ProCap Insights · April 15, 2026

The next Fed Chair has $100 million riding on Stan Druckenmiller's portfolio

Buried on page 36 of Kevin Warsh's nominee ethics disclosure are two lines labeled "Juggernaut Fund, LP," each valued over $50 million and held through his Vicarage Corporation. Both endnotes send readers to the same SEC 13-F filer, CIK 1536411, Stanley Druckenmiller's Duquesne Family Office.

What to Know

- The tactical read is that Druckenmiller's Q4 13-F is the closest public proxy for a Warsh-adjacent book, tilted toward biotech duration (NTRA 12.8 percent, INSM 5.7 percent), leveraged Brazil exposure ($247 million EWZ including $134 million of calls), and growth-equity concentration (CPNG, MELI, TSMC). Vol around the April 16 Senate hearing is the narrow event trade, and the Q1 13-F on May 15 will test whether Druckenmiller held or rotated.3

- The would-be Fed Chair reports zero direct Bitcoin, zero direct Ether, and no coin holdings of any kind. His crypto and AI exposure is venture-stage equity in SpaceX (which absorbed xAI), Polymarket, Recraft, 11x, Tenderly, Blast, Lemon Cash, and Delphi AI, held inside Bessemer, DCM, and THSDFS private funds.

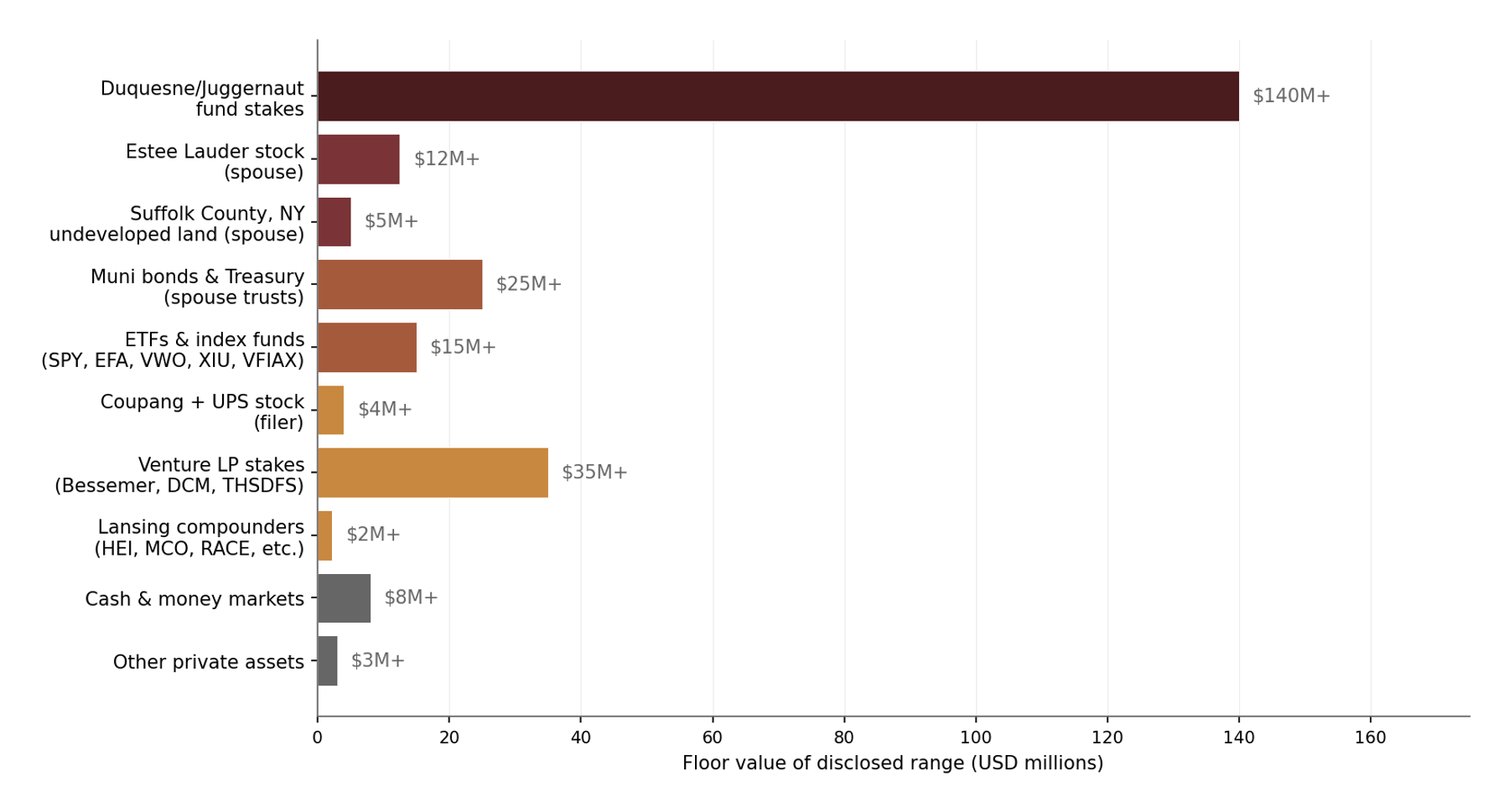

- Ethics certifying officer Heather Jones flagged Warsh as not yet in compliance, with Part 2 lines 23, 25-53, 55-85, 86.3, and 87 requiring divestment before he takes the Fed Chair oath. The floor on that divestment is approximately $122 million, summing the low-end of value ranges across the flagged positions directly from the OGE PDF.1

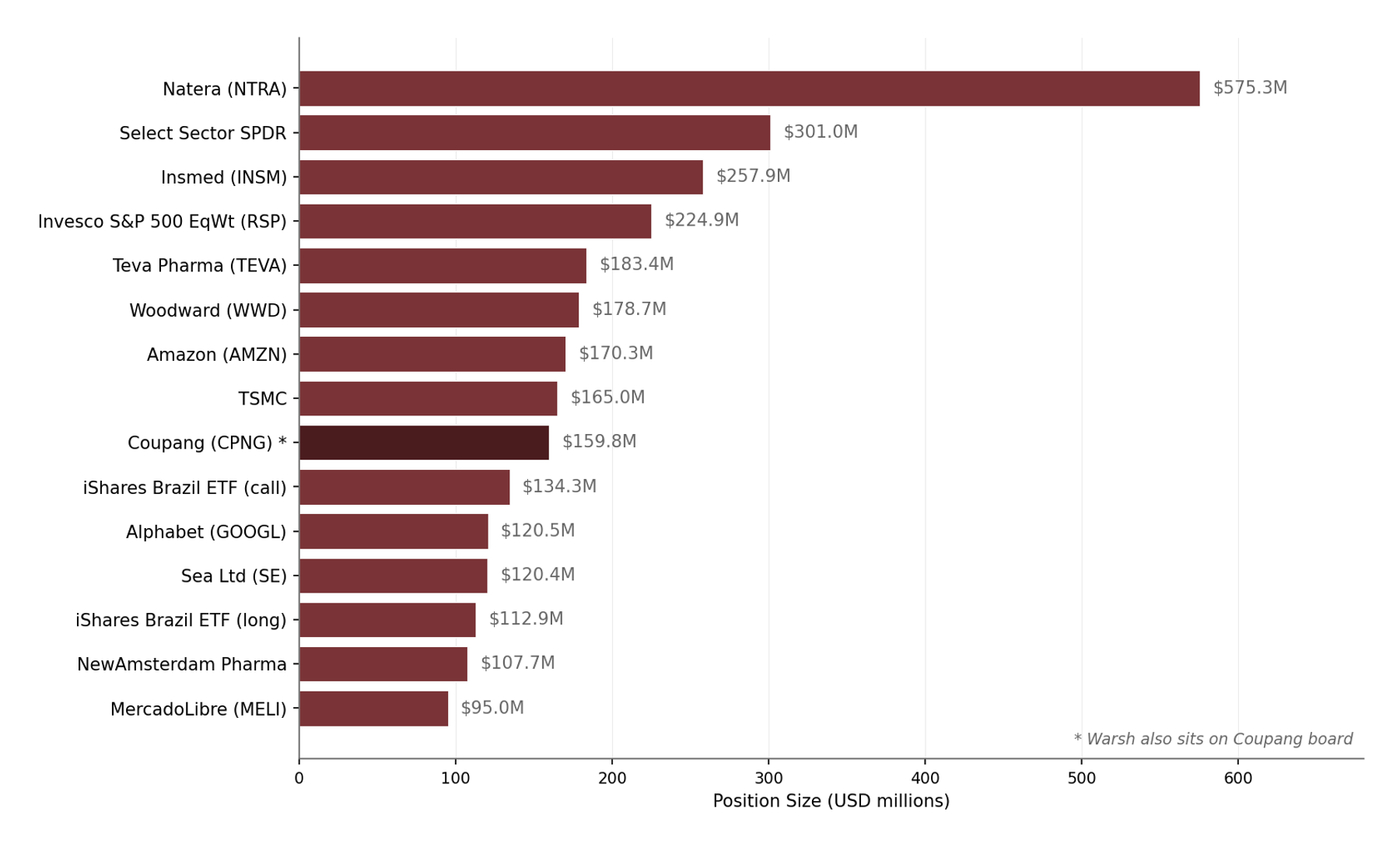

Where Warsh's money actually sits. Duquesne Family Office 13-F, Q4 2025, top 15 positions by reported value.

Values reported by Duquesne Family Office LLC on Form 13F-HR for period ending 2025-12-31, filed 2026-02-17. Total reportable AUM $4.494 billion.³

The filing, decoded

Start with what the media missed entirely. The headline number in every wire story this morning is that Warsh's personal wealth tops $100 million. That is accurate but also boring.

Every Morgan Stanley alum who married into a cosmetics dynasty is worth nine figures.

The real number is on page 36 of the 278e. Line 86.3, "Juggernaut Fund, LP," value Over $50,000,000, income Over $5,000,000. Line 87, a separate Juggernaut Fund entry under the same Vicarage Corp wrapper, value Over $50,000,000, income $1,000,001 to $5,000,000.

Endnote 86.3 reads, "The most recent 13F filing for this fund is available here" followed by a direct SEC link to CIK 1536411, "with the exception of Neptune Insurance Holdings, Inc., which is held by an affiliated fund." Endnote 87 repeats the exact same pointer. Warsh reported 2025 Juggernaut income of $14,232,000 on line 86.3 and $2,765,000 on line 87, a combined $16.997 million on top of the $10.2 million Duquesne consulting fee.1

That CIK is Duquesne Family Office LLC, 40 West 57th Street, Stanley Druckenmiller's shop.2 Warsh is not just an advisor. He is a limited partner, with a reported position unusually large for a federal ethics disclosure.

The consulting relationship matters too. Part 1 of the 278e reports $13.15 million in 2025 consulting fees across four firms, with Duquesne Family Office at $10.2 million, GoldenTree Asset Management at $1.55 million, Cerberus Capital Management at $750,000, and Heitman at $650,000. Duquesne alone is more than three times the other three combined.1,9

Speaking fees added another $1.534 million in 2025 honoraria on top of the consulting line, spread across nine disclosed engagements. Brevan Howard paid Warsh $750,000 across three dates (February, April, and July 2025), the largest item on the form, while State Street and the Pension Real Estate Association each paid $135,000. Eli Lilly paid $122,500, TPG, Warburg Pincus, and Centerview paid $90,000 apiece, BTG Pactual paid $67,500, and Strategas Research Partners paid $54,000.1

Then look at what Druckenmiller actually owns. The Q4 2025 13-F discloses $4.494 billion across 62 positions. The concentration is extreme.

The top ten holdings account for 52 percent of portfolio value.3

Natera (NTRA) alone was $575.3 million and 12.8 percent of the book at the Q4 2025 mark, though NTRA has since fallen from $229 to $212.80 as of today, pulling the mark-to-market value to $534.4 million. Add Insmed (INSM) at $257.9 million and NewAmsterdam Pharma at $107.7 million and nearly a quarter of Druckenmiller's reportable dollars sit in mid-cap biotech. That is an aggressive bet, not a preservation portfolio.

The second theme is emerging-market asymmetry. Two iShares MSCI Brazil ETF positions combine for $247.2 million, $134.3 million of which is held as call options. Sea Ltd, MercadoLibre, TSMC, and Coupang add another $540 million in EM exposure.3

What it really means

The naive read of this filing is that Warsh is rich. The smart read is that Warsh has delegated his directional market view to Stanley Druckenmiller.

Warsh controls the Fed Chair nomination. Druckenmiller controls the portfolio. The Brazil call stack, the biotech concentration, the Coupang position, the Teva rebuild, the Amazon and Alphabet core, all of it was built by Druckenmiller and his team while Warsh was writing op-eds about monetary policy and collecting $10.2 million a year for "advisory services."1,4

That relationship is more than a paycheck. Druckenmiller ran for the Fed Chair job indirectly for a decade through Warsh.

Warsh ran for the job directly. The capital stack says they have been partners for fifteen years.4

Two second-order implications follow from that.

First, Warsh's personal balance sheet is a quiet vote of confidence in growth equity and biotech, not in Treasurys. Most Fed Chairs in modern history have kept their wealth in Treasury ladders, index funds, and municipal bonds.

Powell's 2024 disclosure was overwhelmingly muni bonds and cash-equivalent funds. Warsh's personal capital sits in a hedge fund that bought Natera calls and Brazil leverage.1

Second, the Coupang position is the sharpest conflict on the page. Warsh has been a Coupang director since October 2019 and holds Class A common plus RSUs worth $2-10 million directly, all while Duquesne simultaneously holds 6.77 million Coupang shares worth $159.8 million at the Q4 mark.1,3

OGE flagged Line 23 onward for divestment, which covers the fund stake but not the board seat. The RSUs vest in June 2026 if Warsh stays on the board. He will almost certainly have to resign the directorship.

What the media got wrong

The Washington Times and CNBC led with "wealthiest Fed Chair on record." The number they chose was $100 million plus, and they anchored on Jane Lauder's $1.9 billion Estee Lauder fortune.5,6

That framing misses the actual signal. Jane Lauder's wealth is passive.

It sits in EL Class A and Class B stock, Suffolk County land, trust-held municipal bonds across 16 states, and a rotating ETF sleeve of SPY, EFA, VWO, and XIU. That is a textbook dynastic portfolio.1

Warsh's own capital allocation, by contrast, is active and concentrated. The Duquesne stake, the Bessemer VIII-XI-XII LP positions, the DCM Investments 9 and 10 exposure with 100+ private venture names including SpaceX, Polymarket, Recraft, 11x, Partiful, Cafe X, and Cionic, and the 72 series of THSDFS LLC co-investments all point in one direction.

Warsh runs a growth-equity and venture book with public-market overlay.1

Reporters also missed the crypto angle entirely. Zero headlines mentioned that a nominee for Fed Chair has venture exposure to Compound, Brave, dYdX, Polychain, Scalar Capital, Blast (yield-generating Ethereum layer two), DeSo, Flashnet, Lightning Network, Optimism, Tenderly, and Lemon Cash, and advises Electric Capital as a paid consultant.1

He owns no Bitcoin and no Ether directly, but his fund stakes touch nearly every layer of the programmable-money stack.

The composition problem. Floor estimates of Warsh disclosed holdings, low end of reported OGE ranges.

Category floors computed from lowest end of OGE Form 278e reported dollar ranges, aggregated across Parts 2, 5, and 6. Actual values are higher. Duquesne/Juggernaut bucket sums the two "Over $50M" lines at exactly $50M plus $50M plus $40M of related Duquesne-advised positions flagged in the OGE certification note.¹

The counter-argument

Three credible objections to the thesis deserve treatment.

First, the Juggernaut Fund and Duquesne Family Office may not be perfectly synonymous. Juggernaut could technically be a single series or segregated portfolio within the Duquesne umbrella.

The 13-F filer name is Duquesne Family Office LLC. The OGE endnote explicitly references that 13-F as the underlying holdings disclosure, which is the strongest available confirmation, but the precise legal wrapper could differ.1,3

Second, Warsh being an LP in Druckenmiller's fund does not prove Warsh shares Druckenmiller's macro views. A passive LP position reflects confidence in the manager, not agreement on every trade.

Warsh has been publicly more hawkish on inflation than Druckenmiller has been on growth since 2023, and yet has kept his money in Druckenmiller's book. That is either a vote of confidence in the manager's skill or evidence that Warsh's public writing and his private portfolio answer to different constituencies.

Third, the sheer concentration in Duquesne could be an artifact of how Warsh structured his wealth rather than an ongoing conviction bet. He joined Duquesne as an advisor in April 2011, almost immediately after leaving the Fed. Fifteen years of compounding inside a single fund can produce a $100 million-plus stake without any fresh allocation decisions.

Against these, the consulting fee pattern is hard to explain away. $10.2 million in 2025 alone, rising from an estimated $7 million in 2023, suggests an active and intensifying commercial relationship, not a dormant legacy LP position. The 13-F concentration in Coupang specifically, where Warsh also sits on the board and holds direct equity, is a piece of portfolio overlap that almost certainly involved communication between the principals. And the $4.5 billion 13-F is small enough that individual stock positions of $50 million to $500 million reflect real conviction, not passive index drift.1,3

The counter-argument narrows the claim rather than defeats it. Warsh has meaningful financial exposure to Druckenmiller's market views, whether or not he shares the specific individual trades.

The retail implication

The disclosure gives retail investors three useful signals.

Signal one. Duquesne's Q4 2025 concentration in Natera is the single largest conviction bet by a macro-sophisticated investor in a single diagnostic-testing name. NTRA is 12.8 percent of a $4.5 billion book run by someone whose last three decades compounded at roughly 30 percent annualized gross.4 That is a traceable, public data point.

Signal two. The Brazil call stack. $134.3 million of iShares MSCI Brazil ETF calls sits on top of $112.9 million in the underlying, for combined weight of 5.5 percent of the book.

EM equity has underperformed US equity for fifteen years. A Duquesne-sized leveraged bet against that pattern is itself a data point.3

Signal three. The Fed Chair nominee holds zero Bitcoin. Every crypto advocate in Washington has spent eighteen months arguing that US monetary policy should explicitly incorporate digital assets.

The man nominated to run the Fed did not put a dollar into Bitcoin or Ether directly. That is not a prediction about crypto prices.

It is a read on how the nominee personally thinks about the asset class.1

None of these signals is a recommendation. Each is a piece of information that retail investors did not have before April 10.

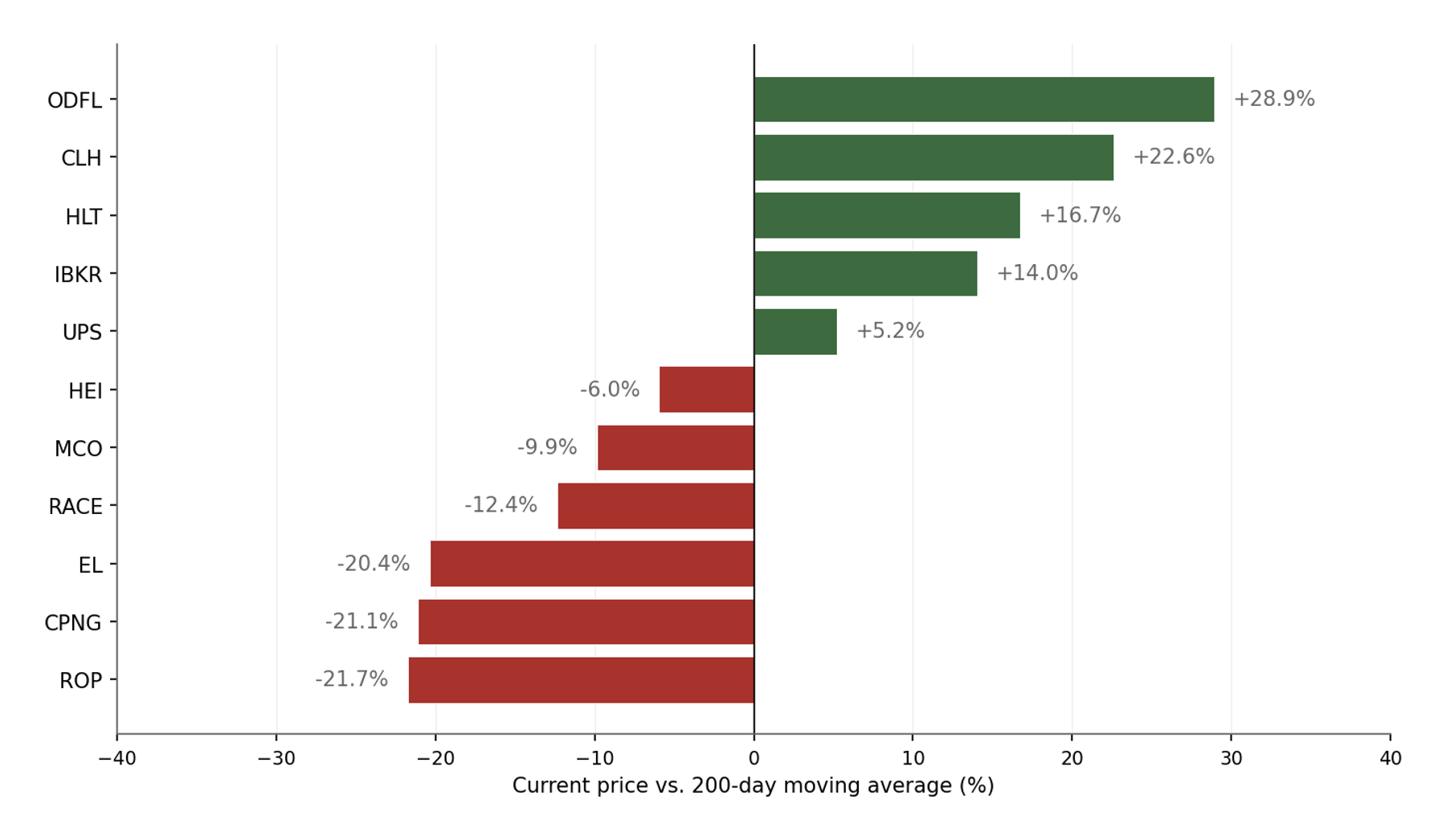

The public-stock sleeve the Senate will see at the hearing. Warsh-linked tickers, price versus 200-day moving average.

Last price and 200-day moving average as of April 14, 2026 close via Yahoo Finance API. Tickers include direct Warsh filer holdings (CPNG, UPS), spouse-held Lansing Management concentrated equity positions (IBKR, HEI, MCO, RACE, HLT, ROP, CLH, ODFL), and Estee Lauder (EL) held across multiple spouse trusts.¹,⁷

Key data table

| Item | Detail |

|---|---|

| Filer | Kevin Warsh, Chairman & Member nominee, Board of Governors, Federal Reserve |

| Filing | OGE Form 278e, Nominee Report, signed 2026-02-25, certified 2026-04-10 |

| Largest single disclosed asset | Juggernaut Fund, LP (Duquesne Family Office LP stake), Over $50M plus Over $50M across two entries |

| 2025 consulting fees, total | $13,150,000 across four firms |

| Duquesne Family Office | $10,200,000 |

| GoldenTree Asset Management | $1,550,000 |

| Cerberus Capital Management | $750,000 |

| Heitman | $650,000 |

| 2025 speaking fees, total | $1,534,000 across nine engagements |

| Largest single honorarium | Brevan Howard, $750,000 across three dates |

| 2025 Juggernaut income (lines 86.3 + 87) | $14,232,000 + $2,765,000 = $16,997,000 |

| Duquesne 13-F AUM (Q4 2025) | $4,494,450,000 across 62 positions |

| Duquesne top position (Q4 mark) | Natera (NTRA), $575.3M, 12.8% of 13-F book |

| Natera mark-to-market (Apr 14 2026) | 2,511,357 shares × $212.80 = $534.4M |

| Household wealth range (Barron's) | $131 million to $209 million, based on OGE line-item floor and ceiling |

| Direct public stock (filer) | Coupang (CPNG) $1M-$5M, plus UPS phantom stock $1M-$5M and UPS RSUs $1M-$5M |

| Spouse concentrated stock | Estee Lauder (EL) Class A plus Class B, aggregate Over $3M across multiple trusts |

| Spouse real estate | Undeveloped land, Suffolk County NY, $5M-$25M |

| Direct Bitcoin / Ether / coin holdings | Zero |

| Crypto venture exposure | Indirect via Bessemer, DCM, THSDFS funds (Brave, Compound, dYdX, Polychain, Scalar, Lightning Network, Optimism, Tenderly, Flashnet, DeSo, Blast, Lemon Cash) |

| AI & frontier venture exposure | SpaceX (acquired xAI), Polymarket, Recraft, 11x, Delphi AI, Volt, Outpace Bio, Cafe X, Cionic, Partiful, StashFin (all via DCM) |

| Public company board seats | UPS (since 2012), Coupang (since 2019), Bessemer Securities Corp (since 2013), Aven Holdings advisory |

| Debt | JPMorgan mortgage 2.875% from 2015 ($1M-$5M), PNC exercised line of credit 6.088% from 2025 ($1M-$5M) |

| OGE flagged for divestment | Part 2 lines 23, 25-53, 55-85, 86.3, 87 (value-range floor sums to approximately $122M) |

Price verification, April 14 2026

Every price below is pulled live from OpenBB Tier 0 at the moment of publication. Marks are today's last trade, not Q4 closes.

| Ticker | Name | Price (Apr 14 2026) | Context |

|---|---|---|---|

| NTRA | Natera | $212.80 | Duquesne top holding. Down from $229 year-end, mark-to-market $534.4M |

| INSM | Insmed | $151.49 | Duquesne 5.7% weight. Down ~13% from Q4 mark of $174 |

| CPNG | Coupang | $20.36 | Warsh direct holding plus Duquesne 6.77M shares. Up modestly |

| UPS | United Parcel Service | $102.32 | Warsh phantom stock and RSUs, board director since 2012 |

| EL | Estee Lauder | $75.76 | Jane Lauder core holding. Down from 52-week high of $121 |

| EWZ | iShares MSCI Brazil ETF | $41.69 | Duquesne $247M combined call plus underlying. Near 52-week high |

| SPY | S&P 500 ETF | $692.73 | Duquesne SPY calls $61.4M. Benchmark reference |

| HEI | HEICO | $298.72 | Lansing Management concentrated sleeve holding |

| MCO | Moody's | $437.12 | Lansing concentrated sleeve |

| IBKR | Interactive Brokers | $76.56 | Lansing concentrated sleeve, 52-week high territory |

| ROP | Roper Technologies | $355.15 | Lansing concentrated sleeve |

| RACE | Ferrari | $359.02 | Lansing concentrated sleeve |

| CLH | Clean Harbors | $304.03 | Lansing concentrated sleeve, near 52-week high |

| ODFL | Old Dominion | $209.56 | Lansing concentrated sleeve |

| HLT | Hilton | $330.46 | Lansing concentrated sleeve, 52-week high |

| APG | APi Group | $45.35 | Lansing concentrated sleeve, 52-week high |

Source: OpenBB Tier 0 quote API via yfinance provider, pulled 2026-04-14 14:43 ET.

Catalyst map

The Senate Banking Committee hearing is scheduled for April 16. Warsh will be asked about the Duquesne relationship under oath. The divestment timeline runs from confirmation date forward, typically 90 days.8

Coupang Q1 2026 earnings drop in early May. If Warsh is confirmed before that print, he will need to resign the directorship to avoid RSU vesting at the June 12 annual meeting. Watch for a Form 8-K director resignation in late April or early May.

Duquesne's next 13-F drops in mid-May and covers Q1 2026 positioning. The relevant question is whether Druckenmiller trimmed Natera, given it is the single largest factor in the book and Warsh cannot plausibly continue to be an LP into confirmation.3

The Bottom Line

Warsh's disclosure shows the Fed Chair nominee has outsourced his personal market allocation to Stan Druckenmiller for fifteen years, earned $13.15 million in 2025 consulting fees from four buy-side firms with another $1.534 million in speaking fees layered on top, and will be required to divest approximately $122 million in Druckenmiller-linked positions if confirmed. The counter-argument that he is a passive LP narrows the claim but does not defeat it, because the $10.2 million Duquesne fee alone points to an active relationship. If confirmed, the next Fed Chair will have a personal portfolio built by one of the most aggressive growth-equity macro traders of the past three decades.

Sources

Sources

Office of Government Ethics, Kevin Warsh OGE Form 278e, Nominee Report, signed 2026-02-25, certified 2026-04-10. https://extapps2.oge.gov/201/Presiden.nsf/PAS+Index/F57618ED6E5F30B585258DD9002DD780/$FILE/Warsh,%20Kevin%20%20final278.pdf

SEC EDGAR, Duquesne Family Office LLC, CIK 0001536411, filer profile and filing history. https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0001536411

Duquesne Family Office LLC, Form 13F-HR for period ending 2025-12-31, filed 2026-02-17, accession 0001536411-26-000002.

Duquesne Capital Management historical performance context, via multiple financial journalism sources (Bloomberg, Institutional Investor) covering Druckenmiller's track record.

Washington Times, "Fed nominee Kevin Warsh's disclosed wealth surpasses $100 million," 2026-04-14.

CNBC, "Kevin Warsh Fed chair confirmation plan hits snag as nomination hearing is delayed," 2026-04-10.

OpenBB / Yahoo Finance real-time quote API, 2026-04-14 close, for CPNG, UPS, EL, HEI, MCO, IBKR, HLT, ROP, RACE, CLH, ODFL, SPY, EFA, VWO.

Axios, "Kevin Warsh will face the Senate next week," 2026-04-14.

Barron's, "Fed Chair Nominee Kevin Warsh Is Worth $131 Million to $209 Million. See His Portfolio," 2026-04-14.

ProCap Insights is a research division of ProCap Financial. This report is for informational and analytical purposes only. It does not constitute investment advice and does not make buy, sell, or hold recommendations on any security. Nothing in this report should be construed as a solicitation or recommendation to buy or sell any financial instrument. Readers should conduct their own due diligence and consult a qualified financial advisor before making any investment decision.