge | $6B+ Stage 3 equipment refund |

Data as of April 4, 2026. Forward P/E computed from FMP consensus estimates. Prices via Yahoo Finance/OpenBB.2

The $166 Billion Tailwind Nobody Is Pricing Into Energy

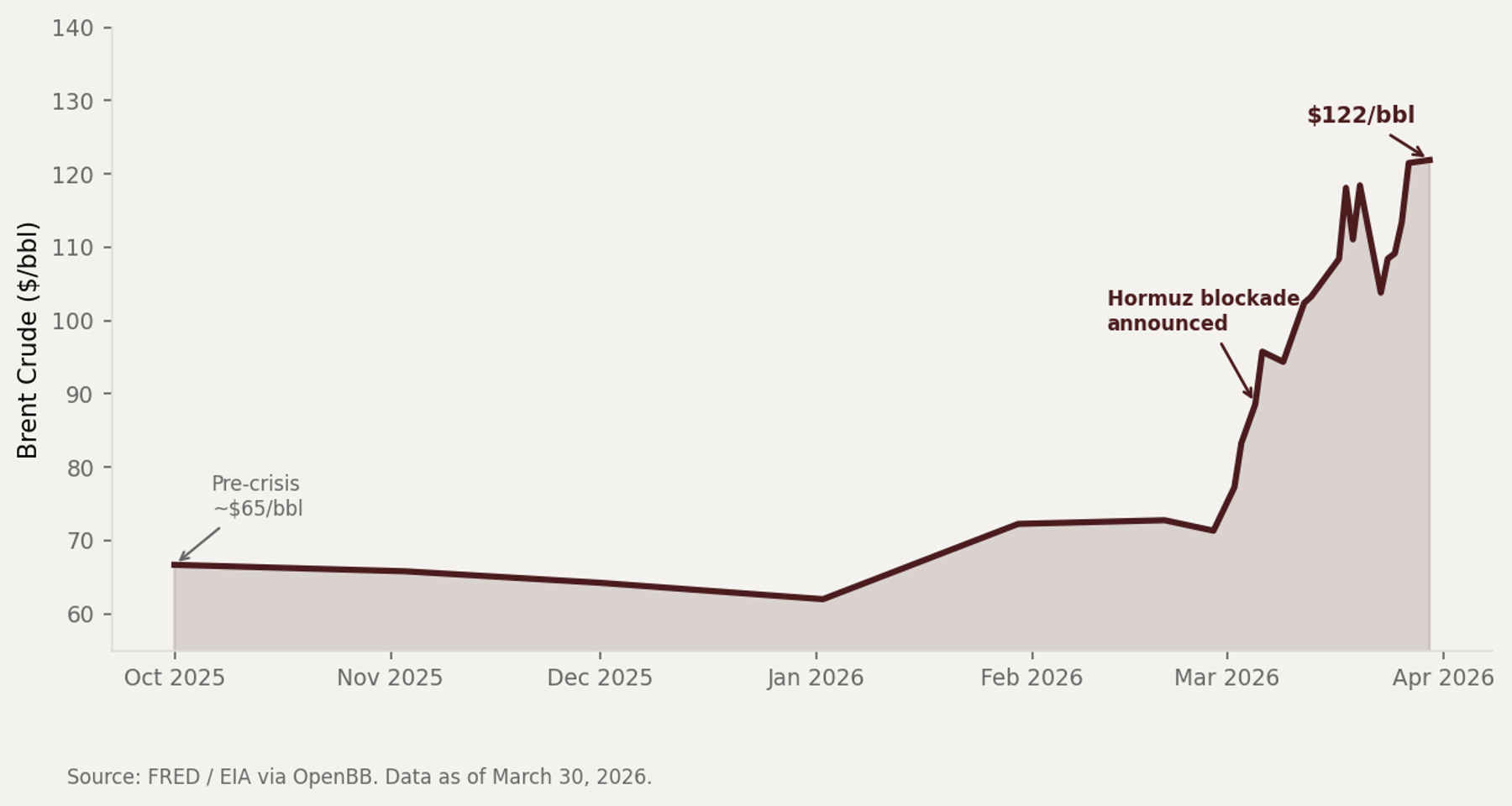

Brent Crude Nearly Doubled in Five Weeks After the Hormuz Blockade

FRED / EIA via OpenBB. Data as of March 30, 2026.

On February 20, 2026, the Supreme Court struck down all IEEPA tariffs in a 6-3 ruling, declaring that the emergency powers law does not give the president authority to tax imports.3 The immediate question was what happens to the $166 billion the government already collected. On March 4, the Court of International Trade issued an order stating that importers of record whose entries were subject to IEEPA tariffs are entitled to refunds, though the ruling remains subject to appeals and administrative implementation.4

Eight days later, Iran closed the Strait of Hormuz. Brent crude, which had been trading near $72 at the time of the SCOTUS ruling, breached $100 on March 12 and hit $122 by month-end.

The two catalysts have been covered in entirely separate news cycles. The tariff refund story belongs to retail analysts, and the oil shock story belongs to energy analysts.

Almost no one has mapped where the two overlap.

CBP is developing a consolidated automated process, including the Consolidated Administration and Processing of Entries (CAPE) system, to handle refunds. Trade practitioners indicate CBP is targeting an initial portal launch in late April, but timelines and functionality remain subject to change.5

That timeline matters because it creates a potential catalyst window. Once the portal opens, companies can begin filing claims, and refund amounts can start appearing in earnings guidance.

Name-by-Name Analysis

Baker Hughes (BKR). The Equipment Importer With a $200 Million Windfall

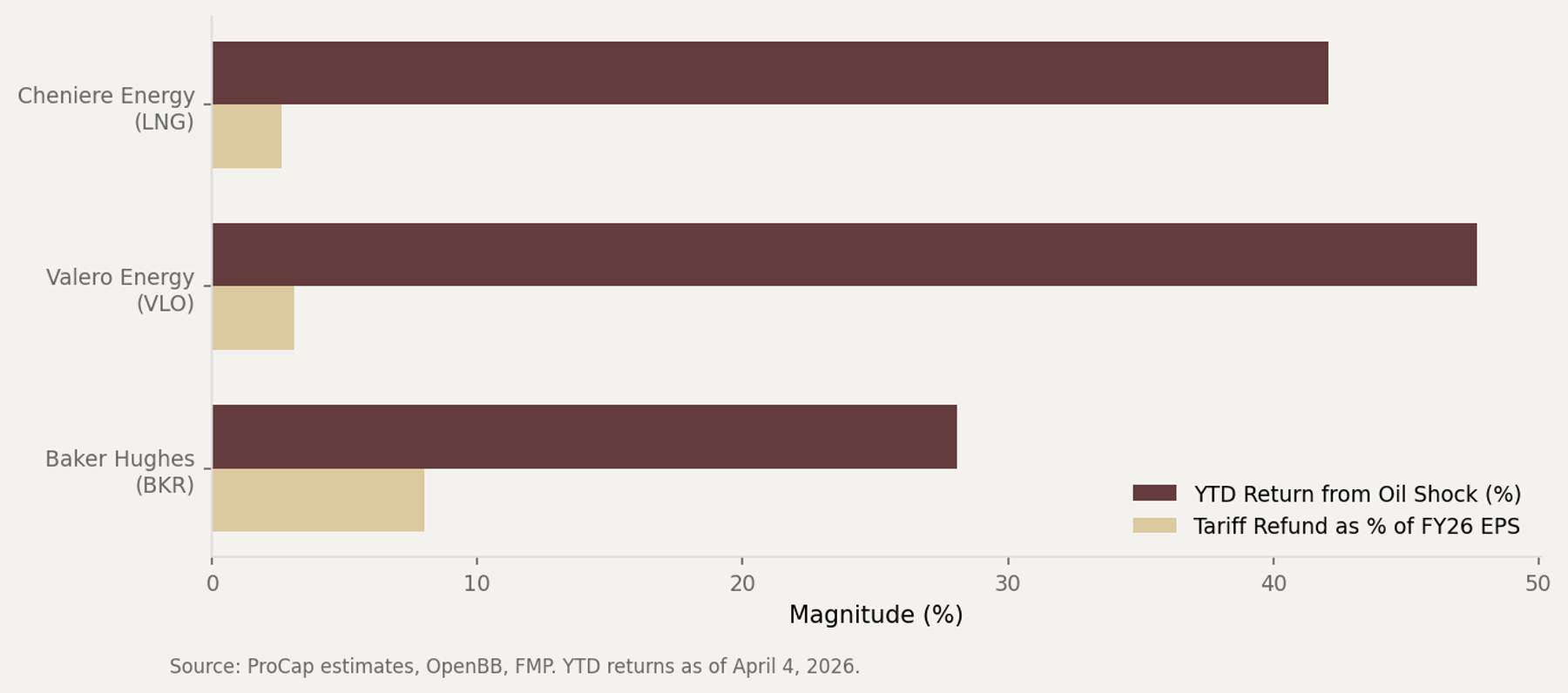

Baker Hughes management disclosed a $100 to $200 million net tariff impact on EBITDA during the IEEPA period, driven by imported steel, specialized drilling components, and subsea equipment.6 That cost is now eligible for a full refund. At the low end of the range, $100 million represents roughly 2.3% of TTM EBITDA. At the high end, $200 million represents 4.7%.

The Iran conflict is the second engine. With Brent above $100, global E&P capital expenditure is accelerating.

BKR posted record Q4 2025 EBITDA, and consensus forward EPS for FY2026 stands at $2.64, up 7% from FY2025 actual. Evercore ISI raised its price target to $68 in February, and Jefferies set $67.7

The critical point is that most analyst models already assume the tariff drag persists. If the CAPE portal delivers refunds in Q2 or Q3, the uplift flows directly to EBITDA and free cash flow. At the current EV/EBITDA of 14.7x, a $200 million EBITDA recovery implies roughly $2.9 billion in enterprise value not currently reflected in the stock price.

Valero Energy (VLO). The Refiner Riding a Double Margin Expansion

The 3-2-1 crack spread jumped from under $20 per barrel at the start of 2026 to over $54 in late March, with the diesel crack hitting $65 per barrel, approaching the all-time record of $83 set in October 2022.8 Valero operates 15 refineries with 3.2 million barrels per day of throughput capacity. Every dollar of crack spread expansion drops almost directly to the bottom line.

Valero's tariff exposure is less headline-grabbing than BKR's but no less real. The company's $1.7 billion 2026 capital program relies heavily on imported steel, and its Gulf Coast refineries import crude from tariff-affected countries.

The IEEPA tariffs added cost to both capex and variable input costs. The tariff refund lowers Valero's effective cost structure at exactly the moment when crack spreads are expanding revenue.

The stock trades at 14.6x forward earnings, a discount to the S&P 500 average despite an earnings environment that rivals the 2022 refining supercycle. UBS raised its target to $215 in January, well below the current price, suggesting the Street has not yet caught up to the dual-catalyst thesis.9

Cheniere Energy (LNG). The LNG Monopoly With a Construction Cost Refund

Iran's missiles struck Qatari gas facilities in March, and some analysts estimate that nearly 20% of Qatar's LNG export capacity could be sidelined for years of reconstruction.10 Cheniere is America's largest LNG exporter, operating Sabine Pass and Corpus Christi with over 45 million tonnes per annum of capacity. When Persian Gulf supply disappears, European and Asian buyers have one reliable alternative. Cheniere is that alternative.

Asian benchmark LNG prices jumped 40% at the onset of the crisis. Cheniere's FY2025 results already showed the business accelerating, with revenue of $19.98 billion (up 27% year-over-year) and net income of $5.33 billion (up 64%).11 The Hormuz disruption pushes 2026 into an even more favorable pricing environment.

The tariff catalyst operates through construction economics. Cheniere has funded roughly $6 billion into its CCL Stage 3 expansion, with Trains 5-7 completing through 2026.

That construction required massive imports of specialized LNG equipment, steel, and industrial materials, all subject to IEEPA tariffs. Management acknowledged working through "escalation" pressures with contractor Bechtel.12 The refund of tariffs on that construction spending could represent a material reduction in the project's all-in cost basis.

Baker Hughes Carries the Largest Tariff Refund Relative to Forward Earnings

ProCap estimates based on company disclosures, FMP consensus data. As of April 4, 2026.

The Consensus and Where It Breaks

The prevailing Wall Street view treats the Iran oil shock as a temporary supply disruption. Most energy analysts are modeling Brent returning to $80-90 by year-end, assuming the Strait of Hormuz reopens within 60-90 days. The tariff refund, meanwhile, is treated as a one-time accounting event for retailers, not a structural catalyst for energy companies.

Both assumptions deserve scrutiny. The Dallas Fed published an analysis noting that the Hormuz closure represents "the largest supply disruption in the history of the global oil market," and that reopening requires military clearing operations that have no guaranteed timeline.13 As of April 5, the strait remains largely closed more than a month after the blockade began. Oil futures curves are in steep backwardation, signaling that the market itself does not believe this resolves quickly.

The consensus also misses the compounding effect. A company that benefits from only one catalyst, say XOM from higher oil, gets a linear payoff. A company that benefits from both catalysts simultaneously gets a convex payoff.

Higher oil prices improve revenue while tariff refunds improve the cost structure. The margin expansion is multiplicative, not additive.

The CME FedWatch tool shows a 94.8% probability the Fed holds rates at the April meeting, with a 12% chance of a hike priced in as recently as March 20.14 The oil shock, if current price levels persist, is likely to push headline CPI toward roughly 3.5% by early summer based on energy pass-through models. In that environment, energy companies with dual margin tailwinds are better positioned than the broader market, which faces the prospect of tighter monetary policy.

The Counter-Argument

The strongest case against this thesis rests on three specific risks, and each one has teeth.

The first risk is refund timing uncertainty. While the Court of International Trade has ruled that importers of record are entitled to refunds, the actual disbursement mechanism is still under construction. CBP's CAPE system and related automated processes are in development, and early phases are expected to handle only a portion of eligible claims, with the remainder processed over time.

Companies with complex import histories, particularly those with entries spanning multiple tariff categories, may face delays extending into late 2026 or beyond. Baker Hughes's $100-200 million refund estimate assumes clean processing. If the system bogs down in bureaucratic or legal challenges, the EPS uplift gets pushed to the right.

The second risk is that the Iran premium in oil prices reverses faster than expected. The Pentagon announced a military campaign to reopen Hormuz on March 19, and success could bring a rapid unwinding of the $50+ per barrel risk premium.

If Brent falls back to $75, crack spreads compress to their pre-crisis range, BKR's activity outlook softens, and Cheniere's LNG pricing premium shrinks. A ceasefire or diplomatic breakthrough could evaporate the oil catalyst overnight.

The third risk is the replacement tariff regime. The administration responded to the SCOTUS ruling by moving to impose new tariffs under alternative statutory authorities, including Section 122, with rates in the low- to mid-teens and an initial 150-day horizon discussed in policy guidance.

These tariffs expire around July 24, 2026, but Congress could pass new tariff legislation before then. If a statutory tariff regime replaces IEEPA at comparable rates, the refund becomes a one-time cash injection rather than a structural margin improvement.

Finally, valuation is no longer cheap for any of the three names. VLO has rallied 48% YTD, BKR 28%, and LNG 42%.

Investors buying today are paying for a substantial portion of the dual catalyst already. If either catalyst fades, the downside from current levels is real.

The Bottom Line

Baker Hughes, Valero, and Cheniere each sit at an intersection the market has not explicitly priced, benefiting from both the Hormuz oil shock and the $166 billion IEEPA tariff refund. BKR carries the highest tariff refund relative to earnings and offers the most upside if refunds process cleanly by Q2, while VLO and LNG provide larger absolute exposure to sustained energy price elevation. A late-April CAPE portal launch is the next catalyst to watch, because that is when the refund thesis can begin to move from theoretical to quantifiable, assuming CBP's timing holds.

Sources

1. ProCap Insights dual-catalyst selection methodology. April 2026.

2. FMP consensus EPS estimates, Yahoo Finance / OpenBB price data. As of April 4, 2026.

3. Supreme Court, Learning Resources, Inc. v. Trump, 6-3 ruling. February 20, 2026. Via NPR, NBC News.

4. U.S. Court of International Trade, March 4, 2026. Judge Eaton ruling on importer refund eligibility.

5. U.S. Customs and Border Protection, CAPE system progress report. March 11, 2026. Via Orrick Insights.

6. Baker Hughes Q4 2025 earnings disclosure. Net tariff impact to EBITDA estimated at $100-200M. January 2026.

7. Evercore ISI, BKR price target $68. February 11, 2026. Jefferies, BKR price target $67. January 31, 2026.

8. Benzinga, "The Diesel Crisis Crushing America Is A Goldmine For These 3 Refiners." March 2026. Crack spread data.

9. UBS, VLO price target $215. January 30, 2026. Via The Fly.

10. 24/7 Wall St., "Wall Street Is Buying These 3 LNG Stocks After Iran Missiles Hit Qatar." March 20, 2026.

11. Cheniere Energy Q4 and Full Year 2025 earnings release. February 2026.

12. Cheniere Energy Q4 2025 earnings call transcript. Management commentary on tariff escalation with Bechtel.

13. Dallas Federal Reserve, "What the closure of the Strait of Hormuz means for the global economy." March 20, 2026.

14. CME FedWatch Tool. April 2026 FOMC meeting probabilities. Via MEXC News, CNBC.